Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

Stocks ran into a bit of a roadblock in the first half of August much like they did around the same time in 2022. The catalyst for the sell-off was the continual rise in longer-term interest rates, which lead to pronounced weakness in ‘longer duration assets’ that are most sensitive to rising interest rates. Top of that list were the growth stocks such as technology, which were ripe for a pullback given their exceptional strength thus far in 2023 and the extreme readings on bullish sentiment in the group. The big names such as Apple, Microsoft and Tesla fell as much as 20% before rallying in the back half of the month. Energy stocks provided some ballast that kept the major indices from breaking further as higher oil prices and low valuations assured continued buying. The big worry for investors had been the annual Jackson Hole Symposium and the headline speech from Fed Chair Jerome Powell. His speech in that gathering in 2022 highlighted that interest rates would continue to rise and that there could be some ‘economic pain.’ That prognosis ignited the market sell-off that didn’t see a bottom until October, 2022. This year the anticipation proved worse than the reality. Although he continued to espouse hawkish views about the need to keep interest rates ‘higher for longer’ to get inflation down to their 2% target, investors seemed to sigh a relief that the comments weren’t more draconian than that. Blowout earnings and guidance from Nvidia also helped to jump-start buying in the technology sector again.

After seeing the sharpest increase in interest rates in more than five decades over the prior year, almost all strategists, economists and investors (ourselves definitely included) expected the economy to cool off sharply this year, particularly since we had all grown accustomed to a very low interest rate environment over the past decade and debts had ratcheted up accordingly. The much-anticipated slowdown has clearly not yet come about, particularly in the U.S. and many pundits are now looking for a resumption of growth in 2024. Forward consensus earnings estimates for the S&P500 are actually now calling for 12% earnings growth next year! The biggest reason we have not seen a typical slowdown in economic growth this year, in our view, was due to the continued support from the massive fiscal stimulus from the Inflation Reduction Act and the Chips Act as well as the accumulated savings from the pandemic stimulus payments. Quantifying this support, an incremental $2.25 trillion payout to the household sector, underwritten by the U.S. Federal government and same Federal Reserve that is trying to push down the inflation it actually helped create. This multi-trillion dollar cash transfer has yet to run out but is also masking some serious shortfalls in spending due to the rise in interest rates. If real consumer spending was constrained to the growth in real disposable incomes since March 2021, it would have been unchanged instead of expanding +10% over this two-year span. This, in turn, would have lead to real GDP growth coming in barely better than a +1% annual rate (i.e. ‘stall speed’) rather than the actual ‘stimulus-lead’ +1.8% growth.

But the economy has yet to fully reset to this new and higher interest rate environment. It typically takes two years before a recession arrives in the aftermath of the initial Fed rate hikes. More importantly, the aggressive four consecutive ¾ point interest rates increases did not come until the back half of 2022. We expect to see continued economic deterioration and, by the time we see the full brunt of the policy lags, the last of the “excess savings” theme in terms of consumer spending support will be gone.

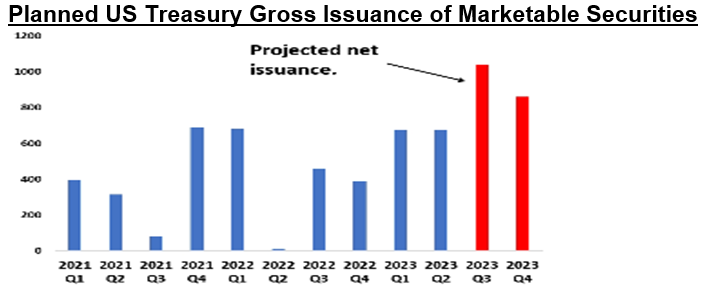

So, if the economy is weakening and inflation is slowly coming down, then why are longer-term interest rates back on the rise again? Ten-year government bond yields rose a full percentage point in the past four months, from 3.3% to 4.3%! We believe this is less a result of expectations for higher growth and a resumption of inflation, but more from the recent increase in the announced issuance of debt over the balance of the year. In essence, it is more of a supply/demand issue than a call on the outlook. The chart below shows the issuance of debt by the US Treasury. They increased the expected supply of bonds for the balance of 2023 by over US$300 billion! That announcement also coincided with the US debt downgrade by Moody’s, which sent many potential investors ‘into hiding.’ Ultimately, we expect that a weakening of the economy and lower inflation will push longer-term interest rates back down.

