Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

The beginning of 2022 saw bond yields rise dramatically, the yield curve continue to flatten, and credit spreads widen. As we had expected, the year end rally fully reversed when increased inflationary pressures caused the market to price in both the Bank of Canada and the U.S. Federal Reserve beginning to raise interest rates in March. Despite Covid–19 cases and geopolitical conflicts remaining elevated, North America central banks indicated they were willing to look past these factors and focus on rapid economic growth and historically high inflation. The relatively more aggressive monetary policies contributed to a risk-off reaction in financial markets that caused sharp declines in equity markets and resulted in widening of credit spreads. The FTSE Canada Universe Bond Index returned -3.41% in January.

Canadian economic data for the most part had a strong showing in January. Employment increased substantially more than expected with the previous month’s employment figures being revised higher. As a result, the unemployment rate declined to 5.9% from 6.0% the previous month and is now only 0.5% above the low-level set in May 2019. In 2021, Canada created 886,000 new jobs, which was a record year. After losing 3 million jobs at the start of the pandemic, employment rebounded to 240,500 above its February 2020 level. Retail sales were lower than expected, but still saw positive growth. Of concern, the Canadian inflation rate increased to 4.8%, its highest level in 30 years. Inflation has now been above the 2% Bank of Canada target for ten consecutive months.

The Bank of Canada surprised many market participants and held its overnight rate steady at 0.25% at its January meeting. The Bank did indicate clearly, however, that it would be raising rates at its March 2nd meeting unless the economic and pandemic situations unexpectedly deteriorated. The delay in raising rates for six weeks, despite the Bank’s acknowledgment of Canada’s strong economic recovery and high inflation, sparked some less than complimentary allusions to Groundhog Day. In contrast with its clear warning about imminent rate increases, the Bank was rather vague about how it planned to reduce its massive holdings of government bonds amassed since the start of the pandemic. Its uncertainty was likely due in part to it never having undertaken quantitative easing prior to the pandemic, so it also has had no experience in trying to unwind it.

The U.S. economy during January saw employment increase by 199,000, which was much lower than expected and retail sales were also lower than forecasts. Despite these disappointments, the Bureau of Economic Analysis released its first estimate of fourth quarter GDP growth at 6.9% annualized. This, combined with 2.3% growth in the third quarter, meant U.S. economic output had risen 3.1% above its pre-crisis level. Given this strong growth, combined with accommodative monetary policy and substantial fiscal income supports, it was not surprising that U.S. inflation soared to 7%, while the core rate had risen to 5.5%. The headline and core inflation rates were at their highest levels in 40 and 30 years, respectively.

As expected, the U.S. Federal Reserve left its administered interest rates unchanged at its January meeting. Like the Bank of Canada, the Fed is now expected by the market to initiate its first rate hike in March. In contrast with the Bank of Canada, the Fed indicated that it would also begin quantitative tightening (i.e. reducing its bond holdings) at the same time as, or soon after, the first rate increase.

The pace at which the Bank of Canada and the Fed reduce their bond holdings is a major concern for bond investors in both countries. The Bank and the Fed were each very aggressive in purchasing bonds to provide liquidity and lower financing costs from the beginning of the Covid-19 crisis. Now that the two central banks want to reduce their monetary stimulus, they would like to shrink their respective holdings of bonds. The pace of quantitative tightening (QT) will be crucial, because it has the potential to push bond yields substantially higher. We believe the run-off of bonds will probably be accomplished almost exclusively by allowing holdings to mature and not reinvesting them. Actual sales are less likely for practical reasons. However, from time to time maturities may prove too large to avoid some reinvestment and that will provide the central banks with some flexibility to choose which part of the yield curve they would like to benefit.

In January, the Canadian yield curve moved sharply higher in a near parallel fashion with increases of 33 to 38 basis points across the various maturities. In contrast, the U.S. yield curve moved higher but also flattened. The yields of 2-year Treasuries jumped 43 basis points while 30-year yields increased by only 19 basis points. The flattening of the U.S. yield curve reflected the increased hawkish rhetoric regarding the Fed’s next meeting on March 16th. As a result of the different yield curve shifts during the month, Canadian and U.S yields finished January very close to each other at all terms.

