Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

October 5, 2021

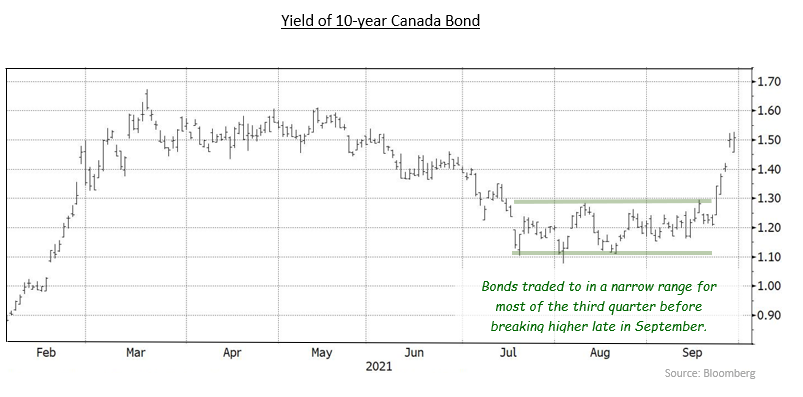

North American bond yields moved higher in September, breaking above the narrow trading range that has been established since July resulting in bond prices moving lower and negative returns on the month. The move higher in interest rates followed many central banks including the U.S. Federal Reserve hinting that they would be reducing monetary stimulus in the coming months. This combined with the progress in mass vaccinations, continued economic recovery and higher than expected inflation all pointed to less need for the extraordinary stimulus currently in place. The FTSE Canada Bond Index returned in -1.40% September.

Canadian economic data was stronger than expected in September. As this is being written, July GDP was revealed to have contracted by 0.1%, slightly better than expectations. Third quarter GDP is now estimated to be 3.5%. Employment increased by 90,200 with full-time positions making up the majority of the growth, while the unemployment rate fell to 7.1%. Retail sales shrank from the previous month, but they were substantially better than the market expected. Worryingly, inflation continued to climb as the year-over-year inflation rate in Canada reached 4.1%, the highest level in 18 years.

The Bank of Canada left its administered overnight rate unchanged at 0.25% at its September meeting. This was fully expected by the marketplace. The Bank continued to claim that inflationary pressures will be transitory, but beyond that comment the Bank remained muted, not wanting to cause any headlines or disruptions in front of the Canadian federal election. In the end, the bond market had no reaction the outcome of the Canadian federal election.

The U.S. economy continued to perform well. Job creation of 235,000 positions was lower than expected but still a solid positive number and the previous month’s employment figures were revised higher. Retail sales surprised market expectations with modest growth on the month. U.S. inflation increased during the period with annual headline inflation up 5.3% while core inflation rose 4.0%. Headline inflation in the U.S. remained at a 13-year high and core inflation was at a level not seen since 1992.

The U.S. Federal Reserve left its benchmark interest rate unchanged at 0.25% at its September meeting, which was fully anticipated by the market. However, the Fed did add to its statement that “a moderation in the pace of asset purchases may soon be warranted”. As a result, the market is now expecting the Fed to begin tapering its quantitative easing (QE) program in November. Additionally, the Fed moved to a more hawkish stance with an increase in its members calling for higher interest rates in 2022. This caused Treasury yields to move higher into month-end as investors considered the impact of potentially diminished demand from tapering of QE and potentially higher interest rates from removal of accommodative monetary policy.

In September, bond yields rose and the Canadian yield curve steepened as 2-year Canada bond yields increased 10 basis points while 30-year yields increased by 19 basis points, so that the spread between the two maturities increased by 9 basis points. Mid-term bonds were even weaker with 5-year and 10-year yields increasing 28 basis points and 29 basis points, respectively. U.S. Treasuries performed similarly to Canada bonds, although U.S. mid-term bonds outperformed as their 5-year and 10-year yields each rose only 24 basis points during the period.

Canadian federal bonds returned -1.20% as the rising yields caused bond prices to decline. Provincial bonds returned -1.80% in the month. The longer average duration of the provincial sector led to its underperformance as yields increased. Investment grade corporate bonds returned -1.06% while non-investment grade bonds returned +0.26%, outperforming higher quality issues during the period as riskier assets continued to perform well. Real Return Bonds, which have quite long average durations, returned -1.37%, which was substantially better than the results of nominal bonds with similar durations. Preferred shares gained +0.87% in the month as redemptions created demand for replacement issues.

We expect to see the Bank of Canada continue to reduce its QE bond purchasing program, with its next reduction likely coming in October. At that point the QE program will enter the reinvestment phase as purchases, which will decline to $1 billion per week, will roughly match maturities of bonds that the Bank holds. In addition, the Bank and the Fed are expected to raise interest rates beginning in the second half of 2022. Since the beginning of the spread of the Covid virus, the central banks’ extremely accommodative monetary policy has led to a steepening of the respective yield curves. Now that the Canadian and U.S. economies are reopening, yield curves should begin to flatten as the central banks take their foot off the gas to normalize monetary policy. This normalization of monetary policy will push the short-mid part of the yield curve higher relative to longer-term yields.

The bond market was trading in a range since July but, in late September, bond yields broke above that range and are now gravitating to higher levels. It is our belief that price inflation will continue to build with economic and social normalization. In this environment, bond investors may push bond yields higher to compensate for the decay of income streams from inflationary pressures. In addition, the tapering of QE and ongoing issuance of government bonds should provide significant upward pressure on yields from reduced demand and increased supply respectively. As a result, we are maintaining a defensive stance in portfolio durations with positioning that is shorter than underlying benchmarks.

Looking ahead to the third quarter we expect, as vaccinations continue to increase across the population and lockdowns recede, the economy will continue to recover. Considerable base and pent-up demand will likely spur robust growth over the remainder of 2021 and in 2022. This strong demand growth will provide firm support for the corporate credit market. While the corporate credit backdrop looks attractive and we are comfortable positioning in the sector, we are mindful of the current expensive valuations of corporate bonds versus historical levels, and therefore we are being very selective in adding to our corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.