Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

December 8, 2020

The successful development of multiple vaccines to counter the pandemic is indeed positive news for the medium term, although not without risks. The coronavirus has been mutating, with at least seven different strains already identified, and it is not certain how well the vaccines will perform against each strain. It is also not yet known how long the immunity will last after receiving a vaccination. However, the vaccines should mean social distancing and lockdown measures will become unnecessary once a sufficient percentage of people have been vaccinated. That will likely take until the end of the second quarter of 2021 in many countries. In Canada, it may take until the end of the third quarter if reports that the federal government was slow in ordering the vaccines prove correct.

In the short term, though, there remain significant economic challenges. The second wave of the pandemic is resulting in rising numbers of infections and hospitalizations that are forcing many jurisdictions in Canada and other countries to reimpose significant social distancing restrictions that will curtail economic activity. Economists’ consensus forecasts of the Canadian economy during the final quarter of this year see little or no growth, and minimal improvement in early 2021. Unemployment could rise somewhat over the next few months and business failures may increase. As a result, government deficits will remain extraordinarily high, leading to continued massive bond issuance. While the Bank of Canada will keep short term interest rates very low, it has already started paring back on its purchases of government bonds, and we think it will probably further reduce its quantitative easing in the first quarter of 2021. Consequently, we believe bond yields for all but the shortest maturities are likely to rise in the coming months, and we have started reducing portfolio durations in anticipation of this. We have also structured the portfolios to benefit from a steepening yield curve because long term yields have greater freedom to rise with the Bank of Canada holding very short term yields steady.

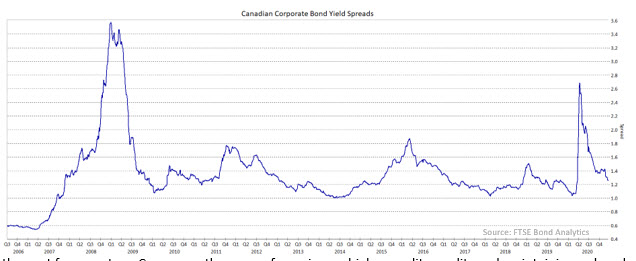

As can be observed in the following chart, the risk premiums (or yield spreads) on corporate bonds have recovered nearly all of the widening that occurred in February and March. The recent tightening of spreads leaves them below the average of the last ten years, notwithstanding the extreme uncertainty of the next few quarters. Consequently, we are focussing on higher quality credits and maintaining reduced exposure to BBB-rated issues. Should spreads narrow further, we will consider reducing the allocation to the corporate sector.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.