Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

October 31, 2023

For most of the past decade it has been hard to get excited about the bond market. With interest rates at multi-decade lows, the yield on bonds barely offset inflation. Stocks, on the other hand, were experiencing earnings growth, share buybacks which inflated earnings further and a myriad of hot stock stories (cloud computing, AI, crypto and the cannabis stocks in Canada) which drew even more funds into that asset class. Today that narrative has switched in our view. Bonds are looking like an exceptionally great risk-return package in the short term, while stocks are facing an earnings slowdown and probably a recession which could undermine the bullish trends.

Market turns are a much tougher investment call to make and most investors tend to have more ‘trend following’ tendencies. The sharp increase in interest rates in the past two years have ingrained the ‘higher for longer’ mantra into almost every investment commentary and the consensus has driven money out of the bond market, which had always been viewed as a safe haven and a good hedge to risk in the traditional 60/40 balanced fund. We believe it is more informative to look back at history to set expectations. Go no further back than four years ago when central bankers were “not even thinking about thinking about” raising interest rates. That changed quickly in late 2021 as inflation accelerated from a decade of easy money that got ‘super-sized’ during the pandemic. But the reason that interest rates were so low for so long was because economic growth could not get strong enough to create any inflation due to the secular gains in global supply chains, labour mobility and increased productivity. While those trends became distorted and reversed to some degree during the pandemic (i.e. “onshoring” the new buzzword instead of ‘globalization’) we expect the same trends to resume and keep longer-term downward pressure on inflation rates. More importantly, the largest portions of the global economy (US, Europe, Japan) are mature economies and seeing slower growth. The emergence of China as a global powerhouse over the past 25 years offset much of that global weakness. But growth in China is also now slowing down as well. The 8-10% growth rates of the past are history and periods of 4-6% growth will be the ‘new normal’.

The bottom line from all of this is that Interest rates have peaked for the cycle. While we don’t expect any cuts in rates until the middle of 2024, we believe that we should start to see positive performance both from the bond market and the yield sensitive and long duration sectors of the stock market (telecom/utilities/ pipelines/technology). Economic growth has been more resilient than expected due to residual support from the pandemic and massive fiscal spending in the US (CHIPS Act, Inflation Reduction Act). Meanwhile, corporate and mortgage borrowers had extended term during the period of record low interest rates so that the full impact of rising interest rates is taking longer normal. The biggest beneficiaries of the rate increases in the short term have been savers, which has also helped sustain consumer spending. All of those positive impacts are in the process of running out. Savings rates have been run down, the fiscal initiatives are running into gridlock (particularly in the U.S) and the impact of the sharp rise in interest rates will start to impact corporate, consumer and mortgage debt as they roll over. In that environment, we have to be more wary about consumer spending and other cyclical stocks as their earnings will disappoint.

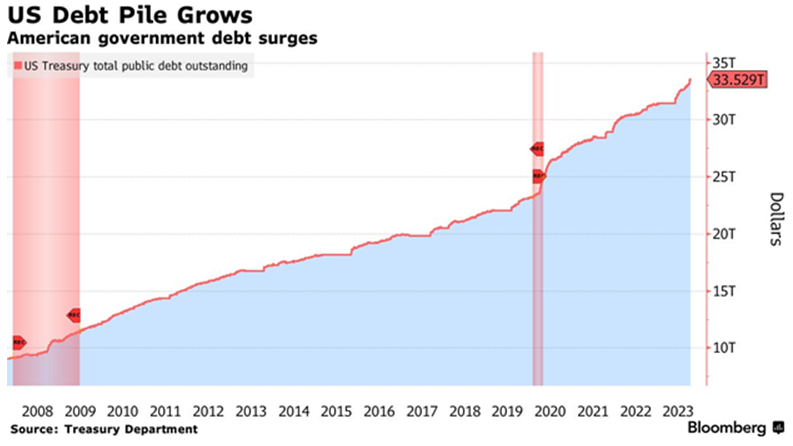

The bond market story is quite different as rarely has it been this bad for bonds. The bond rout has been brutal. Supposedly ultrasafe Treasuries are on track to lose money for three consecutive years, declining 42% over that period. Other bonds, whether mortgage-backed securities or high-quality corporates, have also taken a beating, leaving investors with losses from what are supposed to provide ballast in a portfolio.

