Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

December 6, 2024

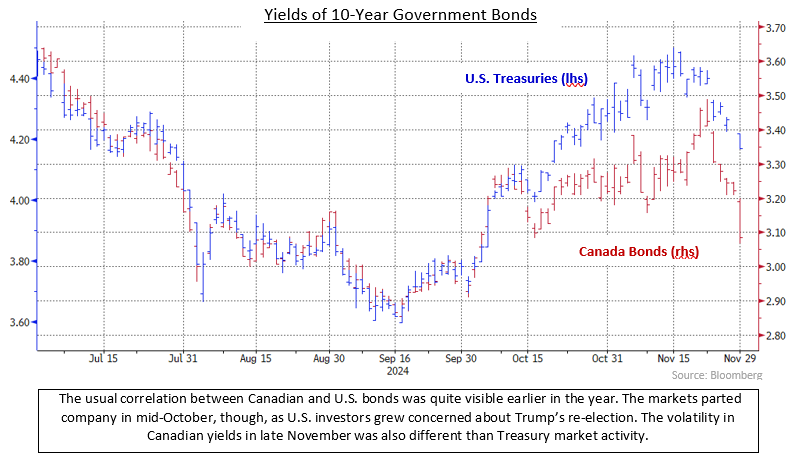

he Canadian bond market experienced a volatile month in November that was dominated by the U.S. elections and its aftermath. A measure of the volatility was the yield of the benchmark 10-year Canada bond that traded in a wide 40 basis point range in the period. Canadian bond yields followed U.S. yields higher for much of the month on concerns that president-elect Trump’s proposed policies would lead to larger U.S. budget deficits and higher inflation. However, the Canadian market staged a very strong rally in the final week of the month to finish with a positive return. The rally was caused by several factors including concerns about the potential negative economic impact of a proposed 25% U.S. tariff on all Canadian imports as well as demand for long term duration bonds due to an upcoming index extension. The FTSE Canada Universe Bond index finished the month with a gain of 1.68%.

Donald Trump won the U.S. presidential election and his Republican party won control of both houses in the U.S. Congress on November 5th. Bond yields in the United States reacted by extending their upward trend that had begun in October as investors were concerned that Trump’s proposed policies of tax cuts and tariffs would result in higher inflation and even larger budgetary deficits. Following the election, financial markets responded to a daily series of announcements of nominations for key administration posts as well as major proposed economic policies. The key consideration for the nominations appeared to be personal loyalty to Trump rather than competency, raising concerns that key economic issues would not be well handled. However, the nomination of the hedge fund manager Scott Bessent as Treasury Secretary on November 25th provided some reassurance that that post would be filled by someone qualified, and that prompted U.S. bonds to subsequently rally.

On November 25th, Trump also threatened to impose 25% tariffs on all imports from Canada and Mexico, as well as higher tariffs on Chinese imports. Canadian bond yields fell in reaction because the tariffs, if imposed, would result in sharply lower growth and possibly a recession. The Canadian exchange rate was also affected by the tariff threat, declining 0.5% against the U.S. dollar in November. Other targets of Trump’s tariffs fared worse, though, as the Mexican peso fell 1.7% and the Chinese renminbi dropped 1.8%.

Canadian economic data received in November showed the economy was performing somewhat below its potential, but not as poorly as some observers had believed. Estimated GDP growth in the third quarter was slightly below expectations at an annual rate of 1.0%. However, the underlying details gave some reason for optimism as domestic demand grew at a 2.4% pace, household consumption rose 3.5%, and the savings rate was at a 3-year high of 7.1%. Weakness in the GDP release came from a drop in the volatile business investment category as well as net trade and inventories. Of note, the GDP release also included large upward revisions to GDP growth over the last three years that meant the Canadian economy was bigger than previously thought and that there is currently less economic slack than previously estimated.

