Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

After investors suffered through two brutal months and any hope for the traditional year-end (‘Santa Claus’) rally seemed lost, both stocks and bonds got ‘off the mat’ in November, leading to the strongest months this year for each asset class. The catalyst for the advance was the late October inflation report, which showed a continued reduction in both the headline and core U.S. inflation rates. The Federal Reserve then held rates steady at their Nov. 1st meeting and, in the follow-up press conference, Fed Chairman Jerome Powell indicated that the risks between higher inflation and lower growth were relatively “balanced.” Investors read into only one part of that statement and immediately jumped to the view that the Fed was done raising interest rates and would, in fact, start reducing rates as early as the second quarter of 2024. That was enough to force the bears to cover their short positions on stocks and bonds and bring cash in off the sidelines. After seeing 10-year U.S. bond yields almost reach 5%, bonds rallied sharply with yields dropping below 4.3% at one point and bonds having their best month in almost fourty years! Stocks followed suit, with the S&P500 Index rallying over 10% off the late October lows, lead once again by the tech sector, which had been the biggest casualty of the rate hikes in 2022. The Nasdaq100 Index surged higher with a gain of over 13% from the late October low. Smaller cap stocks, which had lagged the overall market this year, also had a sharp recovery as measured by the Russell200 Index, which jumped over 8% to push back into positive territory for the year. Despite weakness in the ‘heavy weight’ energy and financial sectors, even the TSX managed to rally over 7% off its low. Investors were clearly looking at only one part of the story, that being the bullish story of a peak and subsequent decline in interest rates. Mostly forgotten has been the reason why inflation is receding and interest rates might be heading lower, that being weaker economic growth and the consequent negative impact on corporate profits. Those risks were highlighted in the earnings reports for the major retailers such as Lowes, Home Depot, Walmart and Target. Even some of the broad-based tech players, such as Cisco, Texas Instruments and Palo Alto Networks, talked about longer lead times for sales to industrial clients.

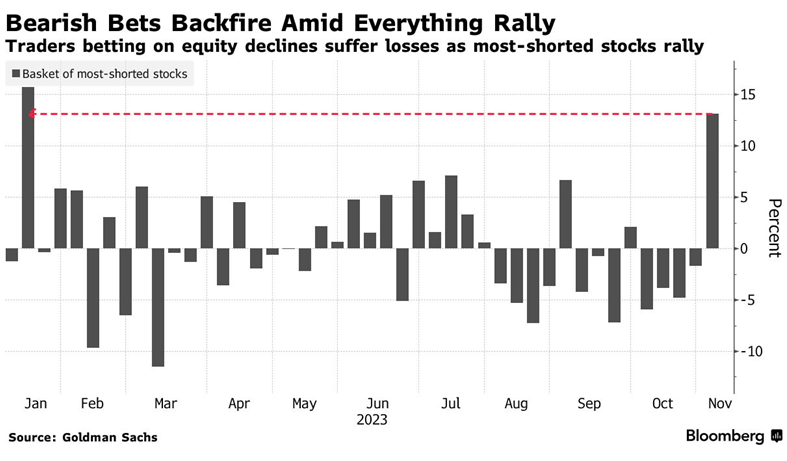

But this was a rally fueled by FOMO (Fear of Missing Out) and short covering by fast-money quants like commodity-trading advisers (CTAs), which were sitting on a $302 billion record short bet in bonds. Economic considerations were put aside in this ‘short-cover rally’ which saw a shift from fundamentals to technical factors as well as the return of corporate buybacks, large systematic demand in both stocks and bonds, short covering in popular thematic shorts and an increase in record low levels of net hedge fund exposure to these markets. This rally could continue into year-end as tax-loss selling is mostly done and the short positioning of CTAs in stocks alone could also lead to over $80 billion S&P500 futures buying if this upside momentum persists. The quality of the advance has also been a bit suspect as chart below shows how the basket of most heavily shorted stocks had their best week since January in mid-November, supporting the view that there was a bit of a ‘buying panic’ aspect to the recent rally.

