Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

November 3, 2021

North American bond yields continued to move higher in October, as central banks prepared to reduce the extraordinary monetary stimulus implemented in response to the start of the pandemic. This combined with the progress in mass vaccinations, continued economic recovery and higher than expected inflation resulted in bond prices moving lower and negative bond returns for the second month in a row. The FTSE Canada Universe Bond Index returned -1.05% in October.

Canadian economic data generally had a strong showing in October. Employment increased by 157,100, which helped the unemployment rate fall to 6.9%. Importantly, full-time positions accounted for all the improvement as the number of part time positions fell. As well, retail sales increased more than expected from the previous month. Less positively, inflation continued to climb as the year-over-year inflation rate in Canada reached 4.4%, the highest level in 18 years. That marked the seventh month in a row where CPI printed above the 2% Bank of Canada target level. In addition, August GDP disappointed with an expansion of 0.4%, which was below market expectations of 0.7%. The third quarter GDP growth rate is now estimated to be just 2%.

In October, the Bank of Canada left its administered overnight rate unchanged at 0.25%. This was fully expected by the marketplace. However, the Bank of Canada predicted an earlier closing of the output gap and has changed its “transitory” view on inflation. Despite the slower than expected growth outlook, inflation is clearly the bigger driver of monetary policy decisions now. Governor Macklem stated “it is our job to bring inflation back to target, and I can assure you we will do that”. The market began pricing the Bank of Canada to begin raising interest rates in mid-2022, a quarter earlier than what was expected just a month ago. Rate hike expectations shifted to a 25 basis-point per quarter pace extending into late 2023, which would bring the overnight rate back to its pre-pandemic level of 1.75%.

The Bank of Canada also transitioned its quantitative easing (QE) bond purchasing program straight to the reinvestment phase, which is the period when bond purchases will not exceed the amount needed to replace maturing bonds. This will result in Bank’s bond holdings not growing for the first time since the pandemic began, but also prevent them from shrinking. Bank of Canada Governor Macklem stated that it was reasonable to expect the reinvestment phase to last at least until the first policy rate hike.

The U.S. economy continued to perform well. Job creation of 194,000 was lower than expected but still a solid positive number and the previous month’s employment figures were revised higher by 130,000. Retail sales were higher than expected and U.S. inflation increased during the period with annual headline inflation up 5.4% while core inflation rose 4.0%. Headline inflation in the U.S. remains at a 13-year high and core inflation is at a level not seen since 1992.

The U.S. Federal Reserve did not meet in October, but the minutes of its meeting that were released mid-month stated that employment increased at a “modest to moderate rate in recent weeks” but growth was capped by a “low supply of workers” and most districts reported “robust wage growth”. The minutes also stated that prices were “significantly elevated” and that “many firms hiked prices amid a greater ability to pass higher costs to consumers” as well “Businesses are continuing to grapple with labor scarcity, materials shortages and rising costs”. The market continued to expect the Fed to begin tapering its QE program in November. Similar to Canada, the U.S. Treasury market saw yields rise through October and the yield curve flattened as investors expected the U.S. Federal Reserve to begin raising rates in mid-2022.

