Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

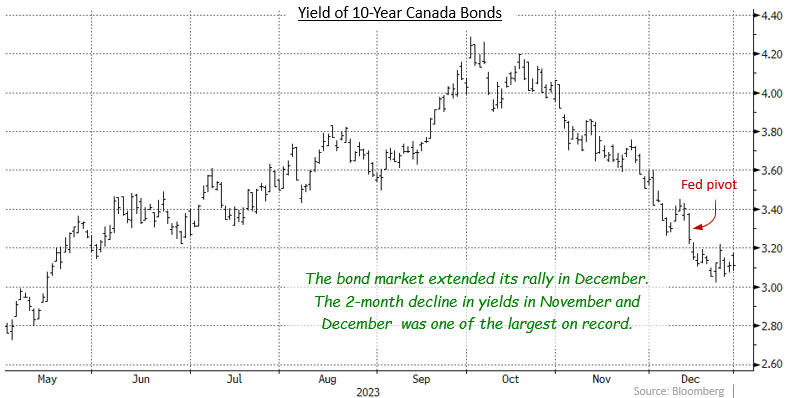

The robust “Everything Rally” extended through December as investor optimism about future interest rate cuts continued to push bond and equity prices higher. The key event in the month was the December 13th meeting of the U.S. Federal Reserve, which left its interest rates unchanged but indicated that rate reductions were likely in the next 12 months. The market reaction was swift and significant as shorter term Treasury bond yields plunged 25 basis points or more that day as some investors speculated that rate cuts might occur as soon as March. Canadian bond yields mirrored the drop in U.S. yields, albeit by a slightly smaller amount. And over the balance of the month, yields in both countries continued to decline. The broad Bloomberg Canada Aggregate and FTSE Canada Universe indices returned 3.52% and 3.43%, respectively, in December.

Economic data received in the month showed the Canadian economy was struggling to grow. Indeed, Canadian GDP failed to expand in October, although the year over year pace of growth increased from 0.6% to a slightly less tepid 0.9% pace. The unemployment rate rose to 5.8% from 5.7% as the 36,000 person increase in the labour force overwhelmed robust job creation of 24,900 positions. Adding to the gloom, housing starts were weaker than expected in November, as starts of buildings with multiple units dropped 26% from the previous month over affordability concerns.

The Bank of Canada met a week before the Fed and left its interest rates unchanged. The Bank said it wanted to see more progress on slowing inflation although it acknowledged the economy was no longer in excess demand. As it happened, inflation in November was subsequently shown to be higher than forecasts due to higher food and clothing prices and the year over year rate held steady at 3.1%. With December 2022’s monthly decline of 0.6% falling out of the next annual calculation, it may be difficult to see inflation declining below 3.0% for the next couple of months.

U.S. economic data received in December showed that the American economy remained resilient. While the manufacturing sector showed some weakness, most other sectors continued to grow. The labour market remained tight as the unemployment rate fell to 3.7% from 3.9% while the participation rate edged upward. In addition, both retail sales and housing starts were stronger than expected. The inflation rate edged lower to 3.1% from 3.2%, but the core rate remained elevated at 4.0%. Overall, the economic data did not present any urgent reason for the Fed to begin cutting interest rates.

Internationally, the only major central bank to adjust monetary policy in December was Norway’s Norges Bank, which raised its rates by 25 basis points for its first increase since September. Other global central banks left their rates unchanged and global bond markets rallied in sympathy with the move in U.S. bonds as investors speculated about the timing of future interest rate cuts by other central banks.

The mid term sector of the Canadian bond market enjoyed the largest moves in December, with 5-year and 10-year bond yields falling 47 and 46 basis points, respectively. The 5-year yield, which is of crucial importance for setting mortgage rates, finished 125 basis points below the peak hit in early October, closing at a level last seen in the Spring. With money market yields remaining above 5.00%, 2-year bond yields declined only 32 basis points in the month. The yield of 30-year bonds fell 35 basis points but remained lower than those of shorter term issues. In the United States, there was little difference in the yield changes for different maturities: the yields of bonds ranging from 2 years to 30 years declined between 45 and 49 basis points in December. As in Canada, lower bond yields are driving down U.S. mortgage rates, with 30-year mortgage rates more than 100 basis points of their recent peak. In contrast with the Canadian market, 30-year Treasuries have yielded more than 5-year and 10-year Treasuries since September.

