Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

Welcome to 2026! I hope the year ahead is both happy and prosperous for everyone.

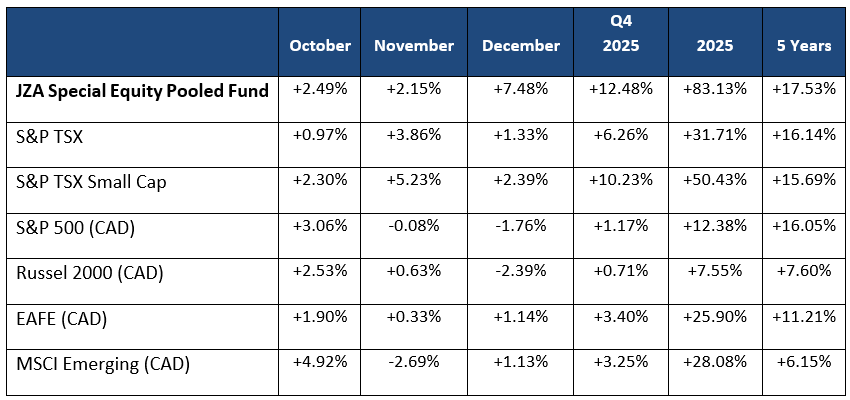

As we close out 2025, we can finally breathe a sigh of relief—portfolio results were exceptional in both the fourth quarter and the full year. Maintaining a significant weighting in materials throughout the year proved to be a major driver of performance. The portfolio returned +12.5% in the fourth quarter and +83.1% for the year, compared with the S&P/TSX Index at +10.2% for Q4 and +50.4% annually. In addition to strong quarterly and annual results, the portfolio has delivered +124% over the past 5 years, or +17.5% annualized, outperforming broad market benchmarks over the same period. For comparison, the S&P 500 returned +111% (≈16.1% annualized) and the NASDAQ returned +101% (≈15.0% annualized) over the same timeframe.

The table below highlights how the portfolio’s performance surpassed both the benchmark index and other major global indices.

Performance is NET of fees

Gold delivered an exceptional +66% gain for the year, ending at $4,319/oz after beginning at $2,603/oz. This rally was driven by lower real rates, a weakening U.S. dollar, and strong central bank buying as countries diversified their reserves away from U.S. dollar dependence. Silver was equally impressive, joining the move by mid‑year and finishing with a remarkable +149% annual increase. As the year progressed and attention on critical materials intensified, copper stood out as a key driver of global economic growth. Years of limited investment in exploration and development have positioned copper for a prolonged period of tight supply, supporting higher prices. Copper rose from $4.03/lb to $5.68/lb, a +41% gain for the year.

Oil, however, did not participate in the broader commodity rally. In contrast to copper, oil remains well‑supplied as OPEC gradually raises production quotas toward historical levels. Demand has been strong and is expected to remain resilient barring a slowdown in future growth. The portfolio has been underweight Oil and Gas for most of the year. In my last note, I indicated an intention to increase exposure in 2026 as the OPEC overhang eased, though recent developments surrounding Trump’s involvement in Venezuela may delay that shift. It remains unclear how quickly Venezuelan production could rise given significant infrastructure constraints.

