Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

July 16, 2020

In May and June, the Canadian and American economies began recovering from their steep plunges in the previous two months. As expected, the reduction in strict physical distancing requirements resulted in an improvement in some areas of the economy. However, we are a long way from fully reversing the sharp drop from February’s levels. We continue to believe that the recovery will resemble a flipped square root sign as the economy experiences a partial, quick rebound followed by disappointingly slow growth that makes full recovery some years away.

The reason we believe the recovery will be slow and prolonged is the Canadian economy is facing a multitude of headwinds. Unemployment is very high, but consumer spending has been supported by temporary government aid programmes. When those programmes wind down, spending will likely be negatively impacted. The unemployment rate may fall initially when recipients of government aid are forced to return to jobs that pay less but, in total, many of those jobs have simply been wiped out. Another economic headwind will be the absence of business investment spending given the economic uncertainty and operating rates that are well below capacity. A third challenge for the Canadian economy is that the travel restrictions to reduce the spread of COVID-19 are limiting the number of immigrants to Canada. In recent years, immigration has played a major role in boosting growth, but that has been severely diminished this year. Even if we are fortunate enough to avoid a second wave of the pandemic, Canadian growth looks like it will be anemic for the next year or two.

If we are correct in expecting growth to be disappointing, the Bank of Canada is likely to keep interest rates at the current, extraordinarily low levels for two years or more. While we believe the Bank will eschew negative interest rates (because they are not effective and have unintended negative consequences), it may try some form of yield curve control (YCC) to keep shorter term bond yields very low. A key question for the bond market, if YCC is adopted, will be the maximum term of the targeted bonds. In Australia’s version of YCC, for example, 3-year bond yields are targeted. Leaving yields of longer term bonds to potentially drift higher. We believe the Bank would likely target yields out to 5 years because of their importance to the residential mortgage market. But that would allow mid and long term yields move higher, which is why we see potential for the yield curve to steepen from current levels.

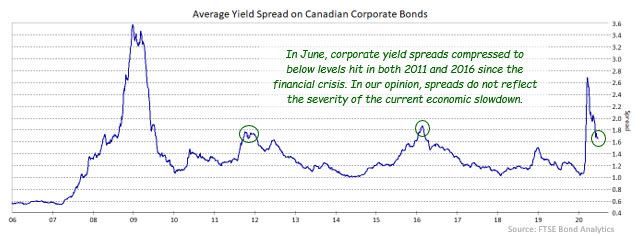

The sharp narrowing in corporate yield spreads in the last two months is overdone, in our opinion, and does not reflect the economic uncertainty nor the likelihood of reduced profitability for many firms in the coming quarters. We are currently in the worst economic downturn since the Great Depression of the 1930’s, but yield spreads are narrower than they were on two occasions since the 2008-09 financial crisis. We are concerned that personal and

corporate bankruptcies may soar when loan payment and rent deferral plans end, and bank earnings will fall sharply as a consequence. We suspect declining bank earnings or a correction in equity markets may be the trigger to corporate yield spreads widening again. Rather than trying to time when that happens, we prefer to be more conservative by shifting to higher quality issues and reducing lower rated issues such as BBB-rated bonds. In the short run, we may give up some yield be focussing on higher-rated issues, but elevated risk levels make that the appropriate strategy. We continue to avoid sectors such as retailing, resources and real estate, and have reduced exposure to autos and subordinated bank debt.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.