Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 6, 2024

Last month we noted the strong correlation between yields of U.S. Treasuries and the bonds of other countries, including Canada. In May, that correlation continued but was made more remarkable due to the difference in their prospective monetary policies. Economic activity in Canada was tepid at best and the inflation rate continued to decelerate. In the United States, economic activity also disappointed but inflation remained too high for the comfort of the U.S. Federal Reserve. The Canadian economic data, combined with dovish comments from the Bank of Canada, led many observers (including us) to anticipate the Bank would begin lowering interest rates at either its June 5th or July 24th announcement dates. In contrast, many U.S. forecasters doubted whether the Fed would cut rates at all this year. Normally, substantial differences in the expected path of interest rates in the two countries would result in significantly different bond market performance. But that was not the case in May. The Bloomberg Canada Aggregate and FTSE Canada Universe indices earned 1.78% and 1.77%, respectively, in the month.

Economic growth in Canada appeared to stall at the end of the first quarter as GDP failed to increase in March. Growth in GDP during the first three months of the year was at a rate of 1.7%, well below the expected 2.2% pace. In addition, the estimate of growth in the fourth quarter of last year was revised from 1.0% to only 0.1%. Other disappointing data included weaker than expected retail sales and manufacturing sales. The unemployment rate held steady at 6.1%, as job creation of 90,400 new positions offset the growth in Canada’s population as well as a small increase in the participation rate. The headline CPI inflation rate declined to 2.7% from 2.9%, while core price measures fell from 3.1% to 2.8%. The CPI measure was the fourth consecutive month below 3.0%, and combined with slow economic growth caused many observers to call for the Bank of Canada to begin easing monetary policy at its scheduled June 5th announcement.

The Fed met on May 1st and left its interest rates unchanged. The U.S. central bank noted the U.S. economy was continuing to expand at a solid pace, and it did not expect to lower interest rates until it had “greater confidence that inflation was moving sustainably toward 2 percent.” The Fed’s statement set the tone for the bond market for the rest of the month, and subsequent economic data did little to persuade investors that the Fed was likely to lower rates in the next few months. Inflation edged lower to 3.4% from 3.5% the previous month and core prices declined to 3.6% from 3.8% but both measures remained too high for the Fed to act. The unemployment rate edged up but remained historically low at 3.9%. Measures of consumer and business sentiment were weaker than expected, but inflation expectations increased. The housing sector data, including starts, sales of new and existing homes, and pending sales, was uniformly below expectations. In addition, the initial estimate of the GDP growth rate in the first quarter was revised lower from 1.6% to 1.3%. The generally disappointing economic news resulted in Treasury yields declining notwithstanding the Fed’s stand pat stance.

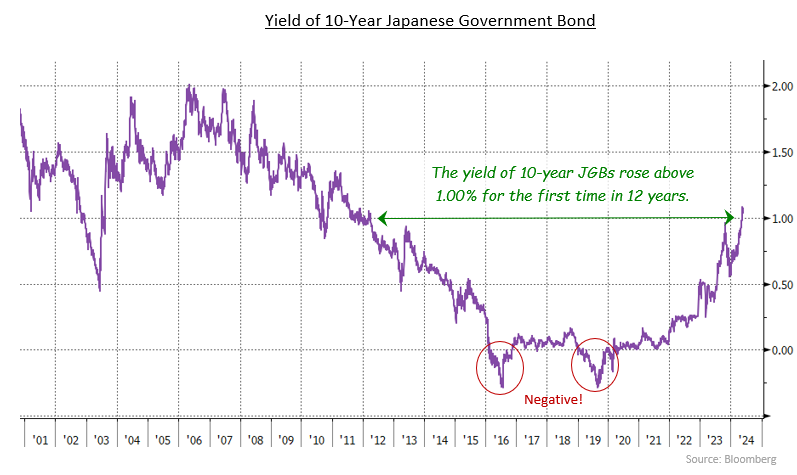

Internationally, Sweden’s Riksbank became the second G10 central bank to cut interest rates, following Switzerland’s lead earlier this year. The Riksbank was responding to Sweden lapsing into recession for four consecutive quarters. Numerous officials from the European Central Bank hinted that it is likely to begin cutting rates at its June 6th meeting. The Bank of England is also rumoured to be considering lowering its interest rates at its June 20th meeting. Only the Bank of Japan among major central banks is considering raising its interest rates as it deals with a sharp decline in the value of the Yen. The possibility of rate increases caused Japanese bond yields to rise, with the 10-year Japanese Government Bond moving above 1.00% for the first time in 12 years.