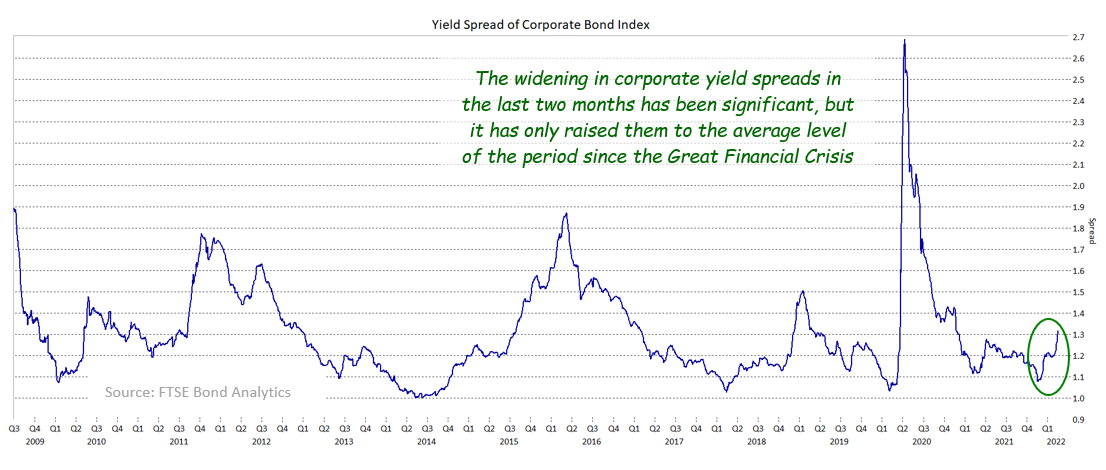

Canadian federal bonds returned -2.34% as rising yields caused bond prices to fall. Provincial bonds returned -4.66% in the month. Provincial performance was hindered by their longer average durations as well as their yield spreads widening by an average of 8 basis points. Investment grade corporate bonds returned -2.94% in January. Corporate yield spreads widened an average 14 basis points in the month as liquidity was relatively constrained. Non-investment grade bonds generally have shorter terms to maturity, higher coupons and higher break-even valuations which helped them outperform investment grade corporate bonds, returning -0.36%. Real Return Bonds returned -6.73%, which was slightly worse than the return on nominal bonds on a duration-adjusted basis. This was due to the market view that central banks should be able to quickly affect a reversal of inflationary pressures. Preferred shares returned -0.02% in a volatile month that saw preferred share rally, sell off, then end the period effectively flat.

In January, both the Bank of Canada and the Fed stated that they plan to begin raising interest rates in March. Given the sharp resultant selloff, we decided to bring the portfolio durations back to neutral versus their benchmarks, as a short term strategic move. We have confidence that the Bank of Canada and the U.S. Fed will increase interest rates several times this year, but we believe that the amount of bearishness, Covid–19 and geopolitical conflicts may present an opportunity where bonds may rally off their current levels providing us with a tactical opening to re-establish defensive durations at more attractive levels.

Canadian and American yield curves have already flattened dramatically, well in advance of interest rate increases, so this cycle has seen a great degree of anticipation. Like the general level of bond yields, it is possible that the yield curves have moved too far, too fast, and they may experience some re-steepening when the central banks actually begin raising rates. However, it is likely that North American interest rates will be increased multiple times in both 2022 and 2023, and we believe yield curve flattening will ultimately continue, with an eventual possibility of yield curve inversion. We are, therefore, maintaining our lean to flattening in the portfolios.

The pandemic-related lockdowns and other restrictions have constrained many types of spending and has generated considerable pent-up demand as a result. This pent-up demand will likely lead to continued economic growth in 2022 and be supportive for corporate creditworthiness. While this environment will present some opportunity for corporate bonds, we are mindful that the likelihood of higher interest rates can be detrimental for risk assets. We are also mindful that, despite the credit back up in January, corporate credit valuation is not cheap versus historical levels. Consequently, we are being patient and cautious about adding additional corporate product to our current allocations.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.