Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

August 5, 2022

The bond market enjoyed a strong rally in July as investors reacted to central bank rate increases by anticipating a recession that would lead to subsequent easing of monetary policy. Bond prices rose and yields fell sharply even as the Bank of Canada, the U.S. Federal Reserve, and other global central banks raised interest rates by the largest increments in many years. Equity markets also surged higher, with large gains for the S&P/TSX composite and the S&P500, as well as other indices. The optimism that the monetary tightening cycle would be short-lived occurred despite inflation rising further and economic data showing growth remaining strong. The FTSE Canada Universe Bond Index gained 3.90% in July.

Data released in July showed that the Canadian economy continued to perform well. The unemployment rate fell to 4.9% from 5.1% the previous month, although the decline was due to a sharp drop in the participation rate. The number of jobs declined by 43,200 in the month, with part time positions representing the majority of the losses. Growth in Canada’s GDP during May was negligible, but better than forecasts, and the year-over-year inflation-adjusted growth rate accelerated to 5.6% from 5.1%. Retail sales and the trade surplus were also better than expected. The housing sector was a notable exception to the positive economic news. While starts of new homes remained elevated, sales of existing homes declined for the fourth consecutive month and average prices also continued to decline. Inflation accelerated less than expected, but still hit a multi-decade high of 8.1%. In addition, inflationary pressures appeared to be broadening as average hourly wages rose at an annual rate of 5.2%, up from 3.9% the previous month.

The Bank of Canada was more aggressive than expected in the month, raising its trendsetting interest rates by 100 basis points rather than the anticipated 75 basis point increase. Despite this being the fourth increase since it began tightening monetary policy, the Bank described it as an effort to “front load the path to higher interest rates”. The Bank said it expected inflation to remain around 8% for the next few months, so it would need to raise rates further as it tried to reduce inflationary pressures.

U.S. economic data was somewhat mixed in July. The unemployment rate held steady at the very low 3.6% rate, as job creation remained robust. However, U.S. GDP unexpectedly shrank at an annual rate of 0.9% in the second quarter, with declines in inventories having the largest influence and business investment and the housing sector also weak. It was the second consecutive quarter of the GDP shrinking, which is a popular definition of a recession, but it is unlikely that the official arbiter of recessions, the National Bureau of Economic Research, will declare the U.S. to be in a recession given how strong the labour market is. As well, several Fed officials stated they did not believe the economy was in a recession. Personal income and spending data were also better than expected in July, helping to refute the recession argument. As in Canada, inflation hit a new high, rising to 9.1% from 8.6% the previous month.

In response to the ongoing surge in inflation the Fed raised its administered rates by 75 basis points, the second consecutive increase of that magnitude. The central bank indicated that it was likely to raise rates further in coming months, but it would be providing less forward guidance about its future actions. Instead, the Fed said it would adjust its moves according to current economic conditions. Some investors interpreted the Fed becoming more data dependent to mean it would quickly reverse its rate increases if the economy weakened, which led to bond yields falling further over the balance of the month. We disagree with that interpretation, however, believing the Fed eliminated forward guidance because it wanted greater flexibility and to avoid the criticism received earlier this year when it raised rates by more than it had suggested was likely.

U.S. bond yields are usually more volatile than Canadian ones but, in July, the opposite was true. The Canadian yield curve flattened as 2-year Canada bond yields declined 17 basis points while 30-year yields fell 38 basis points. Mid term yields, however, dropped substantially more, with 5 and 10-year yields declining 50 and 62 basis points, respectively. The changes left the Canadian yield curve saucer shaped, with mid term yields lower than both short and long term yields. In the United States, the yield curve also flattened as 2-year Treasury yields edged 3 basis points lower while 30-year yields declined 14 basis points. As in Canada, mid term yields fell the most as 5 and 10-year Treasury yields went down 31 and 33 basis points, respectively. The large declines in mid term yields in both countries reflected revised expectations that the Bank of Canada and the Fed would need to aggressively lower rates in 2023 in response to weak economic activity.