The Canadian yield curve moved lower in a near parallel fashion, as yields of different maturities fell by similar amounts. The yield of 2-year Canada bonds declined 17 basis points, for example, while 30-year yields fell 21 basis points. Yields of 5-year and 10-year Canada bonds went down 19 basis points. In the United States, the decline in mid term yields was almost identical to the changes in Canada. The drop in short and long U.S. yields, though, was somewhat less than occurred in Canada.

The decline in yields across the Canadian yield curve propelled the federal sector to earn 1.48% in May. Provincial bonds, which on average have longer durations, saw larger price rises and earned 2.37% in the month. Provincial bond returns were also helped by their yield spreads narrowing 3 basis points in the period. Investment grade corporate bonds returned 1.39% in May, as their relatively shorter duration lessened gains from lower yields. In addition, corporate yield spreads widened 2 basis points due to relatively high new issuance ($12.8 billion versus an average $10.5 billion in the last ten years), as well as a very large new issue expected in early June. Non-investment grade corporate bonds earned 1.18%, while Real Return Bonds gained an average 3.05%. Preferred shares enjoyed another strong month, returning 2.94% in May.

On June 3rd, the FTSE Canada Universe Bond index duration will extend 0.143 years as a result of the removal of $35.8 billion of 1-year bonds and the payment of $13.6 billion of coupons. The change in the index duration is the largest in five years and reflects the large number of Canada and provincial bonds that have June 1st and 2nd maturities. As June 1st and 2nd this year occurred on a weekend, the index changes will occur on June 3rd. The Long Bond index duration will extend a record 0.56 years on June 3rd because of the removal of 10-year bonds and coupon payments. Most of the 10-year bonds being removed from the Long Bond index are Canada and provincial issues, so the Long All Government Bond index will extend 0.75 years. The likely impact of the duration extensions will be buying of long term bonds on June 3rd as index fund managers adjust their portfolios to match the indices.

As this is being written, we are awaiting the Bank of Canada’s June 5th interest rate decision. We believe the Bank will start lowering interest rates either at that meeting or its subsequent one on July 24th. Economic growth has been disappointing for several months, especially if looked at on a per capita basis. With Canada’s population growing by more than 3% in the last year, and annual growth slowing to just 0.6%, the per capita trend is distinctly negative.

The Bank of Canada has indicated that it anticipates its easing cycle, whenever it starts, will be a gradual one, which suggests 25 basis point increments. The potential scope for the Bank to lower interest rates will be limited by several factors. The first is inflation, which needs to continue to recede. Any reacceleration in inflation would likely lead to a pause in the easing cycle. A second factor is the exchange rate. In the past, if Canadian interest rates fell substantially lower than U.S. ones, the Loonie declined in value, sometimes sharply. While a drop in the exchange rate is stimulative to the Canadian export sector, it also increases import costs leading to higher inflation. A third factor will be the reaction of the housing sector. The Bank will want to avoid a repetition of the housing bubble it caused by keeping borrowing rates too low. Should rate cuts result in a surge in demand when Canada already has a housing shortage, the Bank will need to slow the pace of future easing.

As we have noted in the past, the current yield curve inversion has already anticipated substantial rate cuts by the Bank of Canada. Relative to previous experiences with inverted yield curves, this cycle has built in far more potential rate cuts far earlier. With the Bank’s overnight target at 5.00% and yields of bonds maturing in 5 years and longer at 3.50% or less, there is a risk that the bond market has anticipated too much from the Bank. Accordingly, we are reluctant to extend portfolio durations substantially longer than the respective benchmarks. Indeed, we believe the Bank of Canada will not lower interest rates as much as the market expects. For several years, the Bank has been estimating the “neutral” interest rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period. And if money market yields do not fall below 3.00%, we do not see a lot of value in 30-year bonds currently yielding roughly 3.30%. Instead, we are focussed on identifying the opportunities in maturities in 5 years and less where there is the most potential for the yield curve to normalize (i.e. to eliminate the inversion).

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.