But this type of short-term buying can run its course relatively quickly. In order to believe we are entering a new bull market in stocks, an investor really has to subscribe to the view that the economy will slow down (soft landing) from the aggressive interest rate hikes of the past two years but not actually go into a full-blown recession. We continue to be in the camp that believes the economy is on the verge of a sharper slowdown than most stock market investors might be expecting. Beyond cautious comments from companies about their demand forecasts, November consumer sentiment report from the University of Michigan (UMich) has recession written all over it. The headline index sank from 63.8 to 60.4, down four months in a row with a reading 26 points below the 70-year norm of 86.4. The current reading challenges the narrative about the ongoing resilience in the consumer space. Another way to look at it, the UMich index is below the levels we have seen in every recession over the past seven decades, including the Great Financial Crisis of 2008-09. Buying plans for big-ticket durable goods sagged to a six-month low in November. The percentage of consumers saying that they are out of the car market because of “sharp rise in interest rates” increased to an all-time high. Interest rates are having their expected negative impact on the economy, it is just taking longer than normal due to the ongoing fiscal spending excesses from governments and the reticence of companies to lay off workers due to the difficulties in making many of these hirings during the pandemic.

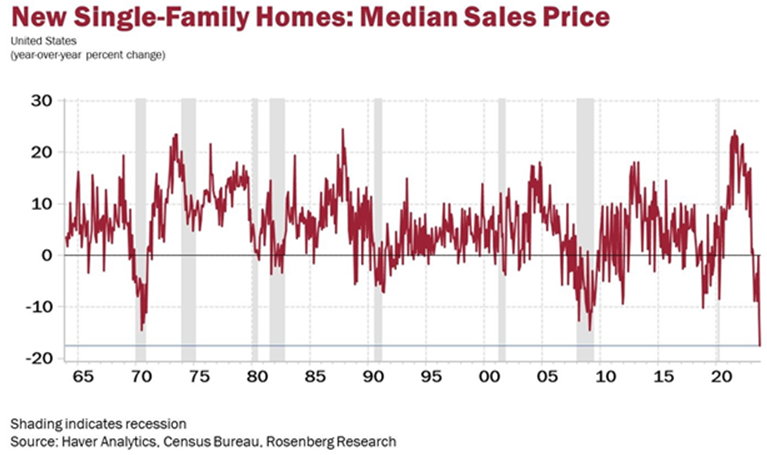

Mirroring the negative comments from both Lowes and Home Depot about consumer spending on housing repairs and renovations, the housing market itself looks to be into a more serious downturn despite the lack of new supply. Higher mortgage rates are taking longer than usual to show up in the housing data since so many homeowners switched to long-term fixed rate mortgages over the past decade. But new purchases need to be financed at current rates and those are restraining demand. The chart below shows the year-over-year change in the median sales price for single family homes in the U.S. The 18% decline is the sharpest drop in over 60 years of data.

While the stock market is typically ‘forward looking’, it seems quite a stretch to already be discounting the end of a recession that we have not even officially entered yet! The more likely path, in our view, is that we continue to see weaker data points but do not move into an actual recession until the first or second quarter of 2024. If the Fed meets market expectations and starts cutting aggressively in 2024, it likely will be against a backdrop of a sharply slowing economy and rising unemployment, which in turn would bring lower inflation. Central bank policymakers, however, won’t cut rates just because the market is expecting it. There will have to be a compelling reason to start easing, and those rate decreases are likely to come slowly, unless something ‘breaks’ in the market or the economy, forcing the Fed into more aggressive action.

