Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

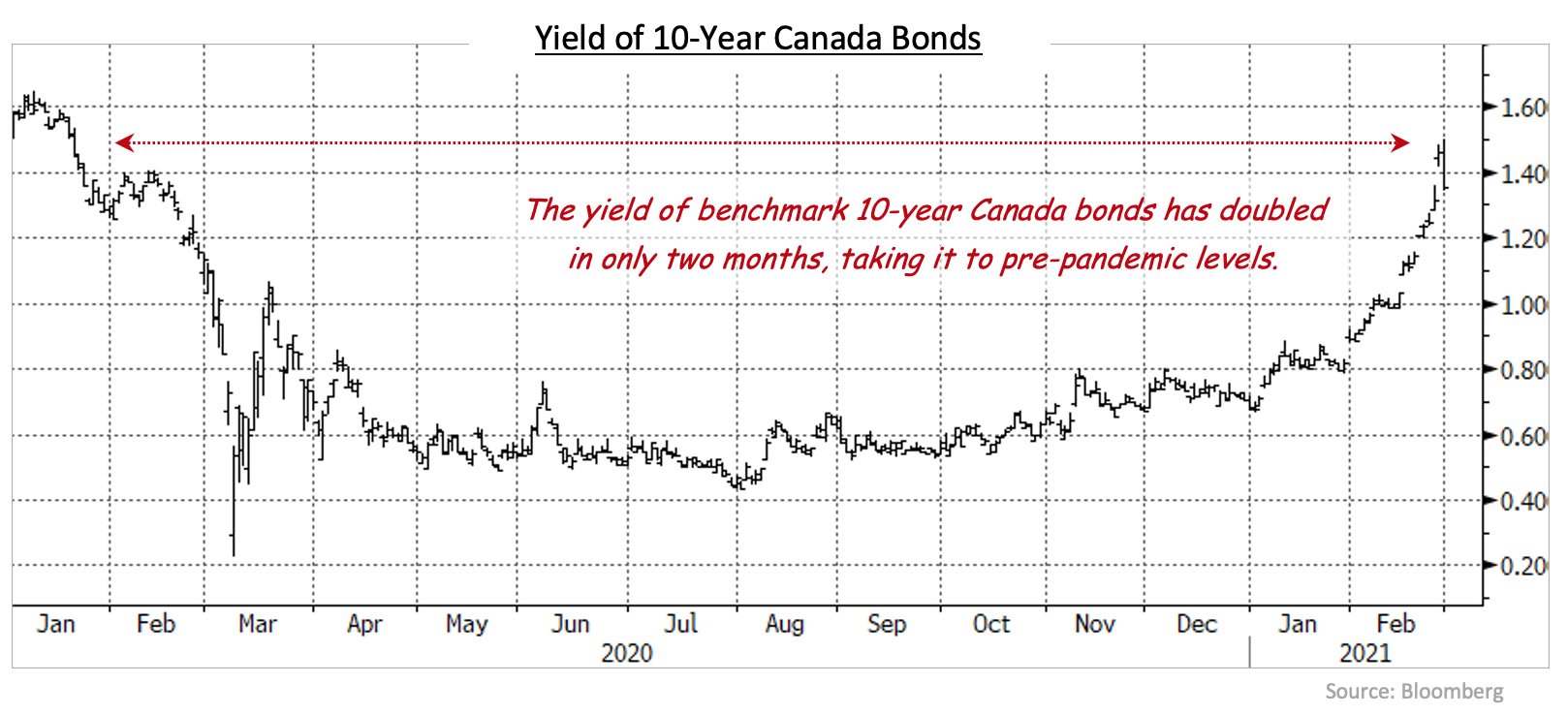

Global markets experienced dramatic increases in yields during February as investors reacted to rising vaccination rates by anticipating strong economic recoveries and potentially rising inflation. The jump in yields appeared to be triggered by a selloff in the U.S. Treasury market where investors were concerned about the impact of a US$1.9 trillion stimulus package working its way through Congress even as the world’s largest economy was improving rapidly. As a result, yields of 10-year U.S. Treasuries climbed 35 basis points. Yields of benchmark 10-year government bonds in other major bond markets rose in sympathy; in the U.K. by 49 basis points, in Germany by 26 basis points, and even in Japan by 11 basis points. Canada was not immune, with its 10-year gaining 50 basis points. Interestingly, the only central bank that seemed concerned by the sharp increase in yields was the Reserve Bank of Australia that, following a 78 basis point rise in yields, stepped in and increased its purchases of government bonds to drive yields back down. Other central banks left their respective quantitative easing (QE) programmes unchanged. The FTSE Canada Universe Bond index returned -2.52% in February.

