Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

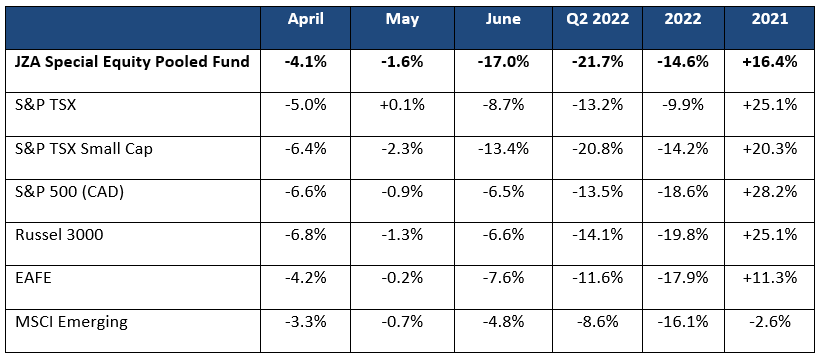

As stated in previous letters, we were never in the camp that inflation was short-term or transitory. The Fed and global central banks have now pivoted from their “transitory” stance and concluded that they need to break inflation with aggressive “front loaded” interest rate hikes. This triggered heavy losses across global capital markets. Within the backdrop of this tightening cycle, stocks suffered their worst first half of the year in over 50 years, as the “free money” era ended. Below are the major global equity index returns and show a considerable pull back. Canada faired better than many other markets because of its higher energy weight.

The poor returns were not just felt in equities, as bond markets also suffered their worst first half on record. The FTSE Canada Universe Bond Index was down -12.2% as of June 30th, 2022. Interest rates pushed higher as record inflation numbers were reported and central banks vowed to reign in inflation via tight monetary policy.

For the most part, commodities held in relatively well in the first quarter of the year but finally succumbed to the pressure of a potential recession. The CRB Commodity Index is still up 25% in 2022, but that is largely driven by the energy sector with oil gaining 40% and natural gas up 48%. In the second quarter the price of copper was down -22% while gold was lower by -7%.

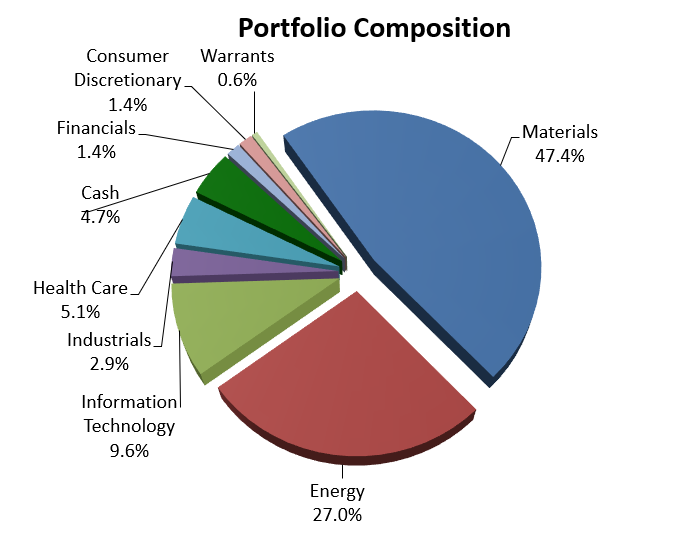

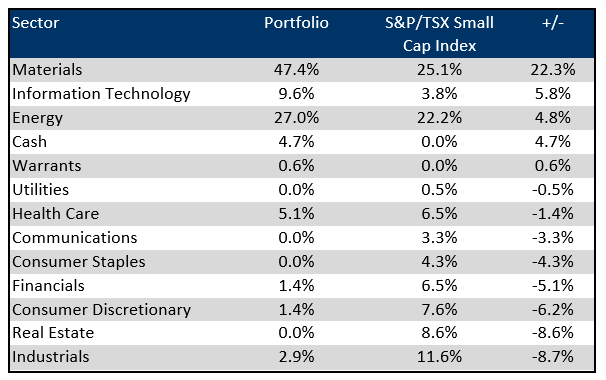

Below are the portfolio and index sector positions as of June 30, 2022:

The three names that detracted most from performance included Copper Mountain, Karora Resources and Arizona Metals. Given the above mentioned pull back in resource stocks, it is not surprising that the detractors are all from the materials sector. Despite reducing the weight of the base metals, the sector downdraft was a significant component of the negative returns experienced in the quarter. These three names collectively cost the portfolio -2.2%.

Copper Mountain is a copper production company with a significant asset in Canada and a developing asset in Australia. It is well managed and is significantly leveraged to the price of copper. In the current environment with the negative funds flow in the space, we have been reducing the position. We are still strong believers in the medium- and long-term copper price but believe our other positions in the space offer better upside and do not have the additional concerns of cost overruns on developing a new project. When we have a more positive market environment, we will consider adding Copper Mountain back.

