Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

Markets were uneven through the second quarter of 2026, with sharp reversals across several commodity-linked sectors. After a strong first quarter for oil and gas, the U.S./Iran truce contributed to a significant decline in crude prices, with Brent falling from a high of $117.63 on April 7, 2026 to $68.69 by June 30, 2026. The magnitude of the correction was somewhat surprising, particularly given the need to replenish global strategic reserves following the closure of the Strait of Hormuz and the persistence of elevated geopolitical risk.

Precious metals, which had been a major source of strength last year, also came under pressure during the quarter. While this may appear counterintuitive against a backdrop of heightened geopolitical uncertainty, rising bond yields and a stronger U.S. dollar weighed on both gold and silver. Gold experienced its weakest quarterly performance since the second quarter of 2013, declining approximately 16% over the period. Copper held up better than most other commodities; however, investor conviction remained limited as seasonal summer weakness took hold and buyers appeared reluctant to step in aggressively.

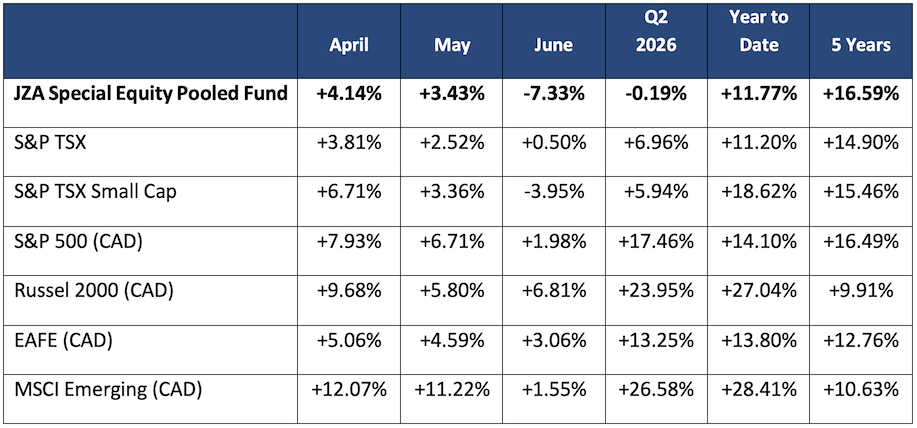

Against this backdrop, the portfolio generated a positive return of -0.19% for the quarter but lagged the S&P/TSX Small Cap Index, which returned +5.94%, primarily due to weakness in gold-related holdings and selected commodity exposures.

The table below summarizes global market returns for the quarter, with the portfolio included for comparison:

Canadian small cap technology and industrials were the strongest-performing sectors in the second quarter, advancing +46.1% and +17.5%, respectively. By contrast, energy was the weakest-performing small cap sector, declining -8.5%. Within materials, the gold sub-sector also came under pressure, falling -15.5% and accounting for the majority of the portfolio’s relative underperformance during the quarter.

