Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

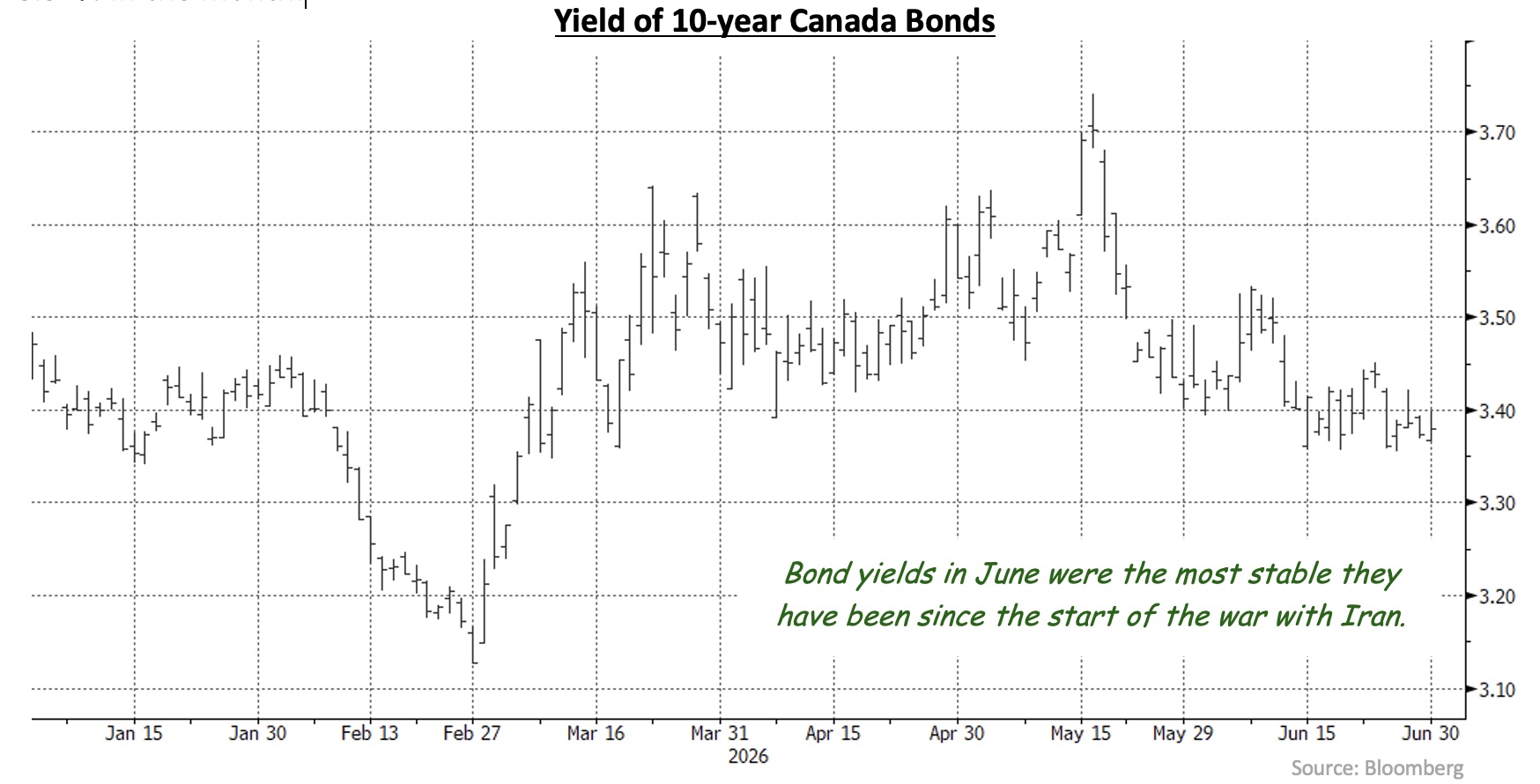

Canadian bond yields edged lower in June as volatility in the month was the lowest since the start of the U.S./Israel war with Iran. The reduced volatility came despite several noteworthy events including a rebound in Canadian economic data, a change in leadership at the U.S. Federal Reserve, the signing of a memorandum of understanding between the U.S. and Iran that led to a sharp drop in the price of oil, and another record breaking corporate bond issue in Canada. The FTSE Canada Universe Bond index gained 0.51% in the month.

Canadian economic data was more positive than in recent months. Early in June, we learned that the unemployment rate fell to 6.6% from 6.9% the previous month, as the number of full-time positions increased by substantially more than expected. Later in the period, 0.5% GDP growth during April was faster than forecasts and helped raise the year-over-year pace to 1.1% from 0.4%. The better than expected GDP news alleviated recession concerns following two consecutive quarters of small contractions. The pace, though, remains roughly half the potential speed of the economy as the U.S. trade war continues to impact some sectors. CPI Inflation accelerated to 3.2% from 2.8%, but all the increase was caused by the rise in energy prices due to the Iran war. Measures of inflation that excluded energy were more restrained around 2.0% and indicated that inflation was not broadening in the economy. The Bank of Canada left its overnight interest rate unchanged at 2.25%.

