Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

February 7, 2020

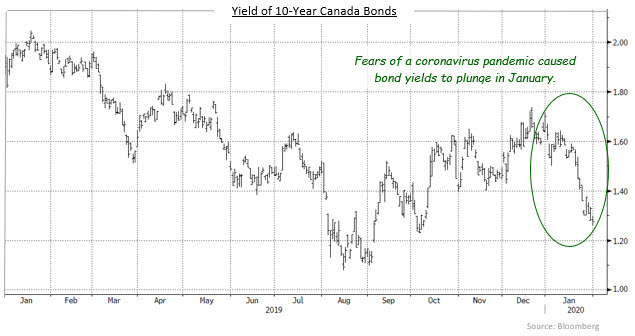

Global bond prices surged higher and yields plunged in January as fears that an outbreak of a new coronavirus in China would lead to a global pandemic. Canadian bonds were caught up in the flight-to-safety bid that developed in the second half of the month, as equity and commodity prices dropped, and investors tried to anticipate the impact of the outbreak on global economic activity. Backward looking economic data and the impeachment trial of U.S. president Trump were mostly ignored in favour of very preliminary data on the virulence and spread of the new disease. Both the Bank of Canada and the U.S. Federal Reserve left their trendsetting interest rates unchanged, but the decline in bond yields in both countries to below the central banks’ respective overnight targets suggested investors were anticipating monetary easing in the coming months. The FTSE Canada Universe Bond index returned 2.91% in January.

Canadian economic news during January was, on balance, mildly positive and offered little impetus for the Bank of Canada to adjust monetary policy. As noted above, however, the data became of secondary importance later in the month with the coronavirus headlines dominating the market. The Canadian unemployment rate reversed its November spike up, falling back to 5.6% from 5.9%. GDP growth in November was better than expected at +0.1% and the year-over-year increase improved to 1.5% from 1.2% the previous month. Inflation held steady at 2.2%.

As expected, the Bank of Canada left its interest rates unchanged on its January 22nd announcement date, just as the coronavirus was starting to dominate the headlines. The Bank was more dovish than expected in explaining its decision, with reduced expectations for growth during both the fourth quarter of last year and the first quarter of this year. The Bank’s statement noted “Governing Council will be watching closely to see if the recent slowdown in growth is more persistent than forecast”. That suggested the Bank would consider lowering its trend-setting rates at either of its meetings in March or April if growth continued to disappoint. The Bank indicated that it was particularly concerned by falling consumer confidence and falling consumer spending. However, a consumer confidence survey released later in the month showed a sharp recovery in consumer attitudes, lessening the likelihood of additional monetary stimulus.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.