Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

October 13, 2017

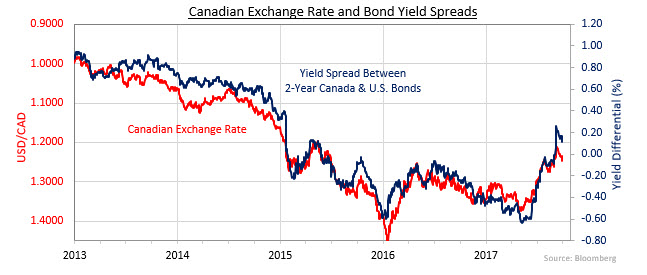

We believe that the Bank of Canada will refrain from further interest rate increases until after the Fed increases U.S. rates again. As can be seen in the chart below, the value of the Canadian dollar has been highly correlated in recent years with the yield differential between 2-year Canada and U.S. bonds. Changes in the Bank’s overnight target rate have significant effect on shorter term bond yields, which in turn influence the exchange rate. In early 2015, for example, the Bank’s surprise rate reduction prompted a sharp decline in Canadian bond yields to below comparable U.S. yields. The Loonie followed suit. As Canadian yields fell further below U.S. ones that year, the exchange rate also fell.

The Bank of Canada’s interest rate increase in September, at a time when the Fed kept its rates unchanged, caused 2-year Canada bond yields to briefly move above U.S. ones and the exchange rate to rise to close to $1.20 (USD/CAD). We believe the Bank of Canada wants to avoid further appreciation of the Canadian dollar so it will not raise rates again until after the Fed moves.

The Fed will probably raise rates at its December meeting, provided there is no significant deterioration in the U.S. economy before then. We anticipate that the small reduction in the Fed’s bond holdings between October and December will not have a noticeable impact on bond yields. Not until the third and fourth quarters of 2018, when the Fed’s bond holdings will decline by $40 billion and $50 billion per month, respectively, do we anticipate that the balance sheet reduction programme will put upward pressure on bond yields.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.