Karora Resources is a low-cost gold producer operating its integrated Beta Hunt Gold Mine and Higginsville Gold Operations in Western Australia. It has exhibited good growth in production and positive exploration results. With the down draft in mining stocks Karora has also seen selling pressure. Although Karora is technically considered a precious metal stock it also has significant exposure to the nickel price given the high-grade veins located at Beta Hunt. This base metal exposure has most likely added to the sell off in the stock. We have added to the position in the current down draft.

Arizona Metals is an exploration company which has been delineating the Kay Mine Project in Arizona. The Kay Mine is a world class gold-copper-zinc VMS deposit hosted in a good jurisdiction on a combination of patented land claims and BLM claims. The deposit has currently been defined from a depth of 150m to at least 900m and is open for expansion on strike and at depth. We have taken profits in this name but currently hold a weight we are comfortable going forward with at this time.

The three names adding most to performance in the quarter were Enablence Technology, New Stratus Energy and Spartan Delta. The three names added +1.3% to total quarterly returns.

Enablence designs and manufactures optical chips targeting multiple industries and applications. The industry applications that these designs sell into include telecommunications, data center sensor systems (including automotive remote sensing) and medical. The design team is in Ottawa and the company operates a planar light wave circuit (PLC) foundry in Fremont, California. This company has gone through significant changes over the last recent years with multiple management teams and a significant financial reorganization. I have just met the new CEO, Todd Haugen and have come away very impressed. A 30-year veteran in the technology industry with both small and large company experience and having just left Microsoft after 20 years because he felt strongly about the prospects of Enablence. We continue to hold a position in Enablence.

New Stratus Energy is an oil and gas company in Ecuador. In the month of June, New Stratus signed an MOU with the EP Petroecuador (Ecuador’s state-owned oil and gas company) to optimize and speed up the development of its oil field in blocks 43 and 31. Upon finalization of the MOU New Stratus would be able to significantly increase its production base which would be extremely positive for the company. Signing of the MOU is the first step and was well received by the market. We have taken profits on the announcement but maintain a full position.

Spartan Delta is a Canadian E&P company. It has a management that we have followed through various iterations. The company has grown from its inception quickly through acquisitions. They focus on acquiring quality assets that are ripe to be restructured, optimized, and rebranded. Assets of focus would include high-quality, multi-zone, oil and gas operated production alongside a large land base and strategic infrastructure footprint. Recently we have taken some profits in the oil and gas sector but continue to hold an overweighted position in Spartan Delta.

OUTLOOK

As mentioned earlier, all markets have been dragged down by the Fed moving from an easing posture to a tightening posture. Despite the already severe draft down in markets, sentiment appears to be overwhelmingly negative, with many investors now predicting an imminent recession. Many technical targets have been met with respect to exhaustion to the downside.

The first stage of the sell-off in stocks was almost entirely due to the re-evaluations of high multiple growth stocks from the rise in interest rates. Future interest rate expectations have risen sharply on the surge of inflation, which is proving to be far broader based and problematic than the Fed previously had thought. Supply chain disruptions, Chinese COVID shutdowns and ongoing geopolitical conflicts have added to the pressures. Fed Chair Jerome Powell was clear in his recent speech that “the Fed will not let the economy slip into a high inflation regime even if this means raising interest rates to levels that put growth at risk”. This latest tough stance has finally pulled commodity stocks substantially lower. The last sector that still shows positive returns for the year remains energy but recently the sector has also come under pressure.

We believe we are in the final stages of the correction and are optimistic for the second half of the year. With commodities finally capitulating we think we have seen the peak in inflation. The rate increases as well as the incredibly strong US dollar will continue to permeate through the economy creating the slow down that will keep inflation under control. It appears that the bond market agrees, with the 10-year bond yield holding around the 3.00% level, after hitting almost 3.5% in early June.

With this backdrop we have begun to add to our technology weight after being underweight for several quarters. Names added include Lightspeed, Docebo, Magnet Forensics and we have recently increased the portfolio’s position in Tecsys. We are once again overweight the technology sector.

We have reduced the portfolio’s exposure in base metals in favour of gold and have reduced our energy weight. We still have an overweight position in materials and energy. As we globally march towards reducing our carbon footprint, the need for increased supplies of basic materials grows. The underinvestment in the materials sector for the past decade will keep the supply side of the equation very tight. In the energy sector, we expect demand will continue to exceed supply due to the geo-political upheaval and capital discipline being demonstrated by companies. Furthermore, China’s demand for both metals and energy has been limited due to their COVID lockdowns. As they re-open their economy, China’s increased demand for energy and materials will help offset the demand destruction in Europe and North America from higher interest rates and slowing economies.

When evaluating the risks to the portfolio, we consider what could go wrong? Could Chairman Powell overdo the rate increases and cause a more dramatic slowdown than expected? Have analysts reduced their earnings expectations enough or will we be faced with significantly negative earning surprises? Could the war in the Ukraine and Russia find a resolution and cause a further selloff in energy? Are we heading for a period of global stagflation (high inflation, low growth)? Obviously, all these risks are possible, but at this stage in the sell-off, we are confident that the market is pricing in many of these scenarios and the portfolio is well positioned for the predictable recovery.

As always, I look forward to any questions you may have.

Looking forward to the back half of 2022!!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.