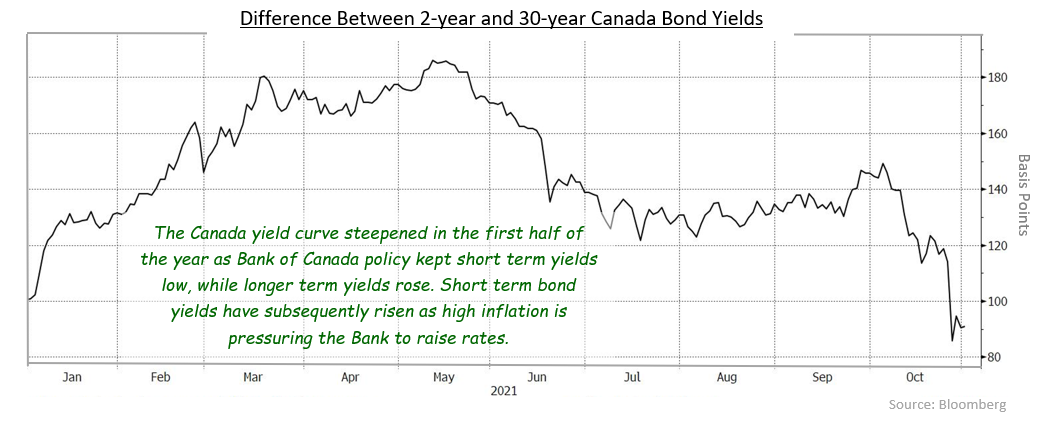

In October, bond yields rose and the Canadian yield curve flattened dramatically in response to the hawkish Bank of Canada announcements. The yield on 2-year Canada bonds increased 54 basis points while 30-year yields increased by 3 basis points, so that the spread between the two maturities decreased by 51 basis points. Mid-term bonds were weak as well with 5-year and 10-year yields increasing 38 basis points and 21 basis points, respectively. The U.S. yield curve also flattened in October, but in a different manner than in Canada. Yields of short term U.S. Treasuries rose only half as much as Canadian short term bond yields, because the Fed was not expected to raise rates as soon as the Bank of Canada. In addition, 30-year Treasury yields actually fell 10 basis points, likely the result of investors switching from short term to long term bonds on a duration-neutral basis. By the end of October, the entire Canada yield curve was higher than the U.S. yield curve, which has not occurred on a sustained basis since the 2008-09 financial crisis.

Canadian federal bonds returned -1.29% as the rising yields caused bond prices to decline. Provincial bonds returned -0.95% in the month, while investment grade corporate bonds returned -0.89%. Interestingly, the yield spreads of both provincial and corporate mid term bonds widened 4 basis points versus benchmark Canada bonds, while long term spreads narrowed. Yield curve positioning following the Bank of Canada’s announcement apparently occurred in both sectors. Non-investment grade bonds returned -0.33%, outperforming higher quality issues during the period as riskier assets continued to perform well. Real Return Bonds returned -1.71%, which was substantially below the results of nominal bonds. This was due to the hawkish Bank of Canada which the market interpreted as committed to quickly resolving the inflationary trend and therefore lessening the need for Real Return Bonds. Preferred shares gained +1.81% in the month as redemptions continued to push prices higher.

The bond markets saw yields continue to trend higher in October as inflationary pressures remained high in North America. As a result, the Bank of Canada stated that subduing inflationary pressures was now its main policy perspective and removal of accommodative monetary policy was in order. The tapering of QE and ongoing issuance of government bonds should provide significant upward pressure on yields. As the Bank of Canada and the U.S. Federal Reserve transition to tighter monetary policy, bond yields should continue to rise from the extreme low levels caused by the pandemic. As a result, we are maintaining a defensive stance in portfolio durations with durations shorter than underlying benchmarks.

Since the beginning of the spread of the Covid virus, the central banks’ extremely accommodative monetary policy has led to a steepening of the respective yield curves which peaked in mid-May. With both the Bank of Canada and the Fed now expected to begin raising rates in the second or third quarter of 2022, yield curves have begun to flatten. We expect this flattening of the yield curve to continue.

Looking ahead to the fourth quarter we expect, as vaccinations continue to increase across the population and lockdowns recede, the economy will continue to recover. Considerable base and pent-up demand will likely spur robust growth over the remainder of 2021 and in 2022. This strong demand growth will provide firm support for the corporate credit market. While the corporate credit backdrop looks attractive and we are comfortable positioning in the sector, we are mindful of the current supply line disruptions and expensive valuations of corporate bonds versus historical levels, and therefore we are being very selective in adding to our corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.