Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

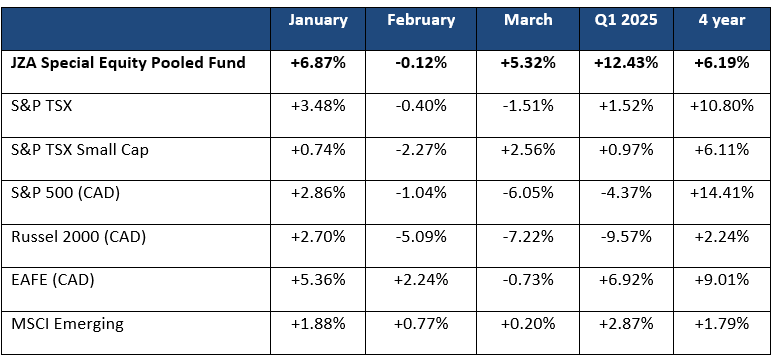

We’re happy to have the first quarter of 2025 in the books. It was a volatile period, but the portfolio delivered strong results—both on an absolute basis and relative to the benchmark. The portfolio returned +12.4%, outperforming the TSX Small Cap Index by +11.4%, which returned just +1.0% last quarter.

Below is a summary of Q1 2025 performance across major global indices. Notably, U.S. equities struggled as Trump’s renewed tariff policies weighed on markets, particularly technology stocks, which entered bear market territory. In contrast, European markets posted positive returns.

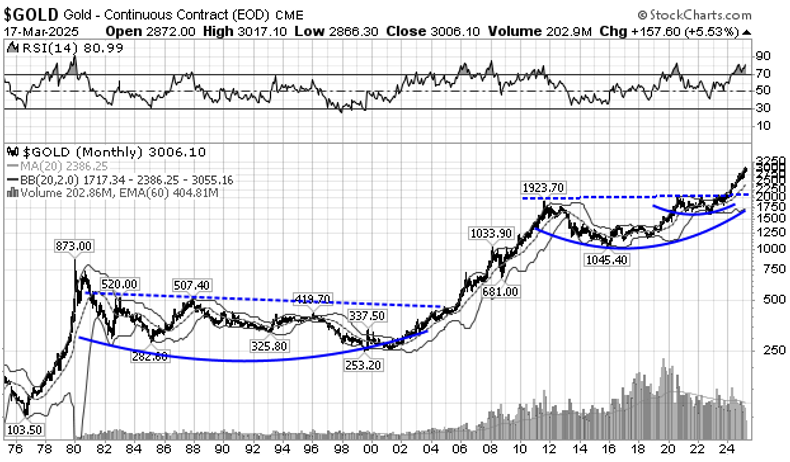

Much of our outperformance stemmed from the strong performance of gold and copper. Gold rallied 19% during the quarter, and for the first time in some time, gold equities responded with strength. Our significant overweight to the sector paid off meaningfully. Copper also rallied sharply, up 25% during the quarter, adding to our returns.

On the other hand, Energy, Industrials, and Technology were a drag on the portfolio. We had increased our energy exposure early in the year to a modest overweight, but we quickly pivoted to focus on natural gas names in anticipation of stronger pricing as Canada’s first LNG export facility begins operation in the second half of 2025.

