Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 7, 2021

As this is being written, a third wave of the pandemic is causing infections and hospitalizations to rise sharply in several parts of Canada. In some ways, this seems a race between vaccinations and variants. As with the second wave, we do not anticipate severe lockdowns will be necessary and, as a result, Canada’s goods-producing sector will continue to thrive. The experience of the second wave showed a smaller number of services sectors in contraction compared to the first wave, with businesses in most sectors finding ways to adapt and keep operating. We believe the same dynamic will occur in the third wave and Canada’s economy should continue to recover. We are optimistic that the increasing availability of vaccines will reduce infections and deaths, leading to a more muted impact of the third wave relative to the second.

As we noted last month, the bond market often pauses and consolidates within a trading range after a significant change in yields such as we have seen so far in 2021. We would not be surprised if that occurs again over the next few weeks and, accordingly, we have shifted the portfolio durations to only slightly short of the benchmarks. We believe, though, that the longer term outlook is for higher yields as the vaccination rates rise and the pandemic hopefully recedes. In addition, we anticipate that the Bank of Canada will reduce its purchases of Canada bonds before the federal government has started to reduce its borrowing requirements. If that occurs, it will put additional upward pressure on yields.

Looking ahead to the second quarter, in addition to a possible worsening of the pandemic, potential volatility may come from the first federal budget in over two years to be delivered on April 19th. With the Canadian economic recovery currently proceeding more rapidly than expected, there is diminished need for increased stimulus spending, but the minority government may be tempted to promise substantial new spending ahead of an early election call. With the Bank of Canada likely to reduce its purchases of federal bonds, the financing of the deficit may put pressure on Canadian bonds. Other sources of potential volatility include a stock market correction as well as geopolitical surprises (e.g. a coup in Brazil, or China moving to take over Taiwan).

The overall yield curve will likely steepen as most bond yields rise while short term yields are restrained by the lack of movement in the Bank of Canada’s overnight target rate. As the economy continues to recover, we think mid term yields will anticipate eventual reductions in monetary stimulus, leading to a steeper yield curve in the shorter maturities and a flatter curve for longer term issues. Accordingly, we have reduced portfolio exposure to the mid term sector.

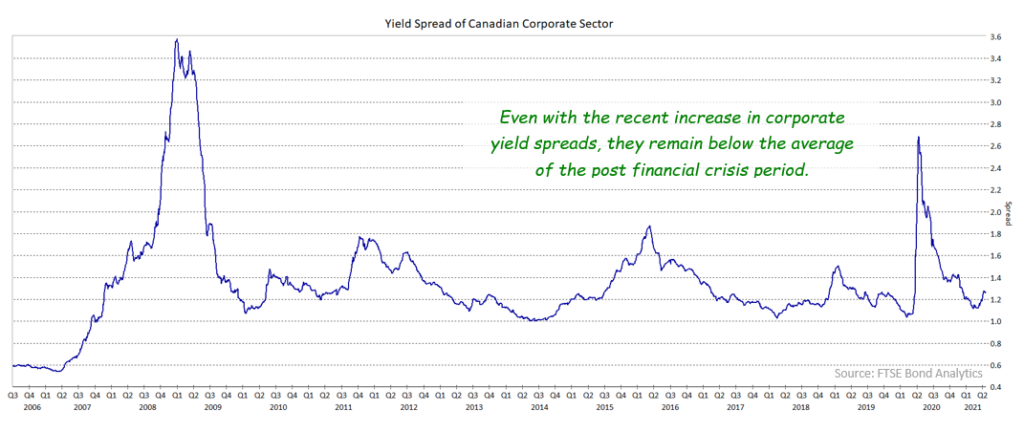

We remain somewhat cautious about corporate bonds. The recent small increase in corporate yield spreads left them still historically expensive. Should benchmark Canada yields continue to rise in the next few months, issuers will try to lock in low financing rates and new issue supply will weigh on valuations. We also wonder if rising benchmark yields will reduce the seemingly insatiable demand for the higher yield of corporate bonds.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.