Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

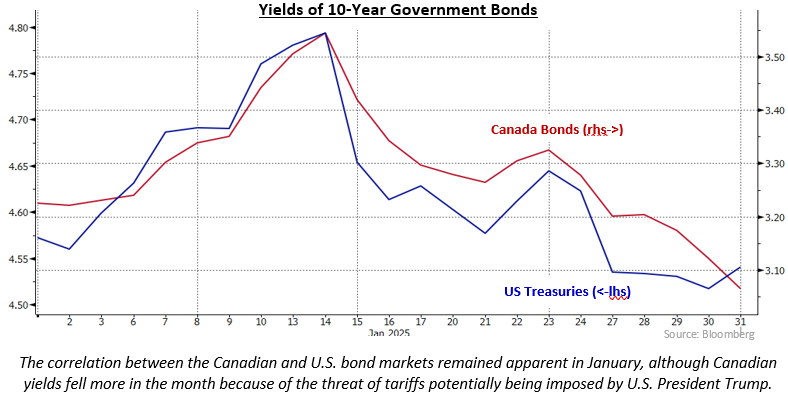

Bond market volatility remained elevated in January, with yields fluctuating in unusually wide ranges. In the first half of the month, investors were focused on the potential for the incoming U.S. administration’s policies to cause higher inflation while failing to address the massive budgetary deficit. Bond yields moved sharply higher notwithstanding the U.S. Federal Reserve’s recent interest rate reductions, and the yield of 30-year U.S. Treasury bonds briefly rose above 5.00% for only the second time since the 2008-2009 financial crisis. Canadian bonds followed the U.S. move to lower prices and higher yields. The selloff was overdone, though, and marginally better than expected core inflation data led to a very sharp reversal at mid-month. Bond prices rebounded over the balance of the month and yields fell sharply, finishing below where they started the month. Canadian bond yields fell more sharply than in the U.S. as investors became concerned that the 25% tariffs threatened by President Trump would hurt the Canadian economy. The Bloomberg Canada Aggregate and FTSE Canada Universe indices returned 1.10% and 1.20%, respectively, in the month.

Canadian economic data received in January had less impact on the bond market than usual because of the focus on Trump’s threatened tariffs. However, there were some significant indications that the Canadian economy was strengthening. The unemployment rate declined to 6.7% from 6.9%, partially due to a drop in the participation rate, but also due to 90,900 net new jobs being created, which was the largest increase in nearly two years. The inflation rate declined to 1.8% from 1.9% in the previous month, but would have jumped to 2.3% if not for the temporary GST/HST holiday. In addition, StatsCan’s preliminary estimate for Canadian GDP in the fourth quarter showed it accelerating to a 1.8% annual rate, fast enough to begin using up the economic slack. The Bank of Canada lowered its interest rates by 25 basis points at its January announcement date, slowing the pace of reductions from the 50 basis point cuts of the last two announcements. Of note, at a discussion following the rate cut, a Deputy Governor (who participates in the rate decisions) said that the low interest rates that existed prior to the pandemic were unusual, implying that we are unlikely to see rates that low in the foreseeable future.

In the United States, the economy remained quite healthy. The pace of GDP growth in the fourth quarter was slightly slower than expected at 2.3%, but much of the shortfall was due to disappointing growth in inventories, which can easily rebound in the next quarter. Of note in the GDP details, personal consumption grew at a robust 4.2% pace. The U.S. unemployment rate declined to 4.1% from 4.2% as a result of stronger than expected job creation. Personal income experienced good growth, while personal spending was stronger than expected. Headline inflation was 2.9%, slightly faster than the 2.7% pace of the previous month, but core inflation was 3.2%, marginally less than the consensus forecast of 3.3%. As widely expected, the Fed left interest rates unchanged at its rate setting meeting. In outlining the reasons for its decision, the Fed said it believed the U.S. labour market was in good shape and inflation was no longer improving.

Internationally, the European Central Bank and Sweden’s Riksbank followed the lead of the Bank of Canada and cut their respective interest rates by 25 basis points. The Bank of Japan responded to higher than desired inflation by raising its interest rate by 25 basis points to 0.50%, its highest level since 2008.

The threat of 25% tariffs by the United States caused the Canadian yield curve to steepen as short term bond yields fell sharply, while longer term yields had more muted responses. The yield on 2-year Canada bonds fell 27 basis points, while 30-year bond yields declined only 8 basis points. At 2.66%, the yield of 2-year Canada bonds finished well below the Bank of Canada’s new 3.00% overnight target rate and was clearly anticipating that the Bank would make significant further reductions to counter the negative economic consequences of the tariffs. In contrast, the U.S. Treasury yield curve was little changed, with yields of all maturities finishing within 3 basis points of where they started the month. Consequently, Canadian yields are at, or close to, record differentials below comparable U.S. bond yields, which makes the Canadian bond market less attractive to international investors.

The federal bond sector earned 1.24% in the month as the drop in yields resulted in bond prices increasing. Provincial bonds also returned 1.24%, as their higher yields were offset by their yield spreads versus federal bonds widening slightly because of the potential negative economic impact of the threatened U.S tariffs. Investment grade corporate bonds returned 1.06%, lagging government bonds because the tariff uncertainty caused their yield spreads to increase an average of 4 basis points. Non-investment grade corporate bonds gained 0.61% in the month. Real Return Bonds surged 2.59%, which was markedly better than nominal bonds with similarly long durations. Preferred shares began the year as they had performed in 2024, gaining 2.25% with $1 billion of redemptions in the month spurring reinvestment buying.

Trump’s narcissistic love of attention and willingness to abrogate all established norms, including a trade deal he negotiated in his first term, suggests that we are in for an extended period of volatility. As this is being written, the threatened tariffs have been postponed for 30 days. The threat to impose 25% tariffs on almost all Canadian exports to the United States because of the very small amount of fentanyl crossing into the United States from this country was akin to trying to swat a fly with a very large sledgehammer. But, having successfully forced both Canada and Mexico to respond to his concerns, we suspect Trump will use the threat again at some time. However, having seen some of the potential retaliatory measures, and understanding his country’s need for Canadian oil, gas, and electricity, we believe the 30-day reprieve on the tariffs are more likely to be extended than imposed. The threat of tariffs will remain a significant risk, though, until the massive U.S. fiscal deficit is adequately addressed. In addition, Trump has ordered a review of U.S. trade relationships for any “unfair” practices by April 1st.

If U.S. tariffs are not imposed, we believe the Bank of Canada is close to pausing its series of interest rate cuts. At its next announcement date, March 12th, the Bank may choose to leave its rates unchanged or cut by a final 25 basis points and indicate that it is unlikely to lower them further. Either way, current bond yields have little room to fall further. Only if the United States decides to impose tariffs and commence a trade war, do we expect the Bank of Canada to make substantial reductions from the current level of interest rates. Given the heightened level of uncertainty, we are keeping portfolio durations close to their benchmarks.

The market’s reaction to potential tariffs immediately before they were postponed suggests there is substantial risk to corporate bonds if they are imposed. With yield spreads still relatively narrow, we believe that corporate yield spreads don’t properly reflect this risk and we are reluctant to add to the corporate sector exposure until there is greater clarity (if such a thing exists) regarding Trump’s intentions.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.