Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 1, 2021

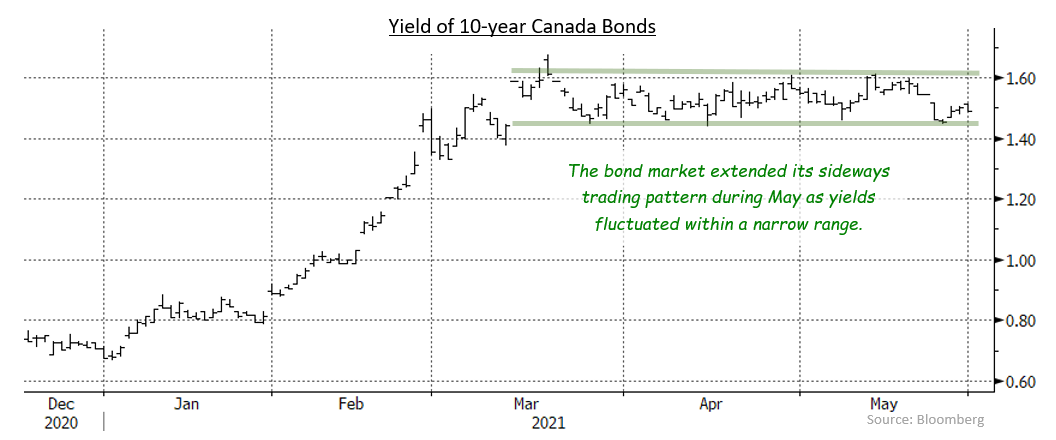

The bond market remained rangebound in May, as prices and yields stayed within the range established in mid-March. With much of Canada under lockdown restrictions since early in April, investors were willing to look past the temporary negative impact and, consequently, they mostly ignored disappointing economic releases, trusting rising vaccination rates to produce an offsetting rebound in activity. Similarly, the market had little lasting reaction to surprising surges in inflation in both Canada and the United States. Instead, investors accepted the assurances from central bankers that the increase in inflation would not last and it would soon revert to an approximate 2% pace. The FTSE Canada Universe Bond index returned 0.63% in May.

The increases in inflation were noteworthy because of its potentially devastating impact on fixed income investors. In Canada, the annual inflation rate jumped to 3.4% from 2.2% the previous month and core prices rose by 2.1%, up from 1.9%. Some of the increases had been expected because the drop in prices at the beginning of the pandemic created a low base a year ago from which to measure price increases. However, the 0.5% rise in prices in April alone had nothing to do with base-year effects and point to other reasons for rising prices. In the United States, the annual inflation rate spiked to 4.2%, well ahead of the expected 3.6%, and the fastest pace since 2009. Core prices rose 3.0% versus year ago levels, the fastest increase since 1996. Of particular concern, the month-on-month increase in core prices was 0.9%, the most since 1982. Central bankers in both Canada and the United States said they believed the rise in inflation was “transitory” and that it would soon fall back close to their 2% targets. Investors, for the time being, seemed willing to believe the Bank of Canada and the Federal Reserve. That complacency was disappointing because the risks are tilted in favour of stronger inflation due to record fiscal and monetary stimulus as well as supply chain shocks in products as diverse as lumber, computer chips, and automobiles. However, the complacency was not entirely surprising because one must be over the age of 50 to have experienced persistent inflation above 2% during one’s career.

Other Canadian economic data received during May was split. If the data covered activity in March, it generally was stronger than expected. If it dealt with activity in April, when third wave lockdowns were imposed, it tended to disappoint. For example, retail sales, manufacturing sales, and wholesale trade during March were all higher than expected. On the other hand, labour market data for April saw more jobs lost than forecast, unemployment rise to 8.1% from 7.5%, and a sharp drop in the participation rate. The bond market reaction to the more recent, weak data was muted by expectations that the passage of the third wave would lead to another sharp rebound in activity similar to what occurred following the first two waves of the pandemic.

