Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 22, 2020

Canada went into lockdown part way through March and the economy contracted by more than 7% that month. The economic shutdown continued unabated through April and May, and economic activity contracted even more sharply. Unfortunately, the longer Canadians remain under social distancing restrictions, the more intractable the economic damage will become. Predictions about the recovery are, however, more uncertain because this recession is different from the other economic downturns that have occurred since World War Two. In some ways, this recession resembles a caldera, which is a large crater formed after a volcano collapses on itself when its base can no longer support it. In this recession, the hardest hit have been millions of lower paid, hourly workers, while higher paid professions have been better able to cope with working from home. Another difference with this recession is that the service sector has been more severely impacted than the manufacturing sector that is typically labelled cyclical. Projecting the path of the recovery from an unprecedented downturn is fraught with uncertainty.

While consumer spending will rise as physical distancing is relaxed over time, the unemployment rate in our opinion will only fall gradually, suggesting it will be a protracted recovery for household spending. With many small businesses already declaring bankruptcy, there simply may not be jobs to return to for many people. In addition, businesses are unlikely to increase investment spending until there is greater clarity regarding future profitability. We also think that immigration, which has been a significant factor in Canadian growth in recent years, will fall sharply this year as a result of travel restrictions. In all, we believe that the recovery will take at least two to three years. Until then, the Bank of Canada will leave its interest rates close to zero, and a substantial rise in bond yields seems unlikely. We are, therefore, cautiously optimistic that yields may decline modestly further in the near to medium term.

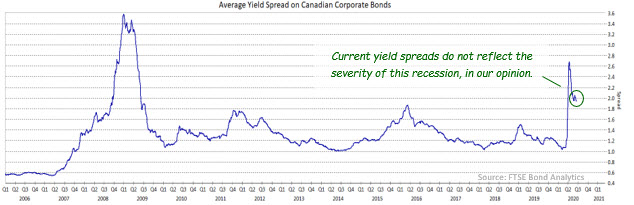

Corporate yield spreads widened very sharply in March, but never reached the widest levels hit in the 2008-2009 financial crisis. Subsequently, the Bank of Canada’s announcement of a $10 billion corporate bond purchase programme and investors’ fear of missing out on any corporate rally led to a partial reversal of March’s spread widening. We are skeptical that the recent narrowing of spreads is appropriate given the severity of the recession, and its unpredictable impact on corporate creditworthiness. The spread widening that occurred in March reflected a revision

to corporate risk premiums due to the sudden slowing in economic activity. The increased credit risk due to a far more severe recession than the financial crisis has not been significantly reduced by the Bank of Canada’s plans to purchase corporate bonds. At this point, corporate profitability for the next few quarters is very difficult to predict. In that vein, in the last week of May, all Canadian banks announced their financial results for the quarter ending April 30th. In each case profits were down significantly because of substantial increases in their provisions for future credit losses (PCLs). Bank of Nova Scotia, for example, disclosed that $92 billion of loans across its geographic footprint have requested payment deferrals, representing 14% of the aggregate loan portfolio. The bank set aside $1 billion of PCLs, which looks somewhat optimistic in light of CMHC’s prediction that `Canadian home prices may fall 9% to 18% over the next year. Our concern is also heightened by the speed with which firms are already failing as the pandemic accelerates some existing trends in the economy. In Canada, Reitman’s and the Aldo shoe group are restructuring, while in the United States such former corporate stalwarts as Hertz, JC Penney, and Pier One Imports have sought bankruptcy protection. We suspect many more firms will follow.

With unemployment possibly as high as during the Great Depression of the 1930’s and the economic recovery likely to take years, we believe it makes prudent sense to be cautious about the corporate sector at this time. Accordingly, we have been increasing the average quality of the holdings and looking for opportunities to reduce the overall corporate allocation. We continue to avoid sectors such as retailing, resources and real estate, and have reduced exposure to autos and subordinated bank debt.

As this is being written, Tiff Macklem has become the next Governor of the Bank of Canada, taking over from Stephen Poloz on June 2nd. Dr. Macklem is a former Senior Deputy Governor of the Bank who lost out to Poloz as Governor seven years ago. Given his previous experience at the Bank, we do not anticipate any significant change in policy as a result of his appointment.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.