Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

August 4, 2021

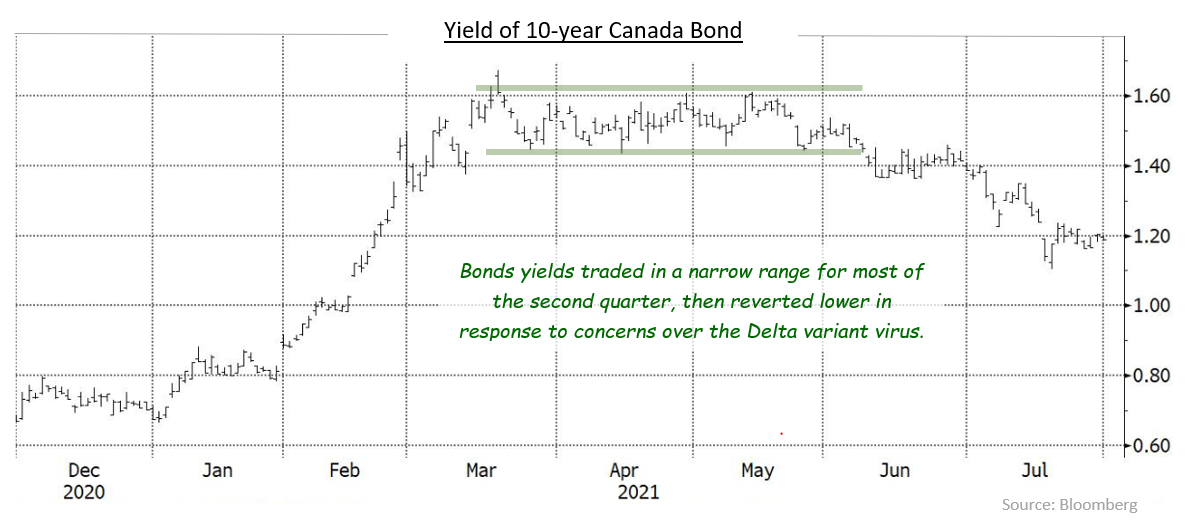

North American bonds continued to rally during the month of July. Yields declined further below the trading range that was established back in March as fixed income investors seemed to be less interested in the level and direction of inflationary pressures and more focused on the risk of the potential spread of the Delta variant virus. The Canada 10-year bond touched a monthly low yield of 1.14% which was considerably lower than the year-to-date high yield of 1.61% that was established in mid-March. The FTSE Canada Universe Bond index returned 1.03% in the month.

Canadian economic data was mixed in July as the most recent May GDP numbers declined -0.3%. However, June was projected to rebound by a hefty +0.7% as the economy re-opened once again, and second quarter GDP was estimated to have had net growth at a +2.5% annual pace. While employment growth was much stronger than expected, the quality of the gains was poor with full-time jobs declining and part-time jobs accounting for all the increase. Retail sales declined but were expected to see improvement in the coming months with the removal of third wave lockdowns. Inflation remained elevated at 3.1%, but that was down from 3.6% the previous month. While headline inflation was still near a 10-year high, monthly inflationary pressures subsided somewhat. However, with supply chain issues still very much present and commodity price gains still feeding through, we believe the risks remain tilted to the upside for inflation.

As expected, the Bank of Canada left its administered overnight rate unchanged at 0.25% at its July meeting and reduced its quantitative easing (QE) program of bond purchases from $3 billion to $2 billion per week. The Bank also stated that it will “remain committed to holding the policy interest rate at the effective lower bound until economic slack is absorbed”. The market continued to mark the second half of 2022 as the starting point for higher interest rates from the Bank.

