Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

October 4, 2023

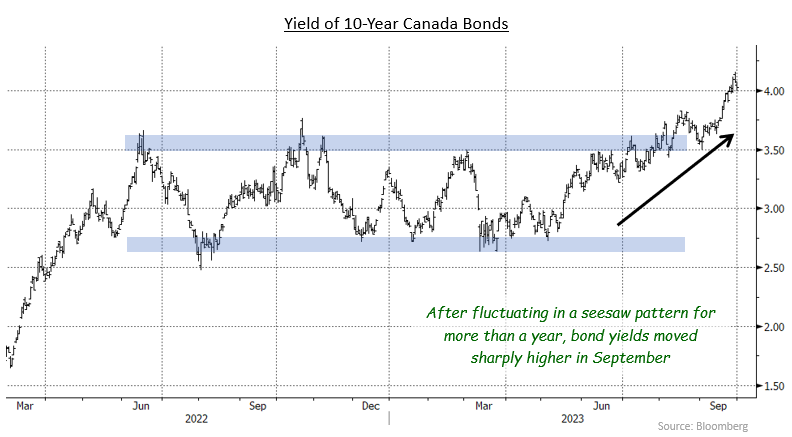

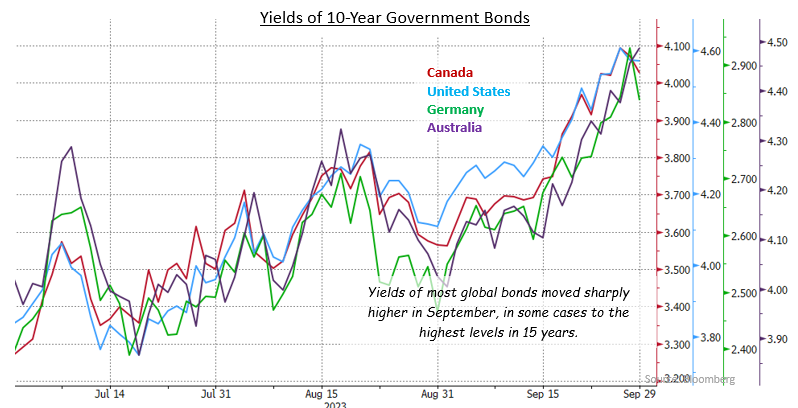

Bond yields moved significantly higher in September. In Canada, the United States, and other major markets investors abandoned the hope that central banks would cut interest rates this year and pared expectations for rate reductions in 2024. With rates anticipated to stay higher for longer, bond investors needed higher yields to compensate for extending the term of their investments. Catalysts for the shift in expectations included a reacceleration in inflation, an extension of the rally in oil prices to above $90 per barrel, and continued resilient economic activity despite the sharp rise in interest rates in the last 18 months. In addition, the U.S. Federal Reserve released new projections that called for another rate increase this year and fewer cuts next year. Also, as the U.S. enters its election cycle, concerns about financing the ballooning U.S. federal deficit increased and made bond investors more cautious. The Bloomberg Canada Aggregate and the FTSE Canada Universe indices returned -2.60% and -2.62%, respectively.

In Canada, the economic data received in September suggested activity was decelerating, but still growing. To some extent, interpreting the underlying strength of the economy was made more difficult by the record wildfire season, labour strikes, and harsh weather events. The key data point in the month was CPI inflation that rose to 4.0% from 3.3%, on strength in gasoline prices, mortgage interest costs and rents. Additionally, core measures of inflation that are closely followed by the Bank of Canada rose for the first time in almost a year. The jump in inflation was larger than expected and reinforced the view that the Bank of Canada was not finished with its struggles to bring inflation back to 2%. In other news, unemployment held steady at 5.5%, but the increase in average hourly wages accelerated to 5.2% from 5.0%, reiterating the need for monetary policy to stay restrictive. Canadian GDP was estimated to have contracted at an annual rate of 0.2% in the second quarter rather than the forecast growth rate of 1.2%, but the market reaction to the news was muted by the hard to quantify impact of wildfires et cetera. Shortly after the GDP data release, the Bank of Canada chose to leave its interest rates unchanged as it wanted more time to assess the impact of prior rate increases.