In the United States, Kevin Warsh chaired his first meeting of the Federal Open Market Committee (FOMC). Nominated in early March by President Trump, subsequently confirmed by the U.S. Senate and sworn in in May, Warsh replaced Jerome Powell and quickly began making changes at the Fed. Among those changes were a much shorter statement, an absence of forward guidance, and the appointment of five task forces to review various aspects of the Fed’s operations including communications and whether it is using the best sources of information in its monetary policy decisions. The U.S. yield curve flattened dramatically the day of the FOMC announcement as 2-year Treasury yields jumped 16 basis points higher. While Warsh emphasized that the Fed was committed to restoring price stability, the sharp increase in short term bond yields was primarily driven by half of the FOMC expecting at least one interest rate increase before the end of this year, with some members anticipating multiple increases. Longer term Treasury yields declined over the balance of the month as investors were encouraged by Warsh’s emphasis on controlling inflation following five years of U.S. CPI remaining above the Fed’s 2% target.

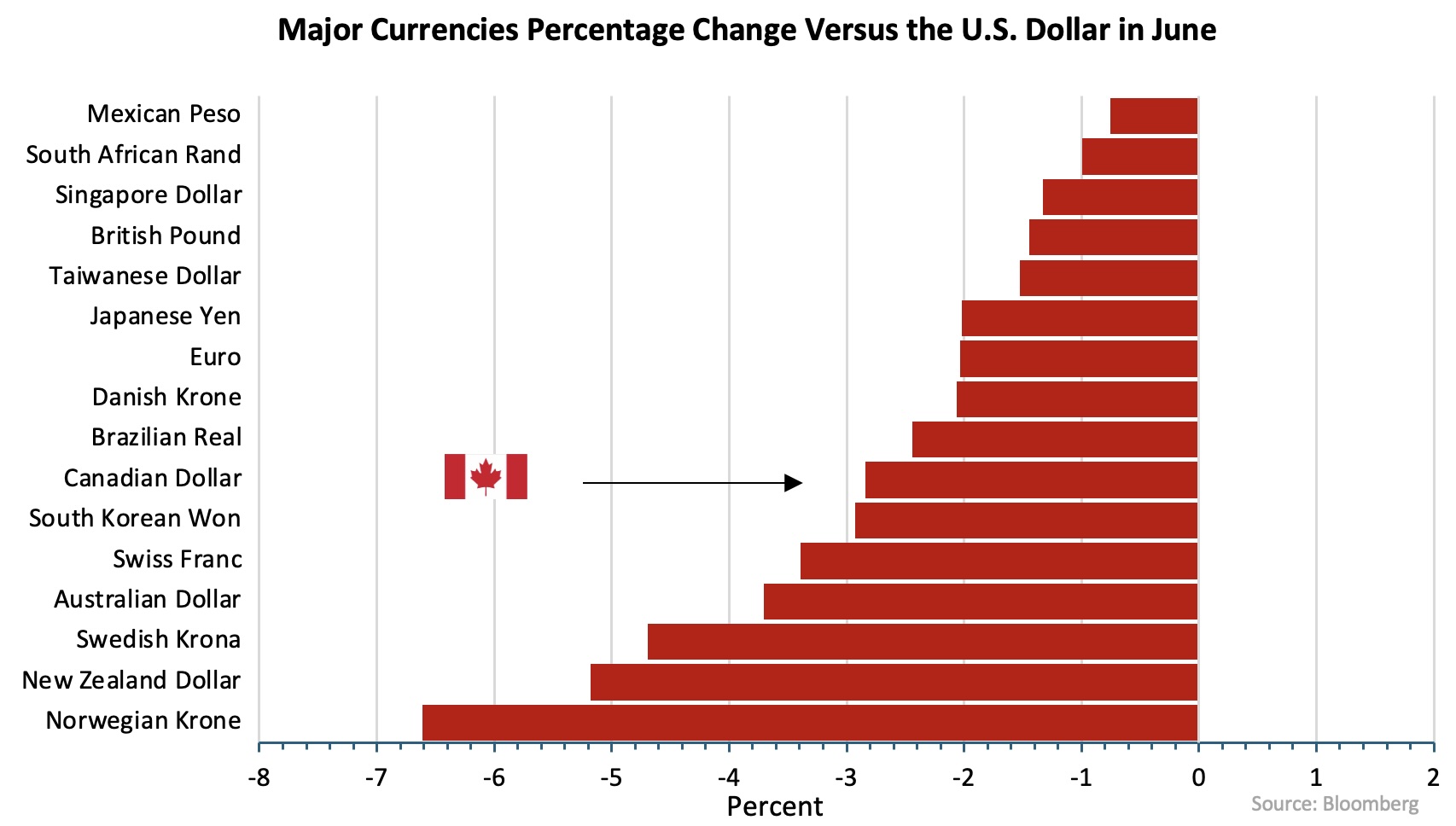

The more hawkish expectations for Fed rate increases this year also led to a rally in the U.S. dollar against all other major currencies, including the Canadian dollar. The Loonie declined 2.84% in June, falling to its weakest level since April 2025.