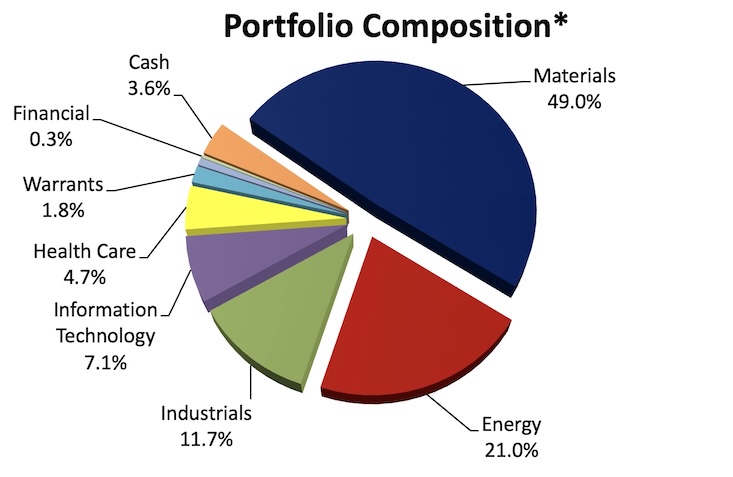

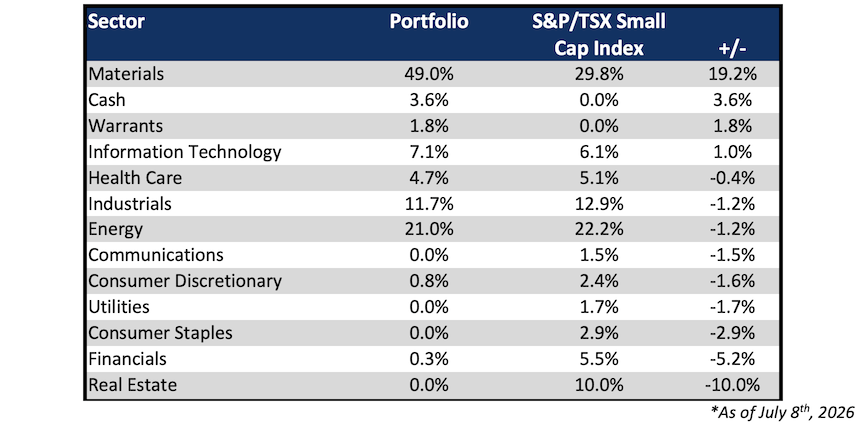

The chart below summarizes sector weights for the S&P/TSX Small Cap Index and compares the portfolio’s sector positioning against the benchmark’s GICS classifications.

The three largest detractors from portfolio performance during the quarter were GoldQuest Mining Corp., Tenaz Energy, and Newcore Gold. Collectively, these holdings reduced quarterly performance by approximately -2.4%.

GoldQuest operates in the Dominican Republic, where it discovered the Romero Deposit in 2012. The project has a robust historical pre-feasibility study that does not include more than half of Romero’s mineral resources and is currently at the mine-permitting stage. In the coming months, GoldQuest is expected to release a Bankable Feasibility Study incorporating updated metal price and cost assumptions, based on a 2,800 tonne-per-day underground mine focused on high-grade gold and copper. While the project has received a temporary halt to activities, stakeholder engagement remains ongoing. We continue to hold the position given the quality of the deposit and our confidence that the local management team can work through the engagement process.

Tenaz Energy is focused on the acquisition and sustainable development of international oil and gas assets. The company is currently the largest operator of natural gas assets in the Dutch sector of the North Sea and develops crude oil and natural gas assets at Leduc-Woodbend in Alberta. Tenaz targets under-optimized and underfunded assets that can generate free cash flow early in their development. We view the management team as experienced and disciplined, with a strong record of acquisitions and technical execution, and we continue to hold the position.

Newcore Gold is advancing the Enchi Gold Project in southwest Ghana, located on the Bibiani Shear Zone, which hosts several large, multi-million-ounce gold mines. The company has an 80,000-metre drill program underway, focused on resource conversion, resource growth, and exploration. The most recent pre-feasibility study, released in June, fell short of analysts’ expectations. We subsequently exited the position as part of our effort to reduce the portfolio’s gold weighting.

The three largest contributors to portfolio performance during the quarter were Enablence, Neo Performance Materials Inc., and 5N Plus Inc. Collectively, these holdings added approximately +3.6% to performance in the second quarter.

Enablence designs and manufactures optical chips used by leading global transceiver companies. The company’s highly specialized optical engineering team produces differentiated designs that reduce insertion loss, increase bandwidth, and improve crosstalk performance. Based in Ottawa, Enablence owns a wafer fabrication facility in Fremont, U.S.A., providing domestic production capacity that helps reduce exposure to global supply-chain disruptions and supports a reliable source of critical components. Its chip designs target AI hyperscalers, datacom, telecom, and automotive LiDAR applications. The company is now well funded and operating in a growing segment of the market. We continue to hold our position.