The Canadian federal bond sector returned 3.15% in July as the drop in yields resulted in higher bond prices. The provincial sector gained 5.18% in the month, benefitting from longer average durations and a 5 basis point narrowing in yield spreads. The investment grade corporate bond sector earned 3.22% as it also benefitted from a 5 basis point narrowing in yield spreads. The narrowing in yield spreads seemed rather muted in comparison with the sharp decline in benchmark Canada yields. Corporate bond investors appeared to be less willing to look through the looming recession and chose to keep risk premiums relatively elevated. Non-investment grade bonds earned 1.69%, underperforming investment grade issues notwithstanding robust equity returns in the period. Real Return Bonds surged 8.09%, again outperforming nominal federal bonds on a duration-equivalent basis. The preferred share market was plagued by illiquidity and continued retail selling, but it rebounded late in the month to finish with a -0.25% return.

Looking ahead, a recession is an increasingly likely outcome. Inflation has risen to very high levels due to multiple contributing factors including supply chain disruptions, the war in Ukraine, changes in consumption patterns due to the pandemic, and excessive fiscal stimulus to counter the effects of the pandemic. Consequently, inflation may not fall quickly enough to avoid economic contraction resulting from higher interest rates. We remain comfortable with the assessment we made last month:

“We believe neither the Bank of Canada nor the Fed will stop tightening monetary conditions if a recession develops but inflation does not fall back towards their 2% targets. The pace and scale of the rate increases may decline, but tighter monetary conditions will continue until inflation is under control. In this environment, we believe that higher bond yields are likely, and we are comfortable with lower than benchmark durations to protect the value of assets in the portfolios.”

In particular, we believe the bond market rally since mid-June has gone too far because it is discounting interest rate cuts in response to a recession that has not even occurred yet. It also assumes a rapid decline in inflation that will allow the Bank of Canada to quickly cut interest rates next year.

We believe the Bank of Canada will probably raise rates by 75 basis points at its September 7th announcement date. That increase, plus additional ones at subsequent meetings, should lead to a full inversion of the yield curve. In other words, shorter term benchmark Canada bond yields will be higher than longer term bond yields. The portfolios are structured with relatively low exposure to the mid term part of the yield curve to protect value as the inversion develops.

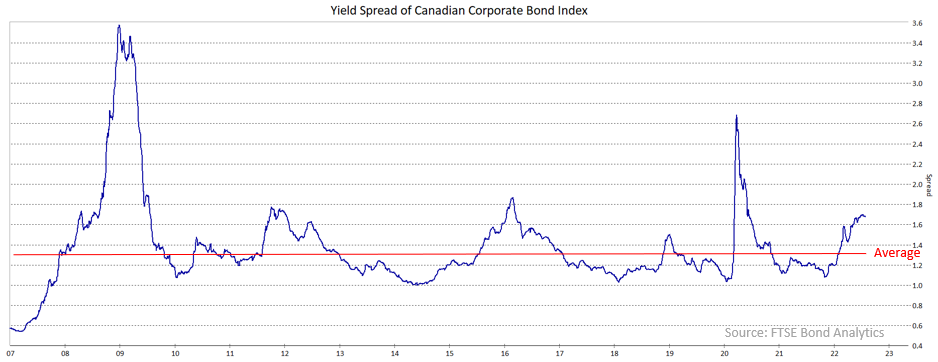

If a recession does occur, starting perhaps later this year or in early 2023, we would expect corporate yield spreads to widen from current levels. As can be seen in the following chart, corporate yield spreads are wider than average, but are not close to the levels experienced either at the start of the pandemic or during the Great Financial Crisis. In light of the growing risk of a recession, we are being very conservative regarding the creditworthiness of issues in the portfolio and about adding new holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.