Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 2, 2022

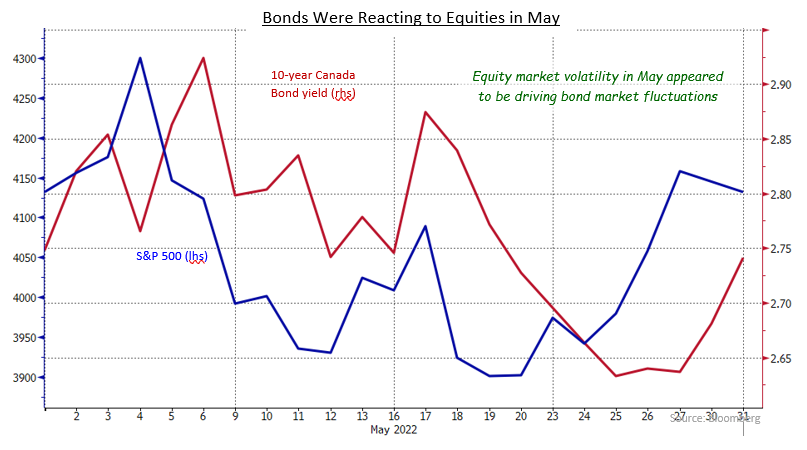

Canadian and U.S. bonds had a seesaw month in May. Initially, yields rose and bond prices declined as inflationary pressures remained high and both the Bank of Canada and the Federal Reserve were expected to make multiple interest rate increases. However, equity market volatility in the second and third weeks of the month raised concerns that economic growth would soon falter and a recession was likely in the near future. As a consequence, bonds enjoyed a flight-to-safety rally with prices rising and yields falling. However, following some strong economic releases, equities rebounded late in the month and bonds also reversed course, taking yields back close to their starting levels. For the whole month, the FTSE Canada Universe Bond Index returned -0.07%.

Canadian economic activity showed continued growth in May. Canadian year-over-year GDP came in at 3.5% and the unemployment rate fell to 5.2%, a new all-time low. Starts of new homes were stronger than expected, but resale activity slowed from year ago levels and average prices dipped slightly. The slower resale activity and price decline followed the start of the Bank of Canada’s monetary tightening, but it remains to be seen whether the one month’s data is the start of a weakening trend. Importantly, inflation continued to rise, edging up to 6.8%.

The high level of inflation led the Bank of Canada to follow through on its promise of another 50 basis point rate hike in interest rates, which they delivered as this is being written on June 1st. Market expectations had been for another 50 basis point increase in July, but the Bank’s June 1st statement warned that it was prepared to act more forcefully if inflation did not appear to be slowing.

U.S. economic data in May remained strong, as job creation was robust at 428,000 and the unemployment rate was very low at 3.6%. The favourable labour situation encouraged consumers, which resulted in strong growth of retail sales. U.S. headline and core inflation edged slightly lower in May but remained at the lofty levels of 8.3% and 6.2%, respectively. The Fed raised interest rates by 50 basis-points in May, its first increase of that magnitude this cycle. The market is anticipating two more 50 basis-point hikes at the Fed’s meetings in June and July.

The Canadian yield curve edged slightly higher in May as most benchmark yields rose between 3 and 5 basis points. The absence of more substantial changes in yields reflected a continuation of the bond market’s consensus that the Bank of Canada would be making a steady series of rate increases over the next few months. In contrast, the U.S. yield curve steepened in May as 2-year Treasury yields declined 16 basis points while 30-year yields rose 10 basis points. The decline in shorter term Treasury yields reflected increased concerns that the Fed’s monetary tightening would soon lead to a recession, while the 30-year yields reacted to the elevated inflation rate as well as the start of the Fed reducing its holdings of bonds.

In May, Canadian federal bonds earned +0.08%, as interest income more than offset the price declines brought on by slightly higher yields. Provincial bonds returned -0.15% in the month, as yield spreads in longer maturities widened slightly, thereby hurting performance. Investment grade corporate bonds returned -0.15%, with corporate yield spreads widening as a result of some very large new issues by banks. Non-investment grade bonds declined -1.63% in response to the equity market volatility. Real Return Bonds returned -0.74%, slightly underperforming nominal bonds of similarly long duration. On a positive note, preferred shares rebounded following a very weak April, gaining 5.01%, driven by two large preferred share redemptions totalling $1.5 billion.

The Bank of Canada and the Fed have become more aggressive in their monetary policy tightening and both are expected to raise their respective interest rates by at least 50 basis points at each of their next two meetings. In addition, both the Bank of Canada and the Fed have begun Quantitative Tightening (i.e. reducing their respective holdings of bonds). In the Bank of Canada’s case, that means the Bank is no longer participating in the Government of Canada bond auctions and it will not be reinvesting the proceeds as its holdings mature. In this environment, we are comfortable with lower than benchmark durations to protect the value of assets in the portfolios.

The Government of Canada will be issuing close to $19 billion of bonds in June. The majority of these new bonds will come in the 2, 3, and 5-year maturities, which will put upward pressure on yields in the front end of the yield curve. This combined with further monetary tightening by the Bank of Canada in the coming months will likely extend the flattening trend and may eventually result in an inverted yield curve, with shorter term yields trading higher than longer term yields. Therefore, we continue to structure the portfolios to preserve value, with higher cash levels and reduced holdings of mid term issues. Although an inverted yield curve is often considered as an indicator of a pending recession, we believe that economic growth in Canada will remain positive for the remainder of this year.

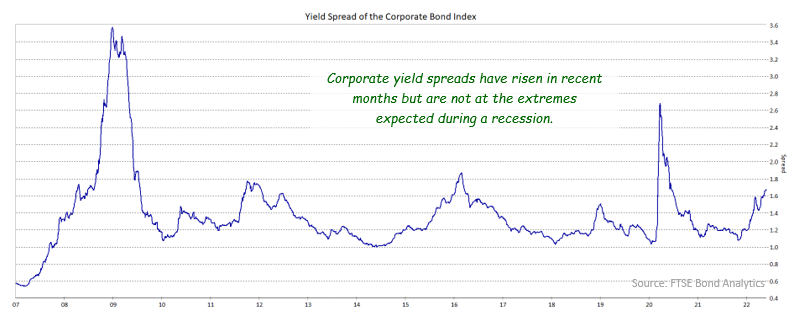

Corporate yield spreads have widened in recent months in response to the interest rate increases by the Bank of Canada and the Fed. However, spreads do not yet appear to be discounting a recession in the near future despite the risk of a recession increasing with the most aggressive monetary tightening programmes in decades underway. If inflation proves to be more entrenched and the central banks have to raise rates substantially higher, a recession may occur. In that event, we would expect corporate yield spreads to widen substantially more. Accordingly, we are being very cautious about adding to current holdings and are looking for opportunities to further strengthen the credit quality of the portfolios.

With regard to the recent equity market volatility, we would caution using the stock market as a predictor of recessions. As the Nobel prize-winning economist Paul Samuelson once quipped “Wall Street has predicted nine of the last five recessions.” In addition, the recent decline in equity indexes that included the S&P 500 briefly qualifying as a bear market was the result of Price/Earning (P/E) ratios being adjusted lower in reaction to higher bond yields. To date, the equity market has not discounted widespread declines in earnings. In other words, not all equity volatility points to the economic environment.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.