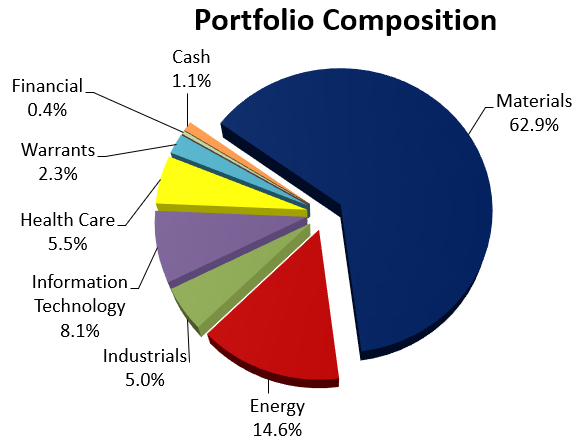

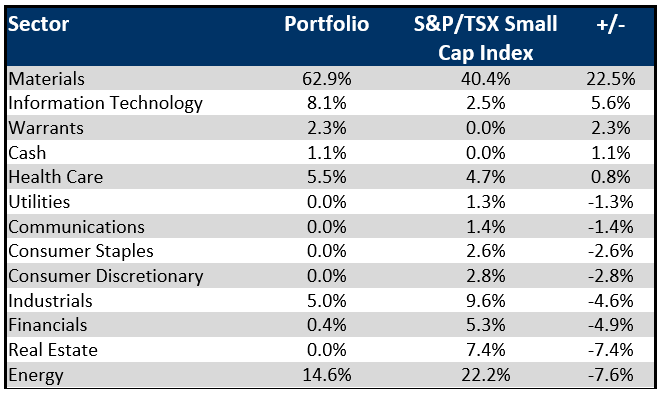

Despite the overwhelming strength in materials, several other sectors also performed well. The chart below highlights sector weights and attribution for the TSX Small Cap Index compared with the portfolio’s allocations versus the S&P/TSX Small Cap Index.

Attribution Review: Key Detractors and Contributors

Turning to the positions that contributed most to quarterly performance, several holdings added meaningful value, while others detracted. The largest detractors in the fourth quarter were Newcore Gold Limited, CanAlaska Uranium Limited, and MDA Space Limited, which together reduced portfolio returns by -1.3%.

Newcore Gold’s main asset is the Enchi Gold Project located in the Ghana along the Bibiani Shear Zone. The property is largely under explored with several high priority geochemical and geophysical anomalies yet to be tested. The current resource is largely a low-grade surface expression, but the deposit is on structure with the Chirano Mine that hosts deep dipping higher grade structures. The leadership of Newcore is top tier, with a proven track record. There is currently a 45,000-meter drill program underway, and we are looking forward to the results. The weakness in the stock may be explained by a warrant overhang that will be cleared up by February 2026. We continue to hold the Newcore position.

CanAlaska Uranium is a Canadian based exploration company which holds one of the largest uranium exploration portfolios (500,000 hectares) in the Canadian Athabasca Basin with the goal of project generation. The company is actively advancing the Pike Zone discovery – a new high-grade uranium discovery on its West McArthur Joint Venture project. Cameco and Dennison are active partners along side CanAlaska. The team is an experienced team with a proven track record of discovery. In November the company announced more results at the Pike Zone discovery that disappointed the market. Management was encouraged by the results, and the 2026 budget will focus on advancing the discovery. On the negative reaction we have added to the position.

MDA Space is a global leader with a 55-year legacy in the global space industry focusing within the satellite industry. Its business can be broken down into three segments, satellite systems, robotics and space operations and geo intelligence. The satellite component is the largest for MDA and the fastest growing segment with the resurgence of the LEO satellites. The program wins tend to be large in nature and take many years to convert into revenue. Over the course of the last few months there is concern regarding some existing long-term contracts and the competitive landscape. We have removed the position and look for more clarity regarding the future.

The three positions adding the largest return to the portfolio in the fourth quarter included Northisle Copper and Gold Inc., Rio2 Ltd., and Discovery Silver Corp. Collectively, the three names added +2.8% to returns.

Northisle Copper and Gold is located in Vancouver, Canada and owns one of the most developable copper-gold porphyry projects in the world. Located on northern Vancouver Island, the access to pre-existing infrastructure in a mining friendly community will help accelerate the development process. The North Island Project is a 34,000-hectare block of mineral titles. A recently updated PEA confirms the robustness of the project, and the company intends to advance towards a pre-feasibility study. We continue to hold a position but have trimmed to manage the weight within the portfolio.

Rio2 is a mining company focused on development and mining operations with an extremely strong team that have done it before. The company is currently focused on taking its Fenix Gold Project in Chile to production in the shortest possible timeframe based on a staged development strategy. The project is in the Atacama Region of Chile in an area referred to as the Maricunga Belt. It is an oxide heap leach project with capital of $235 million to bring into production that is on time and on budget and expected to begin commercial production early this year. In addition, the company has recently acquired Compania Minera Condestable in Peru. The asset purchased is a producing copper mine with clear room for expansion and provides immediate cash flow. The company raised capital to make the acquisition in December, and we added to the position on this raise.