Federal bonds earned 2.83% in December as the steep decline in yields generated good gains in bond prices. The provincial sector, which has a significantly longer average duration, returned 4.22% in the month. Investment grade corporate bonds gained 3.27% in the period, helped by an average 14 basis point narrowing of their yield spreads versus benchmark Canada bonds. The compression in corporate yield spreads was particularly large in short term issues as investors scrambled to lock in attractive yields before the Bank of Canada cuts interest rates. Non-investment grade bonds earned 3.16%, helped by the risk-on market sentiment. The Real Return Bond index gained 3.67%, which was well behind what nominal bonds of similarly long durations earned. Preferred shares, following an outsized gain in November, earned only 0.82% in December.

As noted last month, we are concerned that the recent bond rally may have gone too far. We are not convinced that inflation will continue to quickly fall to the 2% target, in part because the comparison with price moves last year will be more challenging in December. As well, the sharp drop in bond yields has loosened financial conditions markedly, with lower mortgage rates being an obvious example. That means there is less pressure on the Bank of Canada to reduce interest rates. In addition, we think investors have not yet focused on how much (or how little) the Bank will lower rates when it does begin to loosen monetary conditions. The Bank has suggested that its estimate of the neutral rate, which is neither stimulative nor restrictive, may be revised higher. If the Bank ultimately only lowers its overnight target rate to 3.00%, it is difficult to see great value in long term Canada bonds yielding roughly 3.25%. Accordingly, we are keeping portfolio durations close to benchmarks as we await more information on the economy and inflation.

While we believe the rally may have gone too far too soon, we do not believe it is likely to fully reverse. The high yields seen in October will likely prove to be the peak ones for this cycle. The yield curve remains steeply inverted between 1-year and 5-year bonds, and relatively flat for longer maturities. We continue to look for opportunities to lock in attractive yields by extending out of very short term bond holdings into 3-year to 5-year bonds.

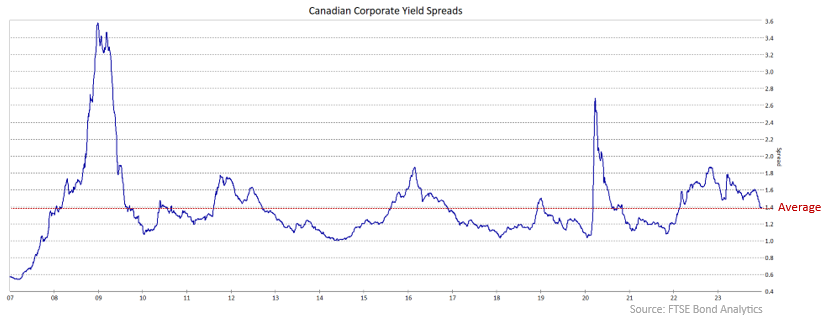

Sector wise, given the need for interest rates to remain high for several more months, we remain cautious about corporate bonds and believe the current level of yield spreads does not properly reflect the level of risk in the economy. As can be seen in the chart below, the recent narrowing of corporate yield spreads has brought them back to the average since the Great Financial Crisis. That seems unduly optimistic given the tepid pace of economic growth and the potential for the Bank of Canada to keep monetary policy restrictive for several more months. We are particularly cautious regarding real estate issuers given their elevated leverage and the need to adjust cap rates to reflect current interest rates and bond yields. In addition, there is a concentration in equity market gains, particularly in the U.S. S&P500 where seven massive tech stocks are dominating the price performance of the other 493 index constituents. Any correction in equities will likely cause corporate yield spreads to widen noticeably.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.