Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

July 2, 2019

Investors once more reversed course in June, turning to the buy side after a brutal downturn in May which saw stock indices drop about 6%. The reason for the reversal and return to a bullish outlook and increasing risk profiles once again came from very dovish central banker comments that fueled a belief that interest rates would be once again heading lower, reversing the increases of the prior two years. Outgoing ECB Chief, Mario Draghi came out with much more accommodative comments that mirrored the early January ‘pivot’ by U.S. Fed chief Jay Powell, which lead to the booming stock market of the first quarter. Then the June Federal Reserve meeting ended with a much more ‘accommodative’ view on the future movement of interest rates, justifying the 75% consensus market view that there will be an interest rate cut in July and another two cuts over the next twelve months. Investors are also expecting some degree of resolution in the U.S./China trade was, where increased tariffs have disrupted global supply chains and dampened expansionary plans. The economy saw some short-term benefits from these trade conflicts in the first quarter as companies built up inventories before the tariffs were fully enacted, but we expect that those gains will all be given up when second quarter numbers are released.

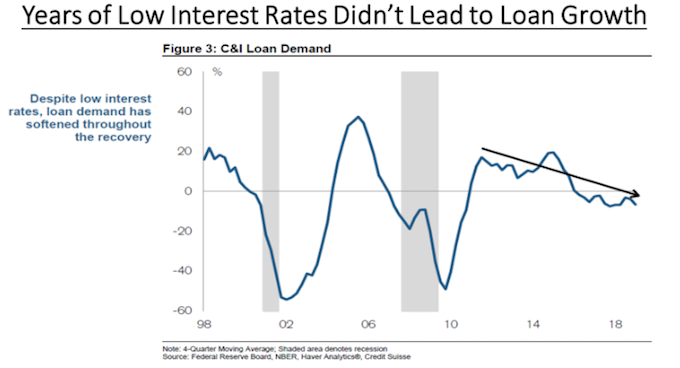

While investors are celebrating expected easier money conditions, shouldn’t we be pointing out that over the past 10 years we’ve seen the most aggressive period of monetary stimulus ever combined with the weakest economic recovery ever? Low interest rates have fueled increasing stock market multiples and high levels of risk taking as investors use a lower discount rate on long-term earnings, which leads to higher valuations. This has been most apparent in the higher growth technology companies, non-cash generating companies such as Amazon, Netflix, Uber and Lyft and speculative business such as marijuana. The low rates have also lead to a huge expansion of low-grade corporate debt. Rather than using those funds for business expansion, much of this debt was just used to fund ongoing stock buybacks, which have hit new records in this cycle. But without the accompanying economic expansion, we are just setting up for a much worse ‘day of reckoning’ when these corporate debts have to be rolled over and equity has to be raised. Monetary policy only works to the degree that it encourages individuals and businesses to take out low interest loans and then put those funds into business expansion or consumption expenditures, respectively. Yet that has not occurred to any large degree. Consumers have paid down their debts while companies have used most of those borrowed funds to buy back their own stock. The question we now have to ask is, ‘has monetary policy lost it’s teeth?’ The chart below answers that question to some degree as it shows how loan growth had steadily decreased over most of the past seven years at the same time as interest rates fell to and remained at record low levels.

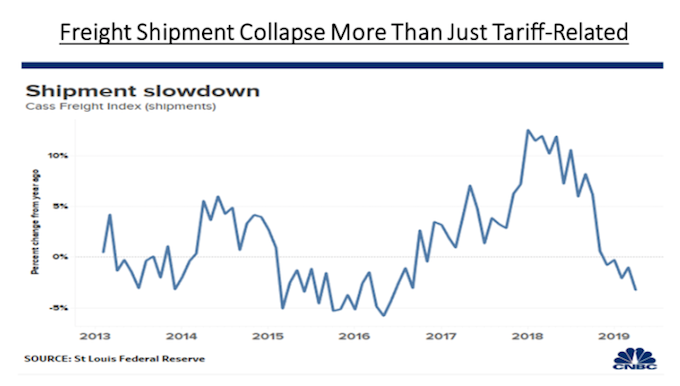

Although stock market investors became much more bullish based on expected interest rate easing, the reality is that the actual economic data has continued to worsen. The OECD organization released its leading economic indicators for May, which remained in recession territory. That was also the 16th consecutive monthly decline. During the prior five episodes since 1974 when the Composite fell to this level for the first time in a business cycle, the US economy was already in a recession. In this cycle, the U.S. received an additional fiscal boost through 2017 tax cuts, which may have delayed the downturn for a few quarters. But the monetary tightening in 2018 has put that decline back in play and we are seeing widespread examples of slowing growth in 2019. The chart below shows how the growth of freight shipments (a key barometer for the strength of the global economy) collapsed over the past year, going negative earlier this year.

Company executives are also getting more nervous about the state of the U.S. economy, with nearly half now expecting a recession within a year, according to the latest Duke University/CFO Global Business Outlook survey. The survey indicated that chief financial officers still believe the economy is weakening and the prospects for their businesses are declining. The reasons for their concerns include tariffs, stronger competition, freight costs and credit risks, among other issues. While the reported economic data has worsened, we expect the weakness to become even clearer as companies begin reporting second quarter earnings over the next month.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.