In the United States, economic indicators were generally positive in September. While the unemployment rate rose to 3.8% from 3.5%, the increase was due to a surge in the labour force as the participation rate rose with more Americans feeling optimistic about finding work. Industrial production and retail sales were higher than expected and business investment continued to rise, in part due to the massive federal fiscal stimulus of the Inflation Reduction Act. As in Canada, inflation accelerated, rising to 3.7% from 3.2%. The Fed chose to pause in its series of interest rate increases but, as noted above, it indicated it expected another increase before the end of the year. In addition, the Fed revised its projections of rate reductions in 2024 to only 50 basis points. Three months earlier, the Fed had indicated that it might cut by 100 basis points next year. The shift in the Fed’s outlook led to a sharp selloff in bonds as well as equities. Equity investors, particularly in the U.S., have largely ignored the ongoing rate increases but that changed with the Fed’s September projections. The S&P 500, for example, declined 4.77% in the month.

nternationally, bond yields also moved higher in September. While the Bank of England and the Reserve Bank of Australia chose to leave their rates unchanged, the European Central Bank, Sweden’s Riksbank, and Norway’s Norges Bank each raised their rates in the month.

The shift in market psychology to believing rates would remain near current levels for an extended period caused bond investors to demand yields closer to central banks’ overnight target interest rates. Given the inverted shape of the yield curve, the largest adjustments in yields were in longer term bonds. The yield of 2-year Canada bonds rose 23 basis points in September, while 30-year bond yields jumped 44 basis points higher. A similar pattern occurred in the U.S. bond market where 2-year Treasury bond yields rose 21 basis points while 30-year Treasury yields rose 53 basis points.

The sharp rise in yields resulted in lower bond prices, which caused the federal sector of the bond market to return -2.07% in the month. The provincial sector fared worse, declining 3.85%, as the longer average duration meant greater impact from the increase in yields. In addition, provincial yield spreads widened 3 basis points with the risk-off environment as well as some deterioration in the fiscal results of some provinces. Investment grade corporate bonds returned -1.77% in the period, thereby outperforming benchmark Canada bonds despite corporate yield spreads widening by an average of 4 basis points. The performance of corporate bonds was helped by their higher yields, as well as slightly lower durations. Non-investment grade corporate bonds returned -0.32%, as their relatively short durations and high coupons mitigated the impact of rising yields. Real Return Bonds returned an average -3.59% as their relatively long durations resulted in larger price declines. However, RRBs fared substantially better than nominal bonds of similar durations which declined roughly 6.00%. Preferred shares rebounded from their weak performance in August, gaining 1.44% in September and again demonstrating their lack of correlation with bonds.

Some months ago, we noted that the fight against inflation resembled the carnival game of Whack-a-Mole. No sooner have price increases in one area of the economy subsided than another sector experiences sharply higher prices. For example, recall the surge in goods prices early in the pandemic, the shift to services such as travel once the economy reopened, and now labour strikes resolved with large wage gains. For a central bank, such as the Bank of Canada, trying to rein in inflation, the problem is that it only has one lever to pull, interest rates. Because different sectors of the economy respond differently in terms of speed and magnitude to higher interest rates, the Bank of Canada will need to keep interest rates at a restrictive level for an extended period to bring inflation back to the desired 2% pace.

Only a widespread slowing of the economy is likely to result in the Bank achieving its objective. While a so-called soft landing might be sufficient, we believe a recession is much more likely to occur because of the difficulty assessing economic activity and inflationary pressures in real time. The Bank will want to avoid tightening to a degree that halts economic growth but does not control inflation, also known as stagflation. Instead, the Bank will need to ensure that inflation is well and truly under control before it can consider easing monetary policy. At this point, it is not clear that the Bank has raised interest rates high enough to accomplish its goal. While some observers are describing the current level of rates as “high”, that is true only if your perspective is limited to the period since the Great Financial Crisis. If we look at the period from 1992 to 2007, when inflation was fluctuating around 2%, it was not uncommon to see the Bank’s interest rates and bond yields at or above current levels while economic growth remained satisfactory.

We believe the recent adjustment of the bond market to rates staying higher for longer may extend somewhat further. Accordingly, we are comfortable keeping client portfolio durations defensively positioned, shorter than their benchmarks. We also believe the maximum inversion of the yield curve has passed, and the yield curve will become rather flat before eventually normalizing. As a result, we have begun adding portfolio exposure to the mid term segment of the yield curve, with additional shifting likely in the coming months. The growing risk of a recession has also made us cautious regarding the corporate sector. In our opinion, corporate yield spreads do not properly reflect the potential for a recession. We believe there is substantial risk that yield spreads widen sharply, perhaps triggered by weakening growth or increased volatility in equity markets. Accordingly, we have lowered the allocation to corporate bonds and reduced the average term of the remaining holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.