Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

November 10, 2022

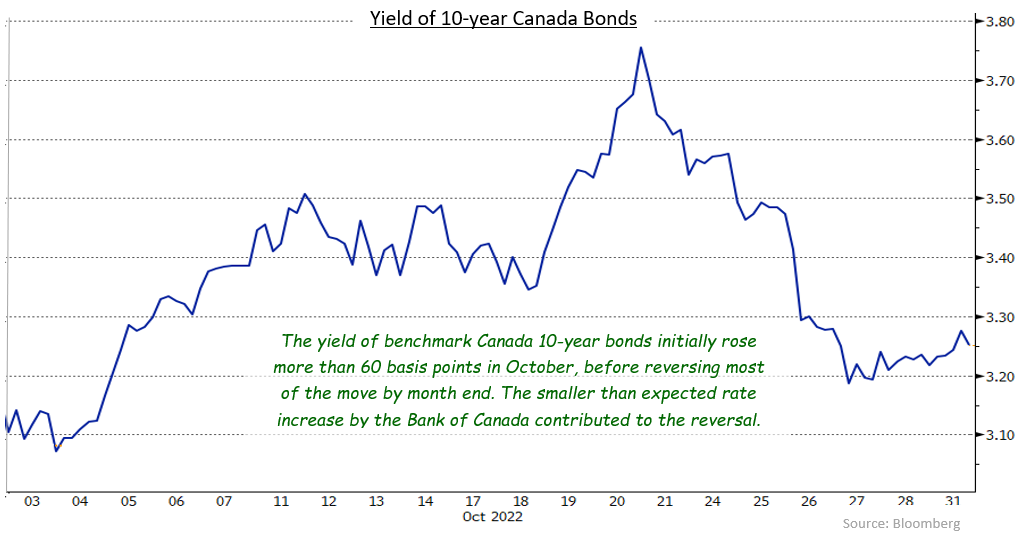

October was a volatile month that saw bond yields rise dramatically for the first three weeks then decline sharply over the balance of the period. In both Canada and the United States yields of benchmark bonds ranging from 2 years to 30 years in maturity initially rose by more than 50 basis points as stubbornly high inflation led investors to anticipate substantially more monetary tightening by the Bank of Canada and the U.S. Federal Reserve. However, both markets turned on October 21st and yields began to fall back. The subsequent drop in yields was significantly larger in Canada as the Bank of Canada surprised the market with a smaller than expected rate increase, which implied it was closer to finishing its series of rate increases. In the end, the FTSE Canada Universe Bond Index returned -1.00% in October.

Canadian economic data was somewhat mixed in October. Canadian GDP grew by 4.0% versus a year ago, but the monthly increase was only 0.1% versus the prior month. Employment increased by 21,100, which was the first jobs increase seen in four months. The increase recovered less than 20% of the jobs lost over the previous three months and was largely driven by an expected rebound in education employment. The positive jobs number combined with a modest decline in labour force participation helped push the unemployment rate down to 5.2% from 5.4%. Retail sales grew more than expected, led by the food and beverage store and auto subsectors. While prices were higher, sales volumes were also higher. Less positively, Canadian home sales declined for the seventh consecutive month as higher interest rates further slowed activity in that sector. In September, Canadian inflation slowed to an annual rate of 6.9%, which was higher than expected and only marginally lower from the 7.0% level of the previous month, despite the aggressive interest rate increases by the Bank of Canada so far this year. The lower inflation rate was driven mainly by a fall in gasoline prices, however gasoline prices began rising again in October.

In early October, Bank of Canada Governor Tiff Macklem made several comments that the Bank would continue to fight inflation aggressively. As a result, the market consensus shifted from anticipating a 50 basis point rate increase to a 75 basis point one. However, as noted above, the Bank chose to raise its rates by only 50 basis points, which led to a rally in short and mid term bonds as investors expected that the Bank might soon stop raising rates and start lowering them. The Bank’s decision to raise by only 50 basis points was predicated on its forecast that growth would soon slow. Curiously, the Bank’s forecast also called for inflation to accelerate slightly in the coming months. Should the economy stop growing and inflation remain excessive, that would indicate a condition known as stagflation.