But investing is about looking ahead to see what may come next: the end of the bond bear market. While long-term yields have spiked lately—pushing the 10-year Treasury to 4.9% from 4% in August—the Federal Reserve is nearing the end of its campaign of interest-rate increases. The risk-reward trade-off on bonds has also become more attractive as there’s a case for significant gains with far less downside risk, based on “bond math” alone. The 30-year Treasuries would gain nearly 13% over 12 months with a 0.5-point drop in yields, based on current levels, but the bonds would lose less than 3%, including interest, if rates rose by a half-point. One persistent worry for bond investors is that while inflation has been trending lower, it may turn out to be stickier than hoped. Stickier inflation could arise from forces like spending on decarbonization, reshoring of manufacturing, and increased military spending. At the same time, Federal deficits continue to grow, while interest on the debt could soon hit $1 trillion a year. That would make it the largest source of federal spending after Social Security and health benefits—and harder to manage. That need to finance these deficits will probably keep the ‘term premium’ on bonds (i.e. the rate in excess of inflation) higher than it has been. This means that the ‘neutral rate’ of interest will have to be higher. Typically we have seen 3% as the neutral rate (2% inflation and 1% real interest rates), we see the market needing 1.5-2.0% real rates to attract enough capital to fund this. However, with inflation falling back to target levels and more economic weakness expected, we see the yield on 10-year U.S. treasury bonds moving back down to the 3.5-4.0% range over the next year.

On other side of the asset mix, the biggest risk for stocks right now is earnings expectations and the guidance for the next few quarters as economic growth slows further. The consensus on S&P500 still expects 12% profit growth in 2024 over 2023. That seems far too optimistic. We expect much weaker growth over the next few quarters and probably a recession so we don’t see these earnings estimates as achievable. More to the point, earnings are down in the past four quarters despite the fact that economic growth has exceeded expectations. Problem is that wage, interest and other costs have been rising faster than company’s abilities to increase prices, thereby leading to lower profit margins, at the same time as volume growth is slowing. We don’t expect any improvement in those metrics in the near term. Recent results from transport companies such as CN Rail, TFI International, UPS and Texas Instruments are great front end indicators of a slowdown from companies with broad economic exposure. Meanwhile, the big tech companies are the ones taking the biggest stock price hits even though reported earnings in the past week have come in mostly above expectations. Investors initially cheered cloud revenue growth at Microsoft turning higher again (to 29% yr/yr from 26%) but decimated Google for their growth of ‘only’ 22%. A similar hit came to Meta despite a strong beat. Amazon appears to have stemmed the damage for now as their numbers were also a beat. Clearly the bar was set very high for tech and these seem to be the ‘final generals to fall’ in this market decline, since the average S&P stock had already underperformed so far in 2023. That might mean we are coming close to the end of the selloff, particularly if interest rates have peaked.

Our strategy remains unchanged in the short term. We recently added more to our bond holdings, using excess cash to go overweight that asset class. While we remain underweight stocks, we have been adding on recent weakness. Our focus continues to be on stocks with good dividend yield support and/or earnings less aligned with economic cycles. Pipelines and telecom stocks meet both criteria. We have also added to technology stocks on recent weakness since their earnings growth is less cyclical from increasing penetration of cloud services and AI as productivity enhancement tools. They are also ‘long duration’ assets and should therefore benefit more from an expectation peak and subsequent decline in interest rates. Finally, valuation following recent pullback is also less of an issue. Tech should retain premium valuations due to stronger long-term growth than cyclical sectors. But cyclical valuations have also risen. While investors fret about valuations of Microsoft, Nvidia, Alphabet and Apple in the high 20s (on a forward basis), the Canadian rails are trading at almost 23x this year’s expected earnings, so we are not really paying a very big premium now for the superior growth in most large tech companies, particularly in the semiconductors.

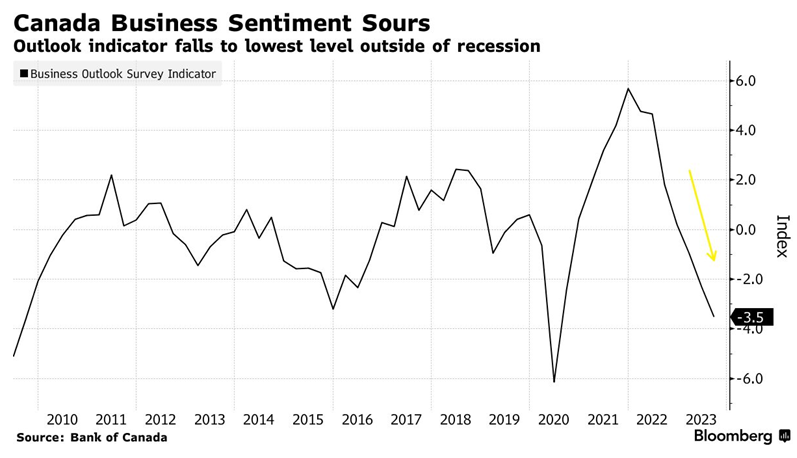

In terms of economic growth, Canada has felt the brunt of the interest rate increases sooner than south of the border. The negative print on second quarter GDP in Canada was the real ‘eye opener’ and the catalyst that has put the Bank of Canada on hold in terms of further rate increases. The effective elimination of 30-year fixed mortgages in Canada shifted many borrowers to shorter maturities and/or floating rate mortgages, meaning that the impact to housing has been felt earlier here. Negative sentiment has also permeated into the business community as the Business Outlook Survey Indicator has moved to its lowest level since the financial crisis (excluding the brief collapse during the pandemic).

