Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

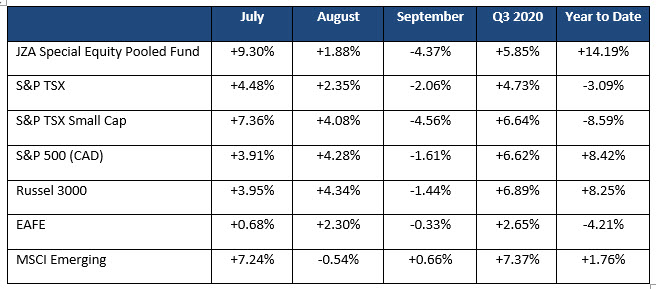

Global stock markets were strong in the third quarter with robust returns in July and August and a moderate pullback in September. Your portfolio was up +5.9% last quarter and is up +14.2% for the year. In the third quarter, the portfolio outperformed the S&P Canadian Small Cap Index by +1.2% and is ahead of the S&P TSX Small Cap Index by +22.8% in 2020. Below is a table of the portfolio and the major global stock market returns for the quarter and the year to date.

The third quarter unfolded as we expected. We knew it would be a little bumpy after the tremendous run in the second quarter. By the last month of the third quarter, investors started to become concerned with the upcoming US elections and the “second wave” of the COVID pandemic. While we forecast a strong fourth quarter for stocks, we anticipate the market will continue to be choppy until the US election. Following the election, investors should get policy clarity and the US government should be able to pass a robust (approx. $2 trillion) stimulus package. Furthermore, with COVID infections rising again, numerous governments are launching new fiscal and monetary stimulus policies to offset the economic impact.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.