In contrast with Canada, U.S. economic data was generally robust. Economic activity in America remained strong as GDP during the third quarter grew at a 2.6% pace, which was faster than expected. Job creation was higher than expected, which helped lower the unemployment rate back to the all-time low of 3.5%. Inflation was slightly lower at 8.2%, but the core rate accelerated, suggesting increasing inflationary pressures. The U.S. bond market anticipated that the combination of strong jobs, high inflation and firm growth would keep the U.S. Federal Reserve actively hiking interest rates for the remainder of the year. And as this is being written, the Fed has increased its rates by the widely expected 75 basis points. The Fed’s next meeting is on December 14th when they are expected to raise the Fed Funds rate by 50 basis points.

The Canadian yield curve became slightly less inverted in October as a result of the Bank of Canada slower pace of rate increases. Yields of 2-year Canada bonds rose 13 basis points, while 30-yield yields gained 24 basis points, which brought the longer term yields closer to the shorter term ones. The U.S. yield curve also became slightly less inverted as short term yield rose less than longer term ones. However, as noted above, U.S. yields rose significantly more than comparable Canadian ones, with 2-year Treasury yields up 42 basis points and 30-year yields 50 basis points higher.

In October, the federal bond sector returned -0.67% as higher yields caused bond prices to decline. The provincial sector returned -1.45%. While provincial yield spreads tightened slightly, the longer than average duration of the provincial sector led to larger price declines. Investment grade corporate bonds earned -0.87% as they suffered from higher yields combined with yield spreads that widened an average of 6 basis points. Non-investment grade bonds earned -0.40%, outperforming investment grade bonds due to their shorter maturities and higher yields. Real Return Bonds enjoyed a positive return of 0.61%, substantially outperforming nominal Canada government bonds due to sticky inflation pressures. Preferred shares declined 0.88% despite other risky assets such as equities performing well in the month.

Both the Bank of Canada and the U.S. Federal Reserve have signalled that they will be continuing to raise interest rates through the reminder of the year, and it is important to remember that influencing aggregate demand and inflationary pressures with changes in monetary policy can involve a lag of six months to a year. However, the Bank of Canada has just decelerated while the Fed has continued to hike in 75 basis point increments. Many observers have criticized the Bank of Canada for “pivoting” or slowing rate hikes because of slowing economic growth, despite inflation not yet being under control. The Fed, though, has been adamant that returning inflation to its policy level is an absolute necessity regardless of the American economy falling into recession.

Over the past year, we have held an overweight allocation to short and long term bonds, and an underweight allocation in mid term issues. This has benefited the portfolios as the yield curve flattened last year and eventually inverted this year. Given that the market is beginning to price in a nearby terminal rate for North American central banks and given the significant inversion that has occurred year-to-date, we are now closely monitoring the yield curve and we are looking for an opportunity to reduce or neutralize our yield curve positioning.

Throughout the month we maintained an underweight in duration to protect the portfolios from the impact of rising yields. Central banks around the globe continue to tighten monetary policy to fight inflation. This global tightening is a powerful force and will likely lead to a decline in aggregate demand and a global recession which will eventually result in declining inflationary pressures. We are mindful, however, that monetary policy works with a lag, and so we are comfortable maintaining an underweight duration position until we begin to see inflation fall from its current multi decade high levels.

Corporate credit has been under pressure throughout the year, but we expect to see credit spreads continue to widen and volatility to increase should a recession develop. Consequently, we have reduced the weight and duration in the corporate sector allocation of the portfolios, and we are maintaining a high quality in our corporate holdings. We are also being very conservative in adding new positions and we will be patient about taking advantage of wider credit spreads as they occur in a slowing economy.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.