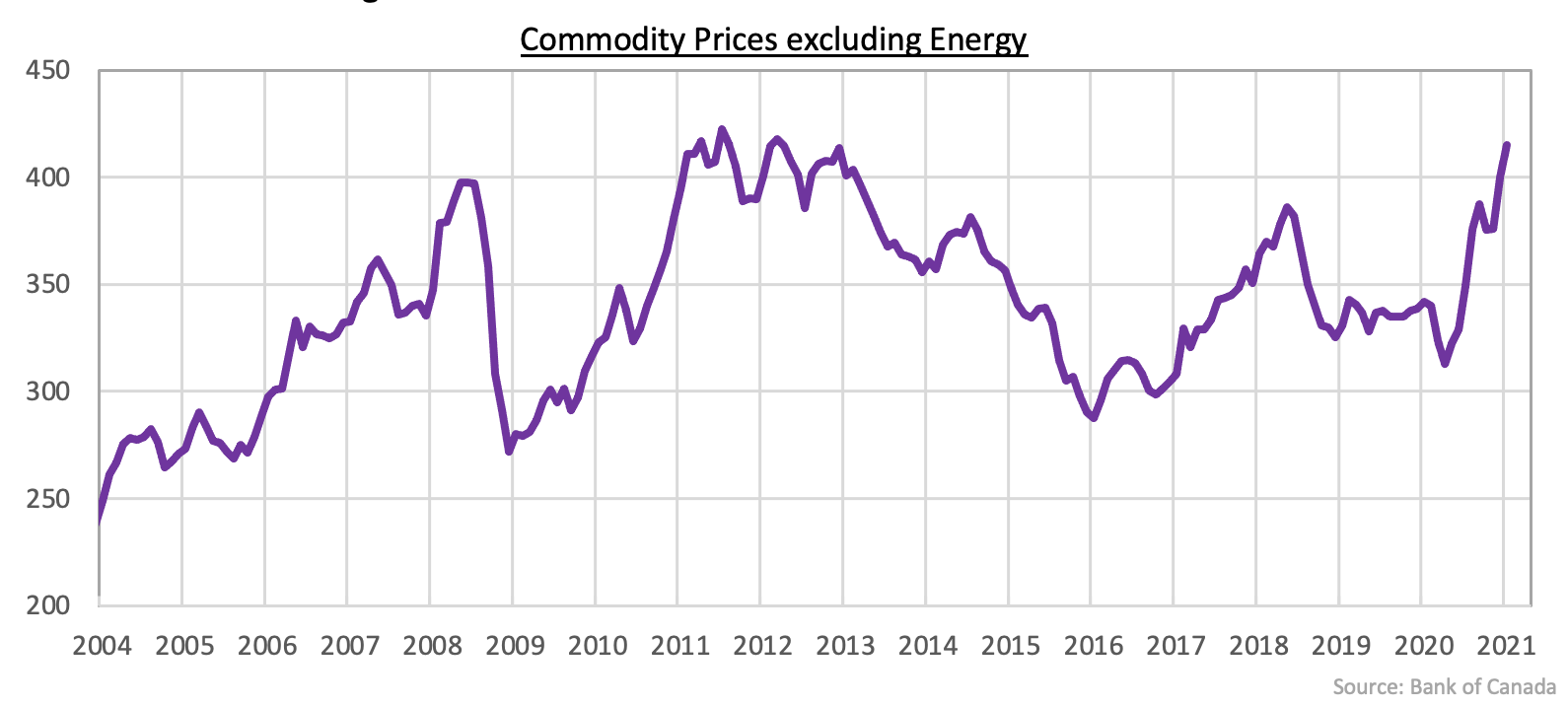

The data on the Canadian economy received during February was mixed. Unemployment rose to 9.4% from 8.8% the previous month, despite a marked drop in the participation rate. A substantial drop in part time jobs due to more stringent lockdown restrictions was the main reason for the rise in unemployment. In contrast with part time positions, the number of full time jobs rose in the period. Other disappointing news saw weaker than expected retail sales volumes for December, although some U.S. based e-commerce sales (e.g. Amazon) were not included in the data. More positively, housing starts rose to the highest level since 2007, with strength in both condo’s and single family homes. Manufacturing sales during January were also robust. Inflation was sightly stronger than expected, rising to 1.0% from 0.7%, but that news was overshadowed by a sharp drop in the core measures of inflation that was subsequently revised to a small increase due to StatsCan making methodological changes in its data series. The Canadian dollar briefly touched US$0.80 on rising commodity prices, but it subsequently subsided somewhat. The price of oil gained $10 in the month, rising to over $62.00 per barrel, while non-energy commodity prices were close to all-time highs.