U.S. data confirmed the resilience of the U.S. economy. The unemployment rate remained at the historically low level of 4.3%, job creation was much stronger than expected, and consumers continued to spend freely. Momentum was favourable heading into the second quarter, with growth in the first quarter revised from 1.6% to 2.1%. CPI inflation rose to 4.2% from 3.8%, as the drop in oil prices was too recent to have had an impact. Of concern, though, core inflation rose to 2.9%, indicating prices were rising rapidly in more than just gasoline.

Internationally, the European Central Bank (ECB) became the first G7 central bank to tighten monetary policy because of inflationary pressures caused by the Iran war. The ECB raised its interest rates 25 basis points. The Bank of Japan (BoJ), which has been gradually moving away from its Zero Interest Rate Policy, also raised its interest rates by 25 basis points. The increase did little to support the Yen, however, as it weakened to 162.5 to the U.S. dollar following massive intervention by the BoJ in May trying to defend the 160 level.

In early June, the United States and Iran signed a memorandum of understanding (MOU) in hopes of ending the war. Israel was not included in the agreement. The MOU included a ceasefire, a reopening of the Strait of Hormuz, and plans for negotiations regarding the future of Iran’s nuclear enrichment programme. While the ceasefire has not always held, some shipping through the Strait of Hormuz has resumed, which has led to a drop in the price of WTI oil to $70 per barrel, well below the $118 peak hit in May. Despite the sharp decline in oil prices, investors were cautious about assuming the ceasefire would last.

The U.S./Israel conflict with Iran is a good example of asymmetric warfare, with the United States’ and Israel’s substantially stronger military capabilities failing to achieve a success such as regime change or an end to Iran’s nuclear weapons development. In asymmetric warfare, the weaker power often needs only to deny the stronger power a decisive victory, while the stronger power must achieve a clear political success to be considered victorious. The weaker power, in this case Iran, succeeds by prolonging the conflict until the stronger side’s political will erodes. U.S. President Trump wants to end the war quickly because it is very unpopular in the U.S. and may impact the mid-term elections in November. Trump’s desire to achieve a quick end means the U.S. may not gain much in negotiations with Iran.

As noted above, benchmark Canada bond yields edged lower in June. Yields declined between 2 and 4 basis points across all maturities. In contrast, the U.S. yield curve flattened significantly in the month, with 2-year Treasury yields rising 12 basis points while 30-year yields closed 9 basis points lower. The rise in short term Treasury yields reflected greater expectations that the Fed would raise interest rates before the end of this year, while longer term U.S. yields declined as investors reacted positively to Warsh’s emphasis on reducing inflation.

The federal sector earned 0.55% in June as slightly higher bond prices due to lower yields combined with interest income. The provincial sector also earned 0.55% in the period, with wider yield spreads for short and mid term issues being offset by narrower long term spreads. Investment grade corporate bonds returned only 0.40% because the yield spreads on short term corporate bonds (which make up more than 55% of all corporates) widened slightly. New issue activity was very strong, highlighted by a $14 billion five tranche issue from Amazon. The Amazon issue was the largest ever in the Canadian market, breaking the $8.5 billion record set by Alphabet only a month earlier. The 30-year tranches of the Amazon and Alphabet totaled $7.5 billion and have begun alleviating the shortage of long term corporate bonds following the telco tenders over the last year. Total new corporate issuance this year has been quite robust at $120.4 billion, up a remarkable 62% versus the same period last year. Non-investment grade corporate bonds returned 0.61% in the month. Real Return Bonds gained 0.92%, as the rise in CPI created buying interest. Preferred shares declined 0.08%, following two months of strong returns.

As expected, the market has unwound some of its expectations of monetary tightening by the Bank of Canada. We believe it is very unlikely that the Bank will raise interest rates at its next meeting on July 15th and will probably leave rates unchanged over the balance of this year. With the price of oil declining back close to the levels that existed prior to the Iran war, the Bank is likely to look through the temporary rise in inflation, especially as there has been no sign of inflationary pressure broadening in the economy. If the Bank does change interest rates later this year, we believe a reduction is far more likely given the weak state of the Canadian economy. Accordingly, we prefer to keep portfolio durations longer than benchmark levels, although we recognize the currently elevated level of volatility in global bond markets may make it difficult for the Canadian bond market to rally too far.

Corporate yield spreads remain at historically tight levels that do not properly compensate investors for the current level of financial and economic risk. We are also concerned that equity markets, particularly in the United States, are frothy and at risk of a substantial pullback that would cause corporate bonds to sell off in sympathy. We recognize, though, that yield spreads may stay narrow for some time, so we are maintaining a sector allocation that is close to neutral while trying to further reduce credit risk. We also note that the recent AA-rated issues from the hyperscalers, Alphabet and Amazon, are putting pressure on lower rated Canadian issues which should lead to gradual widening in their spreads.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.