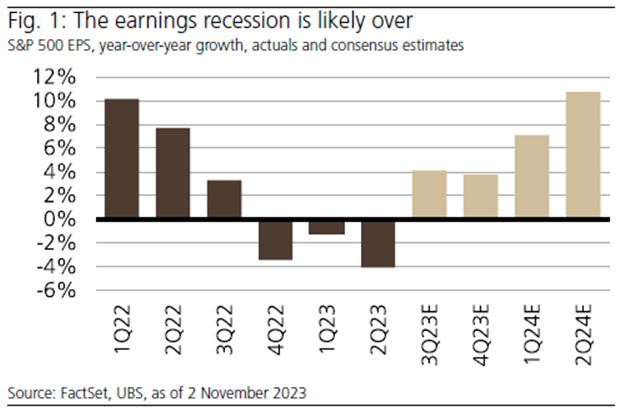

Is optimism the biggest risk in the stock market? With economic growth slowing down, input costs still rising, inflation reducing corporate pricing power and interest rates staying high, it would seem unlikely that S&P500 companies can meet projected profit growth rates over the next year. The chart below shows that, after three straight quarters of negative profit growth, we have seen profit growth turn positive again in the third quarter with a year-over-year gain of about 4%. Consensus estimates are for continued growth over the next three quarters, with year-over-year growth hitting almost 12% by the second quarter of 2024. We think this is far too optimistic an outlook. Falling inflation rates means that companies are losing pricing power on the product side, which had been a big source of profit growth in 2022. Product volumes are expected to remain low due to weaker economic activity but input costs, such as interest rates and labour, will still be higher on a year-over-year basis, meaning that profit margins will remain under pressure and profits will fall short of expectations.

Bottom line is that investors seem to be in a ‘Goldilocks’ world where inflation will continue to come down, central banks will start to cut interest rates and yet the economy will somehow retain enough strength to push a double-digit gain in earnings in 2024. Meanwhile, stock market valuations have risen back towards record highs and bullish sentiment has followed suit. So how do we weave all of this information into a coherent investment strategy for the rest of this year and 2024?

While we are still slightly overweight bonds in balanced portfolios, we are not as bullish as we were just a month ago, when the 10-year U.S. Treasury bond touched 5%. Our target yield over the next year is in the 3.5-4.0% range. Given the continued need to finance massive fiscal deficits, the term premium for bonds should stay at this new, higher level of 1.5-2.0%. Combined with a 2% inflation target gets us to our yield target. That was a great potential return when the 10-year yield was 5% but, having rallied over the past month to 4.3%, the upside for bonds has been reduced. However, we see bonds as a great hedge against stocks in any portfolio as they would rally if growth comes in weaker than stock market expectations, while also providing strong potential for positive returns and higher income than they have provided in over a decade.

On the stock side it is a tougher call. Given our very cautious view on the economy we are underweight all of the cyclical groups including financials, transportation, industrials, consumer discretionary and basic materials. We see those sectors as having the biggest risk of earnings disappointments as economic growth fails to meet expectations. However we recognize the bullish implications from the fact that interest rates have now peaked for the cycle. This will support continued flows into stocks from money market and other cash substitutes. The top sectors that are investing in are those where the stocks have less economic sensitivity and higher than average dividend yields. In Canada, we continue to see the pipeline and telecom sectors as top choices under those criteria. TC Energy, Enbridge, Pembina Pipeline, BCE, Rogers Communications and Telus remain our core holdings in those sectors.

Also, with the expectation of lower interest rates and slower growth in the U.S. we see a weaker U.S. dollar providing a strong backdrop for gold stocks. Gold bullion has finally broken above the US$2000 level while gold stock valuations are at multi-decade lows. The problems that First Quantum and Franco Nevada are experiencing with their Cobre Panama mine highlight the ongoing geo-political risks that arise depending on mine location. Including that caveat, we like Agnico Eagle, B2 Gold, Torex Gold and the Vector Junior Gold ETF (GDXJ) as our core holdings in that sector.

Technology stocks have lead the advance off the lows in the past month and for most of 2023, pushing valuations back towards the late 2021 highs. However, earnings have proven to be resilient in that sector and the continued penetration of cloud services, artificial intelligence (AI), streaming services and the need to continually upgrade the telecom infrastructure support ongoing growth. For those reasons we expect earnings growth to remain better than all other sectors and the premium valuation of tech stocks to remain in play, particularly in a world of falling interest rates. Core holdings in the remain Alphabet (Google), Nvidia, Open Text, PayPal and Broadcomm.

We reduced further our holdings in the financial and energy sectors given macroeconomic and earnings headwinds but retain underweight positions in those sectors due to their historically low valuations. We will look for opportunities to add to those names as weaker economic growth becomes built into earnings expectations. The overall position of stocks remains underweight, due primarily to low weights in the big cyclical sector such as energy, financials and industrials. Cash therefore remains higher than normal (5-8% range in most portfolios). Fortunately, cash returns are now higher than they have been in over 15 years and are therefore not a bad place to hold excess liquidity until we see how the economic data unfolds over the next few quarters.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.