As noted above, a massive US$1.9 trillion fiscal package was being worked on in the United States during February. That stimulus would follow an earlier stimulus package that saw $600 direct payments to approximately 140 million Americans in January. Many of those payments were quickly spent as retail sales surged higher. In addition, unemployment declined to 6.3% from 6.7% even though job creation was weak and the participation rate edged lower. The housing sector remained strong with prices rising at the fastest pace since 2014. However, the rise in bond yields in the last two months will likely cause mortgage rates to rise, which should reduce demand for housing somewhat.

The yield curve steepened in February as 2-year Canada bond yields rose 15 basis points while 30-year yields climbed 28 basis points. The increase in long term yields would have been larger but for a strong rally on the final day of the month that was the result of buying by index funds. The largest increases in yields, though, were at mid term maturities, as 5 and 10-year yields surged higher by 45 and 50 basis points, respectively. The large increase in mid term yields reflected investors re-evaluating the timing of the Bank of Canada raising rates in the future because of better than expected economic growth. In the United States, the yield curve also steepened, but mid term yields did not experience greater increases than for long term bonds.

During February, federal bonds returned -2.14% as the sharply higher yields caused bond prices to fall. The provincial sector returned -3.23% in the month. Provincial bond returns were hurt by their longer average duration, but that was somewhat mitigated by long provincial yield spreads narrowing 4 basis points. Interestingly, yield spreads on short and mid term provincial bonds widened in the period. Investment grade corporate bonds earned -1.95% in February. Corporate yield spreads moved in similar fashion to provincial spreads, with short term spreads widening while long term spreads narrowed. High yield bonds earned 0.92% in February with energy-related issues again having particularly good returns following the rise in oil prices. Real Return Bonds returned -3.70%, but outperformed nominal bonds with similarly long durations as the breakeven rate of inflation increased in the month. Preferred shares gained 4.21% in part because two insurance companies issued Limited Recourse Capital Notes (LRCN’s) that were expected to result in increased redemptions of preferred shares.

Often after a significant change in yields such as we have seen in the last two months, the bond market pauses and consolidates within a trading range. We would not be surprised if that occurs again over the next few weeks and, accordingly, we are shifting the portfolio durations to more neutral comparisons with benchmarks. However, we believe the longer term outlook is for higher yields as the vaccination rates rise and the pandemic (hopefully) recedes. In addition, we anticipate that the Bank of Canada will reduce its purchases of Canada bonds in the coming months, likely before the federal government has started to reduce its borrowing requirements. If that occurs, it will put additional upward pressure on yields.

The bifurcation of the economy that has seen goods related activity (e.g. manufacturing, housing, etc.) perform quite well in the last few quarters, while in-person services (e.g. restaurants, travel, etc.) have been severely impacted, should gradually disappear as social distancing restrictions are lifted. High unemployment in the service sector will fall only gradually but will not impede a robust recovery because savings rates are high and there is, we believe, plenty of pent-up demand that should propel the economy forward over the next year. The recent rise in bond yields will result in somewhat higher mortgage rates that should cool the housing sector somewhat, but the increase will not be enough to cause a downturn, just a slowing.

We remain concerned that corporate yield spreads are at historically narrow levels even as the economy is still recovering. The risk/reward trade-off seems unattractive and we are looking to potentially reduce the allocation to the corporate sector. We also anticipate that the Bank of Canada will in the next few weeks announce the termination of both its Corporate Bond Purchase Programme and its Provincial Bond Purchase Programme. The former never came close to full utilization but provided a psychological boost for investors following the initial panic that prevailed last March and April. The latter programme was more much more active in acquiring bonds and its termination may lead to some widening in provincial yield spreads, particularly for the smaller provinces.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.