On December 2nd, the Universe Bond index duration was expected to increase slightly less than 0.05 years as a result of coupon payments and bonds maturing in December 2025 rolling out of the index. The duration extension of the broad index was not especially large, but the duration of the long term component of the index was expected to increase a much more significant 0.40 years. Long term index funds, as well as closet indexers, needed to make substantial purchases of long term bonds to mimic the extension, which led a very sharp anticipatory rally in the Canadian bond market on the final day of November.

In the United States, economic data received in November was somewhat distorted by the impact of two major hurricanes. However, the economy outside of the manufacturing sector appeared to be performing well. The unemployment rate remained low at 4.1%, personal income and spending saw good growth, and retail sales were stronger than expected. Inflation picked up, rising to 2.6% from 2.4% the previous month, while core measures of inflation remained higher than desired at 3.3%.

On November 7th, the U.S. Federal Reserve lowered the Fed Funds range by 25 basis points, bringing it to 4.50%-4.75%. The rate cut had little impact on the market since it was well anticipated. However, subsequent Fed speakers repeatedly warned investors that future rate cuts might occur slower than the markets were anticipating, which led shorter term bond yields to rise as investors pared their expectations for future rate reductions.

Internationally, the Reserve Bank of New Zealand and Sweden’s Riksbank each responded to weak economic conditions in their respective countries and lowered interest rates by 50 basis points in November. The Bank of England made a smaller move, reducing its interest rates by 25 basis points. In France, French bonds traded at their widest spread, or risk premium, versus German bonds in 12 years on fiscal and political uncertainty.

The Canadian yield curve flattened in November as long term yields fell more than shorter term ones. Yields of 30-year Canada bonds, for example, dropped 17 basis points while 2-year yields finished only 6 basis points lower. Much of the decline in long term yields occurred on the final day of the month as investors anticipated the index extension occurring at the start of December. The U.S. yield curve experienced a similar but smaller shift, with 30-year Treasury yields down 12 basis points in the month and 2-year yields barely moving.

The federal bond sector returned 1.13% in the month as lower yields caused bond prices to rise. The provincial sector gained 2.35%, helped by its longer average duration and yield spreads narrowing almost 4 basis points on average. Provincial yield spreads finished at the lowest level in three years. Investment grade corporate bonds earned 1.67% in November, as their yield spreads tightened an average of 8 basis points in the month. Non-investment grade corporate bonds returned 0.97% and Real Return Bonds earned 1.74%. Announcements of additional redemptions helped preferred shares rebound from their weakness in October, gaining 2.29% in November.

The Bank of Canada is scheduled to make its final interest rate announcement of the year on December 11th. While some observers are forecasting another 50 basis point reduction, we believe the Bank will lower rates by only 25 basis points. The economy does not appear to need urgent stimulative action and the decline of the exchange rate to one of the weakest levels in the last 20 years suggests the Bank should be cautious about larger rate cuts. We also note that the announced GST rebate from the federal government and the partial HST holiday in some provinces will provide short lived economic stimulus that may reduce the need for the Bank to lower rates faster.

We continue to believe that the pace of the Bank of Canada’s rate reductions is less important than the level at which it stops. The Bank’s most recent estimate of the neutral rate, which is neither restrictive nor stimulative, is 2.75%, or 100 basis points lower than the current rate. That seems like a reasonable point for the Bank of Canada to at least pause, given the economy is not in a recession, the scale and pace of easing from the 5.00% rate peak, and the lag with which the economy responds to rate changes. While some observers are forecasting a terminal rate as low as 2.00%, we are not convinced that is the most likely outcome. With the yields of Canada bonds of terms ranging from 2 years to 30 years clustered close to 3.00%, we don’t believe there is a lot of potential for bonds to rally much further. Accordingly, we are keeping portfolio durations close to benchmark levels.

Barring an unexpected resurgence in inflation, the yield curve should normalize further, with shorter term bond yields moving further below longer term yields. As a result, we are maintaining the emphasis on mid term issues which should outperform a combination of short and long term bonds. Regarding the sectoral mix, corporate yield spreads are historically tight, so we are keeping that sector’s allocation roughly in line with the benchmark and waiting for better opportunities to add corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.