Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

October 3, 2018

In issuer news, Standard & Poors downgraded Hydro One bonds to A- during September and retained the “CreditWatch Negative” outlook. When Hydro One closes its acquisition of the U.S. utility Avista, S&P will likely downgrade it again to BBB+. With Moody’s already rating the company Baa1, the approximately $11 billion of Hydro One bonds will fall into the BBB rating bucket when the second S&P downgrade occurs. The yield spread of Hydro One bonds widened by roughly 5 basis points on the news. We do not hold Hydro One bonds, because of credit quality concerns.

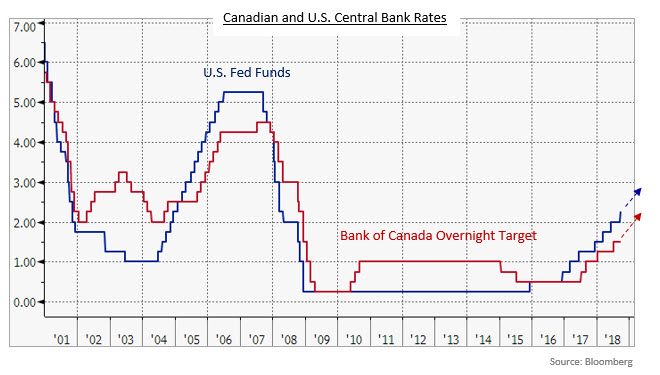

The news that NAFTA has been successfully renegotiated makes it much more likely that the Bank of Canada will raise rates on its October 24th fixed announcement date. Further rate increases, though, will be dependent on what the U.S. central bank does. While the Fed no longer describes its monetary stance as “accommodative”, we believe it will continue to raise short term rates by at least another 100 basis points if the U.S. economy remains operating at full capacity. However, we expect that the pace of the Fed’s moves may slow from the current quarterly cycle. Given the importance of the U.S. economy to the Canadian one, it is not surprising that our respective monetary policies are highly correlated, as can be seen in the graph below. We do not think this is likely to change and Canadian short term rates will follow U.S. ones higher, although perhaps not as rapidly.

.

.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.