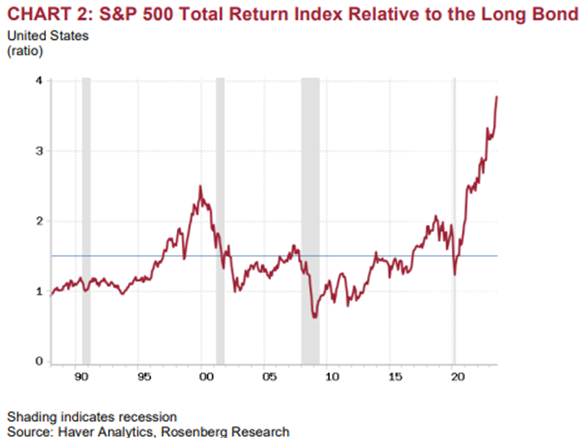

Asset allocation is always one of the key decisions to be made in any investment portfolio. Those shifts should not be extreme with regards to stocks since success in ‘market-timing’ has always been elusive for most investors. Not only do they have to accurately manage when it is time to reduce stocks, they also have to make a timely decision as to when to get back into the market in order to capture the long-term positive returns. So, while not advocating such major changes in asset mix, there are times when the relative returns of various asset classes tend to get distorted, thus providing opportunities to re-balance portfolios. We believe we are in such a period right now with respect to the better opportunities in bonds versus stocks over the next year. To put it in perspective and as shown in the chart below, the long-run average relative index of the S&P500 total return to the 30-year bond return is 1.5. Today, that ratio sits at an unprecedented 3.8. The chart below looks even more extreme than it did at the peak of the ‘dot-com bubble’ back in 1999.

For this reason, we have been “buying the dip” in the Treasury Bond market and reducing our weight in stocks, particularly those in the economically sensitive/ cyclical sectors such as financials, consumer spending and industrials. Stocks certainly have been the place to be for most of this year, recovering much of last year’s losses, particularly in growth sectors such as technology. But we still have concerns about the outlook. While the extremely bullish sentiment measures have cooled off a bit due to the early August sell-off in stocks, they remain at elevated levels and therefore a contrarian bearish backdrop for the stock market. Also, given our concerns about a weakening economy, we believe that the consensus expectation for 12% earnings growth in 2024 is far too optimistic. Finally, despite the claims of most central bankers (and amplified by US Fed Chief Jerome Powell’s headline speech at the recent annual Jackson Hole symposium) that interest rates need to remain ‘higher for longer’ in order to bring inflation down to the 2% target, investors are still clinging to the idea that short-term interest rates are at (or nearly at) their peak levels and will start to fall in 2024. We don’t believe that narrative unless there is another economic shock (like the SVB banking failure in March) or growth has a much sharper drop than expected.