The Canadian dollar closed the month at US$0.8278 having traded as high as US$0.8303 in mid-May. This represented a six-year high in our currency and a 5.4% increase since December 2020, which made the Loonie the strongest performing currency in the G10 year-to-date. While Bank of Canada Governor Tiff Macklem claimed the currency is benefiting from the strong rally in commodities which is good for Canada’s economy, the Governor also noted that continued appreciation of the currency could have a material impact on the Bank’s outlook and was something they would have to “take into account in setting monetary policy”. The bond market has been pricing in the Bank of Canada to begin raising interest rates prior to the Fed in the fall of 2022. However, a stronger Canadian dollar could have the effect of inhibiting exports and become a headwind to economic growth, which might delay the Bank from raising its overnight rate.

In the United States, bond investors expressed a similar apathy to economic data (“datapathy”) as occurred in Canada. The unemployment rate surprisingly edged higher to 6.1% and job creation was far below expectations for close to a million new jobs in the month. However, news that job openings surged to a record 8.1 million positions suggested that fears of catching COVID-19, childcare responsibilities, and overly generous unemployment benefits were discouraging workers from returning to the hard hit service sectors such as hospitality. As in Canada, U.S. bond prices and yields tread water in May.

The Canadian yield curve flattened a little in the month as 2-year Canada yields went up 2 basis points, while 30-year yields declined 4 basis points. The largest move came in 10-year yields that went down by 6 basis points. In the U.S., the yield curve closed marginally lower, with most yields falling by only a basis point or two.

Federal bonds returned 0.30% in May as the slight decline in yields of most bonds produced small price gains. Provincial bonds returned 1.02% in the month. The provincial results benefitted from a 3 basis point narrowing of average yield spreads versus benchmark Canada bonds. Investment grade corporate bonds returned 0.49% with their yield spreads moving marginally wider. Non-investment grade bonds returned +0.71%, with energy related issues particularly strong with oil prices rising more than 5% in May. In contrast with nominal bonds that mostly ignored the surprisingly high inflation rate, Real Return Bonds gained 3.69% as some investors sought more inflation protection. Preferred shares also had a strong month as they continued to be propelled higher by redemptions, rising 3.13% in the month.

Two and a half months into a trading range, the obvious question is what is going to cause the bond market to shake of its datapathy and break out to either higher or lower yields? It seems unlikely that central bankers will be responsible, because both the Bank of Canada and the Fed will probably keep their respective rates close to zero for another twelve months. The Bank and the Fed will adjust their quantitative easing programmes in the coming months, the Bank by making another reduction in the scale of its bond purchases and the Fed by starting to consider when to reduce its purchases, but changes in market expectations for interest rates may be required before the bond market pays much attention. In terms of economic data surprises, the bond market has shown itself willing to look past significant variability.

The consensus view is that economic recoveries in both Canada and the United States will be robust, as vaccinations substantially lower the need for further physical distancing measures, and inflationary pressures will decline as supply bottlenecks ease. The consensus at this time seems prepared to be patient. Only if substantial evidence that growth is disappointingly slow, or inflation is not as transitory as hoped, may bonds move out of their trading range. Our concern is that inflation proves to be a disappointment, and we are keeping portfolio durations defensively short of their benchmarks to reduce the impact of bond yields eventually moving higher.

The yield curve has steepened in recent months because the Bank of Canada has kept short term yields low while longer term yields have risen. Going forward, if our assumption of the Bank’s first rate increase occurring in the fall of next year is correct, we believe the greatest adjustment in yields will come in mid term issues. Accordingly, we have been reducing the allocation to mid term issues in the portfolio, moving to a more barbelled term structure.

We remain cautious about corporate bonds as they remain historically expensive. Should benchmark Canada yields resume rising in the next few months, issuers may try to lock in low financing rates and new issue supply will weigh on valuations. We also wonder if rising benchmark yields will reduce the seemingly insatiable demand for the higher yield of corporate bonds.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.