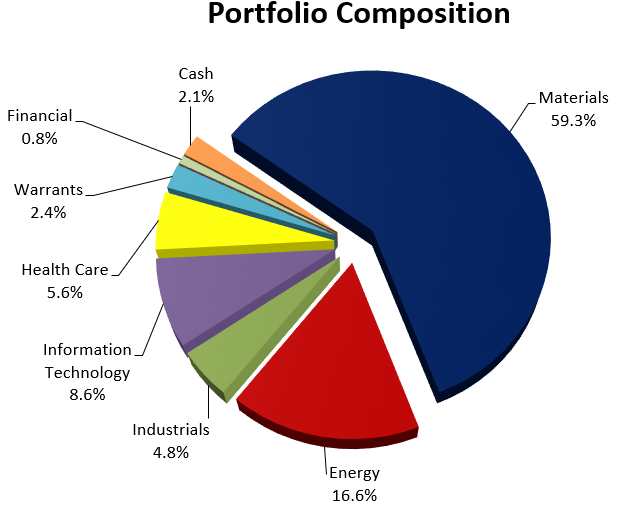

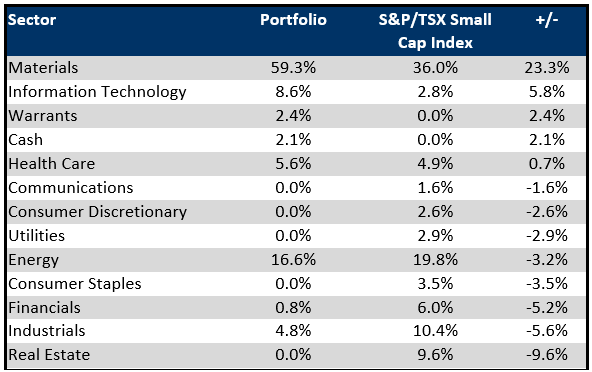

The sector weight chart below (not shown here) illustrates our positioning relative to the index. While gold exposure was a standout, security selection within sectors also played a vital role in our outperformance.

The three largest detractors in the quarter were Capstone Copper, Source Energy, and Hudbay Minerals. Combined, these names detracted -1.4% from performance.

Capstone Copper and Hudbay Minerals are both copper producers with high-quality assets across North and South America. Early in the quarter, copper prices rallied sharply, with the LME-Comex spread widening dramatically due to aggressive U.S. buying in anticipation of tariffs. However, after Trump’s April 3 “Liberation Day” announcement of unexpectedly high tariffs, sentiment shifted rapidly. Fears moved from copper shortages to concerns about a global recession, driving prices and equities down.

Capstone and Hudbay had both performed well over the past several years, but with growing market uncertainty, both were aggressively sold. We are not attempting to predict the resolution of the current trade war in the short term, but we remain convinced that structurally the world is in a copper deficit. Both companies have strong growth profiles and balance sheets, and we’ve used this weakness to add to our positions.

Source Energy Services is a frac sand logistics company servicing Canadian oil and gas producers. Source imports a significant portion of its sand from the U.S., and recent reciprocal tariffs have squeezed margins. Additionally, falling commodity prices (WTI around $60 and weak natural gas) have led to reduced drilling activity and pressure on cash flow across the sector. While we continue to like Source’s strategic infrastructure network, we are waiting for a more attractive entry point before adding to our position.

The three top contributors this quarter were Collective Mining, Spectral Medical, and NorthIsle Copper and Gold, which collectively added +3.0% to portfolio performance.

Collective Mining is an exploration company advancing the Guayabales project in Colombia, anchored by the Apollo system, which hosts high-grade gold-silver-copper-tungsten mineralization. The same management team previously built Continental Gold, which was acquired by Zijin Mining in 2019. We were early investors, following our strategy of backing proven teams. In March, Agnico Eagle increased its stake to 14.99%, demonstrating confidence in the management and company. We continue to hold a core position and recently trimmed our weighting on price appreciation and allocate the capital to new opportunities.

Spectral Medical is developing PMX, a therapeutic hemoperfusion device for septic shock, guided by its FDA-cleared Endotoxin Activity Assay. PMX is already approved in Japan and Europe and has treated over 340,000 patients. Spectral is in a Phase 3 trial (Tigris Study), which faced delays due to COVID, but is now nearing completion. We maintain our position in anticipation of positive data and commercial rollout.

NorthIsle Copper and Gold is developing the North Island project on Vancouver Island, a brownfield site with excellent infrastructure. The company recently released an updated PEA and is progressing toward pre-feasibility. Exploration continues across its broader 34,000-hectare land package. The stock performed strongly following the lifting of the four-month trade restrictions, and we’ve since trimmed our position to keep the weight in line with our risk guidelines.

Writing this section is more difficult than usual. On January 20, 2025, Donald Trump was inaugurated as the 47th President of the United States, achieving control of the presidency, Senate, and House. Markets initially welcomed the clarity, but sentiment quickly turned when Trump launched a global trade war. Canada and Mexico were first to face tariffs, with further escalations reaching Europe and Asia.

April 2, “Liberation Day,” marked a turning point when the scale of tariffs dramatically exceeded expectations. The result has been rising volatility and sharp corrections across equity, bond, and currency markets. U.S. equities, especially in the technology sector, have suffered a swift re-rating.