U.S. data showed that that economy was in a good place. Second quarter GDP grew at a robust 6.5% annual pace, although that was well below expectations. However, given that the U.S. savings rate is above 10%, there remains ample spending power for consumers to drive strong growth ahead. Employment rose by 850,000, with an upward revision to the previous month, and retail sales surprised the market by rising rather than declining as expected. U.S. inflation rose again with a monthly increase of 0.9% which was substantially higher than expected. Year over year inflation in the U.S. hit a 13-year high of 5.4% and core inflation, at 4.5%, was at a level not seen since 1991.

As expected, the U.S. Federal Reserve left its benchmark interest rate unchanged at 0.25%. While the Fed continued to stress that inflationary pressures will be temporary, Chairman Powell did state that the economy had made progress toward its goals of full employment and low inflation, and the Committee would continue to assess progress at upcoming meetings. With only three Fed meetings remaining in 2021, the bond market is expecting the Fed will begin to taper its $120 billion monthly QE program this autumn.

During July, the Canadian yield curve flattened marginally as 2-year Canada bond yields declined 6 basis points while 30-year yields went down 8 basis points. However, as often is the case, mid term sector led the way and, during July’s bond rally, 5 and 10-year yields fell 17 and 18 basis points, respectively. In the United States, most yields fell by similar amounts as in Canada with 30-year yields being the main exception. Yields of 30-year Treasuries fell a remarkable 17 basis points as investors ignored higher inflation and focussed instead on the potential for growth to slow sharply because of the rapid spread of the Delta Covid variant.

Canadian federal bonds returned 0.85% as declining yields caused bond prices to rise. Provincial bonds returned 1.24% in the month. The longer average duration of the provincial sector led to its strong performance as yields fell while provincial yield spreads were flat from the previous month. Investment grade corporate bonds returned 0.92%. Short and mid-term yield spreads moved wider by 3 basis points due to robust new issue supply, while long term corporate spreads held steady in the month. Non-investment grade bonds returned 0.64%, thus underperforming higher quality issues in the period. Real Return Bonds, which have quite long average durations, earned 1.60%, essentially keeping pace with nominal bonds as investors pondered whether the recent rise in inflation was likely to soon be reversed. Preferred shares returned 0.80% in July as redemptions continued to create demand for replacement issues.

The bond market traded in a range from March through early June, but yields have declined since then. While the Bank of Canada and the Fed continue to hold accommodative monetary stances, we believe that the recent rally in bonds has been primarily driven by a flight-to-quality from fears of a potential slow down due to the rise of the Delta variant virus. We also believe international demand for safe haven bonds may have played a role in the recent rally. It is our view, however, that well vaccinated developed nations will be able to stifle the viral spread and pent-up consumer demand will spur rapid growth as restrictions are removed and economies are reopened. In this environment, inflation will continue to build, and investors will likely demand higher yields to compensate them for the decay of fixed income streams from inflationary pressures. In addition, the tapering of QE and ongoing issuance of government bonds should provide significant upward pressure on yields from reduced demand and increased supply. As a result, we continue to maintain a defensive stance in portfolio durations with positioning that is shorter than underlying benchmarks.

We expect to see the Bank continue to reduce its QE bond purchasing program, with its next reduction likely coming in October. In addition, the Bank and the Fed are expected to begin raising interest rates in the second half of 2022. Since the beginning of the spread of the Covid virus, the central banks’ extreme accommodative monetary policy that led to a steepening of the yield curve. Now that economies are poised to begin reopening, yield curves should begin to flatten as the central banks “take their foot off the gas” to normalize monetary policy. This normalization will push the short-mid part of the yield curve higher relative to longer-term yields and further flatten the yield curve.

Looking ahead to the third quarter, we expect, as vaccinations increase across the population, lockdowns will recede, and the economy will continue prosper into the reopening. Considerable base and pent-up demand will likely spur robust growth over the remainder of 2021 and 2022. This strong demand growth will provide firm support for the corporate credit market. While the corporate credit backdrop looks attractive and we are comfortable positioning in the sector, we are mindful of the current expensive valuations of corporate bonds versus historical levels, and we are being very selective in adding to corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.