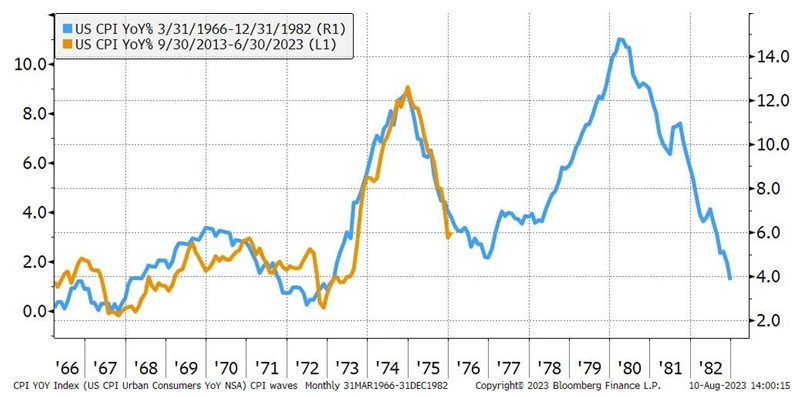

We believe that central bankers want to avoid a repeat of the mistakes made during the inflation surge of the 1970s. The chart below of the U.S. consumer price index (CPI) inflation shows the year-over-year percentage change from 1966 to 1982 in blue, overlayed on the past decade in orange. The path thus far has been remakable similar. But after inflation started to come down, central banks eased up on their tightness only to see inflation re-accelerate for the balance of the decade. That necessitated Paul Volcker to push interest rates into the low-teens in 1980 to finally see a break in the rate of inflation. However that also came with ‘back-to-back’ recessions in the 1980-82 period. In Canada, those of us old enough to remember will recall (then) Prime Minister Pierre Trudeau’s pledge of “6 and 5”, which was his inflation target. That was the same year that we saw a record 19.5% rate for the November annual Canada Savings Bond (CSB) program. Nobody wants to get into a repeat of that episode and we expect that central bankers are aware of these risks of prematurely cutting interest rates before inflation is comfortably back into the target range.

Given all these concerns, we continue to have a cautious outlook for stocks and have structured client portfolios accordingly. Cash balances are currently slightly higher than normal and we have recently added to bond holdings to move them into an overweight position (around 40% asset allocation). We are holding a similar weight in stocks, which is an underweight to the traditional benchmark of a 60(stock)/40(bond) portfolio. The focus in the stock allocation has been on defensive positions with less economic sensitivity, high dividend yields, moderate valuations and secular growth potential. The top sector in Canada that fits that mould right now is the telecom group. We recently added to positions in Rogers, BCE and Telus. Worries about a wireless ‘price war’ are exaggerated in our view while we continue to see growth of broadband services due to growing wireless apps and streaming activities. Rogers will see additional growth from the absorption of Shaw Communications and should be in a position to start increasing the dividend again once the acquisition debt gets reduced to a more manageable level. Telus has been hurt by weakness at Telus International but carries a dividend yield of 6% and trades at its lowest valuation since prior to the pandemic. BCE is more constrained on growth but has stable earnings and a safe dividend yield of 6.7%!

Another sector where we are overweight and have added recently is the pipeline group. Energy infrastructure remains key in Canada to getting excess oil and gas supplies to international markets. TC Energy, Enbridge and Pembina Pipeline all trade at valuation discounts to their long-term averages (currently trading around 10-11 times operating cash flow) and all carry dividend yields well in excess of 6%. Earnings are stable that the overall energy sector since they are tied to volumes and have very little commodity price sensitivity. Cost overruns on existing projects have hampered performance, particularly for TC Energy, but we believe the discounted valuations and high dividend yields more than compensate for that.

Despite risks to valuations from the ‘hype’ around artificial intelligence (AI) and higher interest rates, we continue to carry a significant position in technology stocks in both the US and Canada. The highest conviction tech position in the portfolio right now is Nvidia. They have proven themselves to be the clear leader in the deployment of AI this year. The last two quarters the company has absolutely blown away the expectations. In May they guided to revenue of over $11 billion versus expectations of just $8 and then topped numbers again this quarter by forecasting next quarter revenue of over $16 billion. While the stock is up almost 200% so far this year, its valuation has actually come down due to the earnings growth. It started the year with annualized earnings of less than $5 per share but now carries estimates for the next fiscal year of almost $20 per share. There has been re-making of the entire data centre space to enable them to add AI tools and Nvidia has a dominant position in sales of graphics-processing units for AI related purposes, with around a 90% share of the market. It is therefore able to price at a premium to the rest of the industry. There are of course risks, the biggest one being that they don’t do their own manufacturing (they sub-contract to Taiwan Semi) and therefore could see supply issues that would impede them from meeting the growing demand. But they see little competition thus far, with AMD, Marvell and Broadcomm, among others, all running distance second places. Also, some of Nvidia’s own customers are shaping up to be its competition. Alphabet has its custom Tensor Processing Units, or TPUs, although it also partners with Nvidia for various AI applications. Amazon also has custom chips which it also offers as alternatives to Nvidia’s GPUs. But for the next two years, Nvidia seems to be the ‘only game in town’ for the expansion into AI services for so many customers. However, it’s not necessarily one factor or another that could hit Nvidia stock. A mixture of issues and the increasingly high hurdles it faces to beat expectations could be enough to puncture confidence in the stock. The company’s outstanding performance so far is only moving the bar higher for the stock to keep rising. But within the technology sector, it is very hard to ignore a company with such dominant growth in a transformative technology at a valuation that is not out of line with the rest of the industry!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.