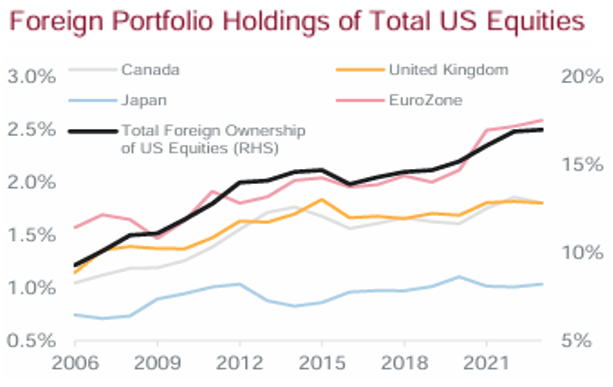

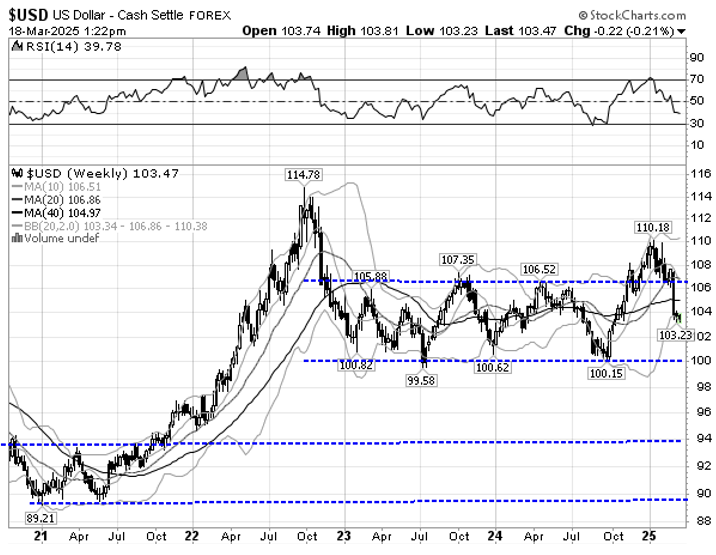

Foreign ownership of U.S. equities had surged over the past five years, amplified by a strong USD. As the administration’s unpredictability grows, there is risk of widespread repatriation.

We do not believe that Trump’s vision of reshoring global supply chains is achievable in the short term. Capital projects take years to plan and execute, and the business community is unlikely to invest in new U.S. facilities with this level of policy uncertainty. With economists now revising growth forecasts downward, the key question is whether we are headed into a recession. At this point, it is unclear. Recent signs that Trump may be pausing or renegotiating some tariffs offer a faint glimmer of optimism.

In the meantime, gold has emerged as a safe haven. The portfolio’s overweight in gold has helped mitigate broader market declines.

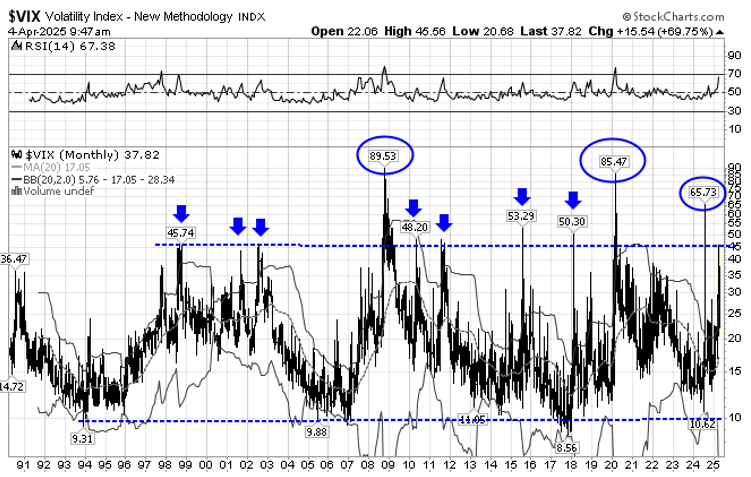

As the correction continues, we expect to trim gold positions in favor of more cyclical sectors such as base metals, industrials, and energy, particularly if macro conditions stabilize. With the VIX recently hitting extreme levels, we believe we may be approaching a market bottom and we are actively evaluating companies showing leadership potential in this evolving landscape. Names like Kits Eyewear, Kneat.com, MDA Space, and Firan Technology offer strong fundamentals and relatively low tariff exposure.

The last four decades of globalization and North American supply chain integration will not be reversed overnight. Global trade and specialization have driven tremendous global growth. While some sectors have lost ground, others have flourished. Economic theory supports global productivity through comparative advantage.

If there is a takeaway from this volatility, it is that Canada must invest in itself. We need to reduce internal barriers, improve permitting and infrastructure, support innovation, and enhance productivity. We have the resources the world needs. It is time for all of us (large and small) to repatriate capital back and invest in Canada.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.