Neo Performance Materials Inc. is a Toronto-based global manufacturer of advanced industrial materials, rare earth magnets, and specialty metals. It is one of the few fully integrated rare earth producers outside China, serving fast-growing end markets such as electric vehicles, wind turbines, and industrial automation. The company operates through three primary segments: Magnequench, Chemicals and Oxides, and Rare Metals. We continue to hold our position.

5N Plus is a Montreal-headquartered global producer of specialty semiconductors and ultra-high-purity performance materials. The company operates through two primary divisions: Electronic Materials and Performance Materials. Its key target markets include space and defence, renewable energy, and health care. The company is experiencing significant commercial acceleration, and we continue to view its end-market exposure favourably.

We have tempered our enthusiasm slightly following last year’s exceptional market gains, as some consolidation was both reasonable and expected. At the same time, the global backdrop has become more complex, with the U.S./Iran conflict continuing to create geopolitical headwinds and periodic volatility. In the United States, a new Federal Reserve governor, the approaching midterm elections, and the likelihood of heightened political rhetoric from President Trump all add to the potential for market uncertainty. Trade policy also remains an area to monitor, as the U.S. has declined to formally renew the USMCA/CUSMA agreement, leaving trade relations among the three countries subject to annual reviews ahead of the scheduled 2036 expiration.

On the other hand, the economic backdrop remains resilient and provides reasons for optimism. In the U.S., the labour market improved meaningfully through the spring, with the three-month average of payroll gains rising to approximately 188,000 by May, while June unemployment remained relatively low at 4.2%. Inflation pressure also eased late in the quarter, with June CPI declining 0.4% month-over-month and core CPI up 2.6% year-over-year. Globally, manufacturing activity remained in expansion, with the J.P. Morgan Global Manufacturing PMI at 52.2 in June, marking the eleventh consecutive month above the 50.0 expansion threshold. Combined with ongoing investment in AI infrastructure, defence, electrification, and supply-chain security, these trends support a constructive outlook for future global growth and remain broadly aligned with the portfolio’s exposure to select technology, industrial, and critical materials companies.

We have reduced the portfolio’s gold weighting but remain overweight. We continue to believe the U.S. dollar is in a longer-term downtrend, while the risk of further rate increases should diminish as commodity prices have corrected and inflation data continue to normalize. Within gold, we have concentrated our exposure in what we view as higher-quality projects with a credible path to potential takeout opportunities.

Our broader commodity exposure is now more balanced across base metals, oil and gas, and precious metals, although copper remains the portfolio’s most significant overweight. Security of supply remains a central theme. While softer near-term demand may create volatility, the long-term supply outlook remains constrained, supporting our constructive view on copper and related opportunities.

We have also added to the industrials sector over the past several months, with a particular focus on companies tied to defence and national security.

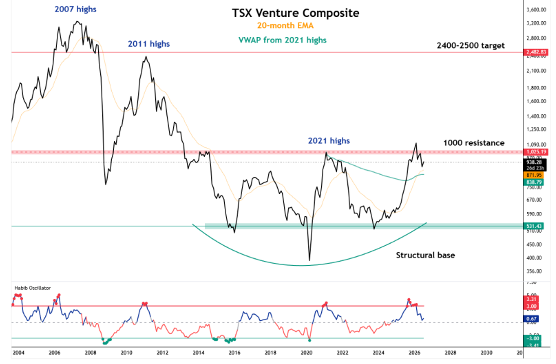

The two charts below highlight longer-term trends that we believe remain encouraging. Both indices have experienced meaningful breakouts followed by reasonable corrections as overbought conditions were worked off. More importantly, both continue to point to a positive longer-term outlook for Canadian small caps.

In summary, while the quarter included some near-term headwinds, we remain constructive on the portfolio’s longer-term opportunity set. We believe the portfolio is well positioned across several durable themes, including critical materials, energy security, defence and national security, AI infrastructure, and select Canadian small cap companies with superior growth prospects.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.