Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 9, 2026

Financial markets moved lower in March amid substantial volatility caused by the U.S./Israel war with Iran. The lack of clear U.S. goals in the conflict combined with often conflicting and/or contradictory comments from the U.S. president as well as Iran’s effective closure of the Strait of Hormuz resulted in significant day-to-day swings in financial asset values. Interestingly, bonds did not enjoy a safe haven bid in the uncertainty as investors chose instead to focus on potential inflationary risks as the price of oil surged more than 50% in the month. Credit spreads widened somewhat for both provincial and corporate bonds, but benchmark bond yields appeared more sensitive to shifts in oil prices than were yield spreads. The FTSE Canada Universe Bond index fell 1.97% in the month.

Economic data received in March continued to show that the Canadian economy was struggling. The unemployment rate rose to 6.7% from 6.5% the previous month, as almost 84,000 jobs disappeared. Growth in Canadian GDP was slightly better than expected in January, but the year over year growth rate fell to only 0.6% from 1.0%. The inflation rate declined to 1.8% from 2.3% a month earlier, but the drop reflected base effects as prices rose 0.5% in the most recent month. The Bank of Canada left its interest rates unchanged at its March 18th meeting and Governor Macklem was dovish in his remarks about the decision:

“With inflation close to target and the economy in excess supply, the risk that higher energy prices quickly spread to the prices of other goods and services looks contained. But the longer this conflict lasts and the wider it gets, the bigger the risks. Governing Council will look through the war’s immediate impact on inflation but if energy prices stay high, we will not let their effects broaden and become persistent inflation.”

The Bank’s willingness to be patient regarding a temporary rise in inflation was in contrast with the sharp rise in short term bond yields that implied multiple interest rate increases would occur later this year.

As in Canada, U.S. economic data received in March covered the pre-war period and did not provide an indication of the war’s effect on economic activity. That said, the U.S. economy appeared resilient as the war began with the unemployment rate of 4.4% close to historical lows. Personal income and spending experienced healthy increases and the manufacturing sector was stronger than forecasts. CPI inflation held steady at 2.4%, failing to improve toward the Federal Reserve’s 2.0% target. The Fed left its interest rates unchanged in March as it too indicated a willingness to look through a temporary rise in inflation.

Internationally, the only central bank that adjusted its interest rates in March was the Reserve Bank of Australia. The RBA responded to higher than desired domestic inflation and raised its rates 25 basis points for the second consecutive month. Global bond yields, though, moved sharply higher in March, with many markets, particularly in Europe, experiencing larger yield increases than occurred in Canada and the United States. Media reports suggested global central banks were significant sellers of U.S. Treasuries as they sought to bolster their own economies and exchange rates.

Canadian bond yields rose sharply across all maturities in March, with the biggest increases occurring in shorter maturities as investors anticipated that the Bank of Canada would be forced to raise interest rates later this year to combat inflation. Yields of benchmark 2-year Canada bonds, for example, climbed 42 basis points, while 30-year yields rose 25 basis points. The upward shift in the Canadian yield curve, characterised as a bear flattening, was almost identical to the shift in the U.S. yield curve despite the Bank of Canada and the U.S. Federal Reserve likely having very different policy responses over the next year.

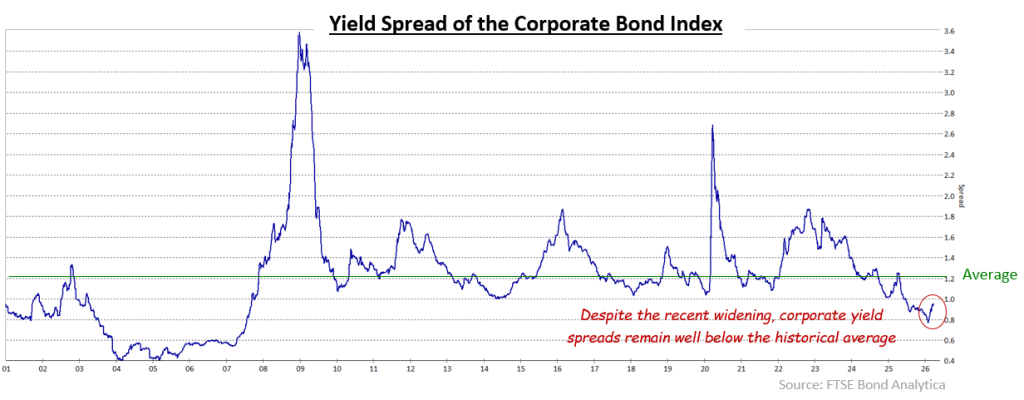

The federal sector returned -1.70% in the month as higher yields pushed bond prices lower. The provincial sector declined 2.54%, reflecting the longer average duration of the sector combined with a 4 basis point widening of long term provincial yield spreads. The increased spreads were due in part to concerns about increased supply as eight provinces delivered budgets that forecast larger than expected deficits and delayed returns to balanced budgets. The corporate sector returned -1.70% notwithstanding its relatively short average duration. Corporate yield spreads widened an average of 5 basis points, with the largest increases occurring in long term issues. Non-investment grade corporate bonds returned -0.79% in the risk off environment. Real Return Bonds declined 2.19%, significantly outperforming nominal issues with similarly long durations. Preferred shares were less volatile than either bonds or stocks in March, declining only 0.92% in the month.

Rather than trying to predict the end of the U.S./Israel war with Iran, which seems at least partially dependent on the everchanging whims of a mercurial U.S. president, we are looking at the likely ramifications of reductions in the supply of oil, natural gas, fertilizer, and other goods produced in the Middle East due to war-related damage. Even if the war were to end overnight, repairs to the damaged production facilities will take several months to a few years in the case of liquid natural gas infrastructure. While Canada is largely immune to the supply shortages that are negatively impacting Asian countries as well as Europe, we will be affected by higher prices.

We believe the Bank of Canada will be correct to look through the temporary spike in inflation that seems likely. Higher interest rates won’t lower gasoline prices. With the Canadian economy already struggling due to the U.S. trade war, the potential for demand destruction due to higher energy prices and uncertainty around the Iran war could slow domestic economic activity even more. Global growth also seems at risk. We believe the Bank of Canada is unlikely to raise interest rates this year, while interest rate cuts are a growing possibility. Consequently, we believe the recent sharp rise in short term bond yields is likely to reverse.

Despite the increases in the yield spreads of both provincial and corporate bonds in February and March, both sectors remain expensive, in our opinion, and do not properly reflect the currently elevated economic risks. Corporate bonds, we believe, are particularly vulnerable to a correction in equity markets.

We are also concerned that a developing liquidity crisis in private credit may spill over to public credit markets. In both Canada and the United States, large private credit funds have had to restrict, or “gate”, withdrawals because the funds did not have sufficient liquidity to satisfy investors’ redemption requests. In addition, the bankruptcy of little known British mortgage lender, Market Financial Solutions, caught traditional lenders by surprise and left them with large losses. What is unknown are the exposures of banks and alternative lenders to private credit. Warren Buffett’s comment about excessive risk taking may apply “Only when the tide goes out do you discover who has been swimming naked.”

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.