Irrationally reactive markets create opportunities in both the short and long term. Stock market investors have many ‘knee jerk reactions’ to events which can create ‘trading opportunities’ in the short term as well as longer-term investments. Oil and gold are an example of a short term trade. The horrific attacks in Israel and the fear that Iran may be behind the attacks has investors worried that war and an oil shortage could develop from this. Much like market reaction after the Russian invasion of the Ukraine in early 2022, oil and other commodity prices spiked, only to give the gains back a few months later despite the fact that the conflict still goes on. The chart action on Canadian fertilizer giant Nutrien in 2022/23 is a classic example of this as the stock surged from $80 to almost $140 and then retraced all of those gains and then some to $74. Selling into these initial overreactions (or buying on the weakness from the collapse of SVB in March of this year) often proves to be a good trading strategy. Much of the initial reaction is often due to large/quant fund positioning, which leads to massive short covering or liquidations. Normality then returns and markets revert to their medium term outlooks. Longer term opportunities are also created from excessive ‘hype’ about stocks or sectors. AI stocks earlier this year as well as SPACS and meme stocks in 2021 and the ‘work from home’ stocks (i.e. Peleton, Docusign, Zoom) in 2020. In the end, rational minds prevail and fundamentals do matter, so it almost always makes sense to use that as making your decisions for investments in the longer-term. However, in the shorter-term, leaning against the trend can often work out to be a good trading strategy.

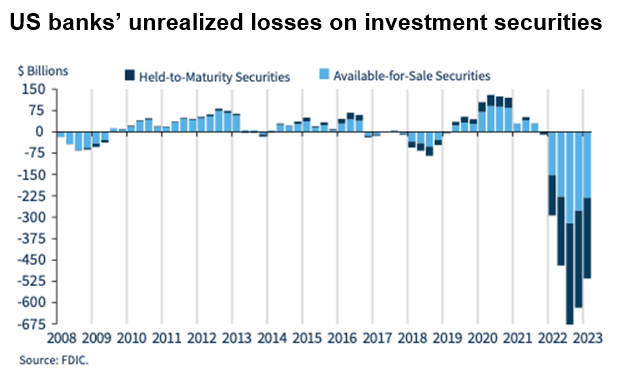

One area where we are still cautious is on the banks, particularly in the U.S. While valuations are at low historical levels, we expect they will face more earnings headwinds in the near term as economic growth slows. That would mean higher levels of loan loss provisions, less revenue from capital markets activities and slower loan growth. On top of that, in the U.S., the banks had been one of the largest buyers of treasury bonds over the past decade as loan growth was insufficient to deploy their assets and so they were able to generate a positive spread on their deposits (rates effectively at zero) and treasury bonds (where they earned as little as 2-3%). The sharp rise in rates blew up that trade this year and lead to the collapse of Silicon Valley Bank. While the regional banking crisis seems to have been controlled once again by the major coming in and scooping of the weaker players, the massive unrealized losses on their bond holdings are going to be a noose around the neck of banks for some time. The chart below shows the unrealized losses on bonds on the balance sheets of U.S. banks has ballooned to over $650 billion from a position of net gains as recently as the third quarter of 2021. Bank of America alone carries over $100 billion of those losses.

Long term opportunities in renewable energy. These stocks ran up to extremely high valuations in 2021 as investors became bullish on the outlook and longer term growth potential in this group versus traditional fossil fuels. Valuation differentials became excessive, with the renewables trading at mid-teens cash flow multiples while traditional fossil fuels were mired at 3-4 times cash flow. Since then the fossil fuels have strongly outperformed the renewable group. Rising oil prices and more ‘shareholder friendly’ strategies (such as increased dividends and stock buybacks) fueled more interest in that group. Meanwhile, rising interest rates were more of a headwind for the renewables space as most companies in that sector are still into major capital spending programs that require debt financing. However, valuation differences have narrowed substantially in the past year and the renewables group is trading at only 7-8 times cash flow while the fossil fuel group may be looking at peak commodity prices. Also, many major global pension funds have completely pulled out of fossil fuels altogether as they look for ‘carbon neutral’ investments. This will keep valuations at a permanent discount to the renewables in our view. That may lead to more corporate activity in the group (i.e Exxon/Pioneer and Chevron/Hess deals this month) but not any valuation growth. Renewables, however, will see growing cash flows from their current capital expenditures and will also receive more equity from the displaced fossil fuel investments. In Canada, Boralex, Northland Power and Brookfield Renewables all stand out as interesting longer term investments in this sector.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.