Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 12, 2022

The bond market sold off sharply in March as inflationary pressures forced the Bank of Canada and the U.S. Federal Reserve to initiate what are expected to be series of interest rate increases. At the beginning of the month, bond prices traded higher and bond yields moved lower as Russia’s invasion of Ukraine caused a flight to safety bid for bonds. However, the market subsequently came to a consensus that the war in Ukraine was a regional event and its most significant impact globally would be to exacerbate already high inflation by causing shortages of certain commodities and foodstuffs. Bond yields moved steadily higher through most of the remainder of the month, encouraged by the central bank rate increases and expectations of more aggressive monetary tightening in the coming months. In one example of the sharp increases in bond yields, Canadian 10-year bond yields rose to 2.60%, a level not seen since October 2018. The FTSE Canada Universe Bond Index returned -2.99% in March.

Canadian economic activity reverted to a more robust footing as both Ontario and Quebec ended their Covid-19 lockdowns. Notwithstanding the lockdowns, GDP growth for January was estimated at 0.2% which set up first quarter GDP to grow at a robust 4% pace. Employment surged in February, with 336,600 new jobs created, leading the unemployment rate to drop a full percentage point to 5.5% from 6.5%. The unemployment rate fell below its pre-pandemic level and the participation rate improved to near pre-pandemic levels. Other good economic news included retail sales, which increased substantially more than expected. Less positively, Canadian inflation continued to increase, reaching 5.7%, its highest level since 1991.

The Bank of Canada finally began raising its interest rates on March 2nd, with a 25 basis point increase. Subsequent comments by Bank officials hinted that future increases may be more aggressive, and the bond market began anticipating increases of 50 basis points at the next two rate setting meetings. Yields of shorter term bonds were especially impacted as investors anticipated the changing trade-off between money market instruments and bonds.

U.S. economic data showed continued strong growth in that country. As in Canada, there was robust job growth and it pushed the U.S. unemployment rate down to a historically low rate of 3.6%. Retail sales were also higher than forecasts. U.S. inflation continued to climb, reaching 7.9%, while the core rate rose to 6.4%. The headline and core inflation rates were at their highest levels in 40 years. The inflation readings increased the pressure on the Fed to take more aggressive action to slow the price increases.

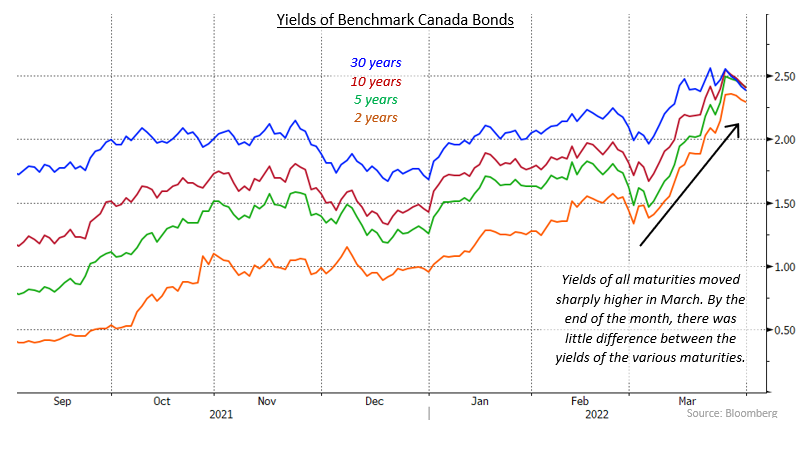

All Canadian bond yields moved higher in March, with shorter term yields rising more than longer term ones. Yields of 2-year Canada bonds, for example, rose 82 basis points in the month, reflecting the impact of the Bank of Canada’s March 2nd rate increase plus expectations of larger increases in the near future. By comparison, the yield of 30-year Canada bonds rose only 25 basis points in the period. By month end, there was very little difference between the yields of 5, 10, and 30-year Canada bonds, with each of them close to 2.40%. In other words, the Canadian yield curve have become quite flat. In the United States, the shifts in bond yields were remarkably similar to the Canadian ones, with larger increases in shorter term yields than in longer term ones and a convergence of most yields to approximately 2.40%.

In March, Canadian federal bonds returned -2.99% as rising yields caused bond prices to fall. Provincial bonds returned -3.25% in the month. While provincial yield spreads closed marginally tighter in the month, their performance was hurt by their longer average durations as yields rose. Investment grade corporate bonds returned -2.60% as they experienced considerable volatility in their yield spreads during the month. Corporate yield spreads widened sharply in the first half of the month as investors were concerned about the ramifications of the Russian/Ukrainian war as well as the impending monetary tightening in both Canada and the United States. However, on March 16th, the day that Canadian inflation was shown to be the highest since August 1991 and the Fed started raising interest rates, corporate yield spreads began to narrow again. It seemed investors had a “Buy the Dip” mentality and decided to take advantage of the relative cheapening of the sector. By month end, all but 2 basis points of the initial 15 basis point widening had been reversed. Non-investment corporate bonds returned -1.57% in March, outperforming investment grade corporates due to their larger coupons and shorter duration. Real Return Bonds returned -2.54%, which was better than the return of nominal bonds with similarly long durations. Preferred shares returned -0.27%, thereby outperforming bonds by a significant margin in the month.

Despite Russia’s invasion of Ukraine being a tragedy that has shocked the world, central bankers are treating the event as a regional disruption and remain more focused on current inflationary pressures reaching multi-decade highs. Both the Bank of Canada and the Fed have indicated that they plan to be more aggressive in subsequent moves than their initial 25 basis point rate hikes in March. Market expectations are that both central banks will increase rates by 50 basis points at their next meetings, which are April 13th and May 4th respectively. We see little reason to disagree, and we expect additional rate increases are likely at the subsequent meetings scheduled for June. In addition, the Fed has stated that Quantitative Tightening (reducing its holdings U.S. Treasuries through maturities and/or sales) is a strong possibility to commence in May, which may push bond yields higher still.

At the beginning of March, we shortened portfolio durations which was highly beneficial to performance as bond prices sold off and yields increased throughout the month. However, now that the central banks have begun reducing monetary stimulus and the market has priced in aggressive tightening going forward, we have returned duration of the portfolios to neutral. In our view, much of the monetary tightening expectations have been priced into the market and there is still a substantial risk with the crisis in Ukraine. While we are still cautious about the potential higher yields, we feel that being neutral duration gives us the opportunity to take advantage of a volatile market, especially after so much bearish sentiment has been priced into bonds.

Over the past year, North American yield curves have seen substantial flattening due to expectations of monetary tightening. With the Canadian and U.S. economies remaining strong, it is likely that the Bank of Canada and the Fed will raise interest rates multiple times in both 2022 and 2023. As a result, short term yields in both countries may experience more upward pressure than longer term yields, and the yield curves may become inverted as a consequence. However, while some observers believe an inverted yield curve is a harbinger of a recession, we do not believe growth is going to falter significantly over the next twelve months. The portfolios are structured to try to preserve values should short term yields be pushed higher.

Last autumn, corporate bonds had rallied to historically expensive spread levels. At that time, we were somewhat defensive regarding the positioning of corporate bonds in the portfolio. With the cheapening of corporate bonds in the first quarter of 2022, we now see corporate credit as more attractive and have been taking advantage of opportunities to add oversold corporates to the portfolios. We are mindful of volatility surrounding global geopolitical tensions and, therefore, we are being patient with this strategy and look to continue to take advantage of opportunities as they become available.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.