Discovery Silver is an Americas-focused precious metals company with a diversified portfolio including high-quality gold producing assets in and near Timmins, Ontario, Canada and 100% ownership of the Cordero project in Mexico, one of the world’s largest silver development stage projects. In April of 2025 Discovery completed their purchase of the Porcupine Complex in Timmins from Newmont Corporation. Managements extensive experience in the region and the relatively low price to NAV paid provided significant upside for the stock to appreciate through the year. We continue to hold the position but have trimmed to keep the weighting at a level we are comfortable with.

Outlook

As we turn the calendar to a new year, it offers a natural moment to reflect on where we’ve been and where we are headed. When I began my career, the world was emerging from the “cold war,” interest rates were moving from double‑digit highs toward generational lows, and global economies were embracing integration through free trade and monetary unions. Lower costs, partnership, and collaboration were dominant themes, and the overall environment appeared optimistic.

Today, the landscape is very different. Multiple conflicts are unfolding, and major economies are re‑evaluating their reliance on foreign sources for the critical minerals that support growth. Interest rates remain low, but inflation has become a persistent challenge for policymakers. Deglobalization and a more inward‑focused mindset now shape global economic strategy. The world has grown more cautious, and nations increasingly prioritize self‑sufficiency.

Some argue recent U.S. political developments accelerated this shift, though the underlying trends were already in motion—it simply hastened their arrival. Regardless of who is in office, this new reality appears firmly established, and a return to the previous era seems unlikely.

From a Canadian perspective, these shifts are not entirely negative. Canada has long needed renewed investment in infrastructure to ensure our resources reach the markets that want them. As a country, we possess abundant critical minerals and energy, but we must reduce the regulatory hurdles that impede responsible development.

In 2025, the materials sector delivered a substantial rally, with both precious and base metals showing strength. While it is unlikely that precious metals will repeat last year’s magnitude of gains, we do not anticipate weakness. With interest rates trending lower and central banks continuing to accumulate gold to diversify away from the U.S. dollar, a steady upward trajectory seems reasonable. In this environment, disciplined stock selection is essential. Advancing projects should narrow their discount to NAV as they progress, creating meaningful value. Companies such as G Mining, Erdene, and Rio2 stand out. Larger producers, supported by strong free cash flow, may also drive increased M&A activity, with developers like Freegold, Banyan, Collective, and Omai well positioned for consolidation.

Turning to copper, we expect another very strong year. While supply shortages dominated last year’s narrative, both constrained supply and solid demand should support a robust backdrop in 2026. Preferred names include Capstone, Hudbay, Taseko, North Isle, and Osisko Mining. The portfolio continues to maintain a significant overweight in basic materials and a solid overweight in precious metals.

We remain underweight energy and recently reduced natural gas exposure in favour of oil‑weighted producers and service companies. As the quarter progresses, we expect to move closer to market weight. Oil prices have been held back by the OPEC supply overhang, but as excess production is absorbed, fundamentals should normalize and create a more constructive environment. Companies of interest include IPCO, Tamarack Valley, Spartan Delta, and McCoy.

While the portfolio typically holds a group of growth‑oriented technology names, recent conditions have made it difficult to find companies with consistent performance and predictable growth. Instead, we have leaned more toward industrials and healthcare for diversification and upside potential. Key holdings include Kraken, Gatekeeper, Tantalus, and Firan in industrials, and Extendicare, Savaria, and Spectral Medical in healthcare.

The narrative this quarter remains broadly consistent with last quarter, and our optimism for the year ahead is unchanged. Global conditions continue to support a sustained rally in hard assets. The recent breakout in the TSX Venture Index illustrates this backdrop well. After finally surpassing the 1000 level for only the second time since the COVID period, the index appears to be entering a multi‑year breakout. For those who viewed last year as a potential blow‑off top, the long‑term chart tells a different story. With global equity markets reaching new highs, the TSX Venture’s previous peak—above 3400 in 2008—remains far ahead, suggesting there may still be considerable room to run.

Happy 2026!! Stay invested in Canadian Small Cap stocks!!!

Please reach out with any questions or if you’d like to discuss these themes further.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.