Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

March 12, 2025

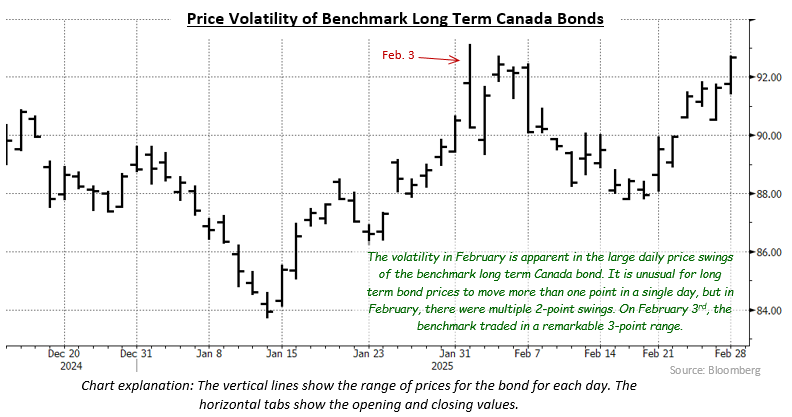

surprise imposition of tariffs on Canada, Mexico, and China by U.S. President Trump on the opening weekend of February initiated a trade war that caused substantial volatility in the bond market, as well as other financial markets. On February 3rd, the first business day of the month, bond prices opened substantially higher as the economic uncertainty caused a flight-to-safety bid. Bond prices rose further through the day but fell sharply in the late afternoon when Trump announced a temporary pause on the tariffs. Over the balance of the month, on-again, off-again headlines regarding the tariffs led to significant fluctuations in Canadian bond prices. Yields eventually closed lower on the month due to the ongoing threat of tariffs and their potential negative impact on economic activity. In the United States, bond yields fell even more sharply in February on concerns that the trade war would hurt U.S. growth, as well as equity market volatility. The Bloomberg Canada Aggregate and FTSE Canada Universe indices returned 1.08% and 1.10%, respectively, in the month.

Data received in February showed that the Canadian economy was performing better than expected prior to the instigation of the trade war by the United States. Canadian GDP grew at a robust 2.6% pace in the fourth quarter of last year, despite a large drop in inventories, while final domestic demand surged higher at a 5.6% pace. In addition, GDP growth in prior quarters was revised higher, especially in the third quarter which was increased to 2.2% from the previous 1.0% estimate. As a result of the better than expected growth, the amount of slack in the Canadian economy (i.e. the Bank of Canada’s output gap) was reduced by half. The unemployment rate also surprised, declining to 6.6% as strong job creation more than offset higher participation. Inflation remained low at 1.9% because the temporary GST/HST holiday caused food, alcohol and clothing prices to weaken.

In the United States, the economy continued to experience healthy growth, although concerns about the trade policy and cuts to the federal workforce began to make consumers and businesses more cautious in their spending. Early in the month, the unemployment rate edged lower to 4.0% from 4.1% despite a rise in the participation rate. Subsequent economic data, though, was generally softer than expected, which contributed to bond yields falling. The weaker than expected data included retail sales, housing starts, personal spending, and consumer confidence surveys. Importantly for the Federal Reserve, inflation edged higher to 3.0% and expectations for inflation over the next year and the next five years moved markedly higher as the nascent trade war was expected to cause higher prices. The Fed did not have a rate setting meeting in February, with the next one scheduled for March 18th and 19th.

Internationally, the trend to lower interest rates continued in the month. The Bank of England and the Reserve Bank of Australia cut their respective interest rates by 25 basis points, and the Reserve Bank of New Zealand reduced its rates by 50 basis points.

Canadian bond yields fluctuated with the constantly changing expectations of whether the 25% tariffs would or would not be imposed. Yields initially declined in chaotic trading on February 3rd following Trump’s weekend declaration that tariffs would be imposed. Once the start date of the tariffs was delayed until March 4th bond yields moved higher on expectations that the tariffs might never be imposed. However, renewed threats of the March 4th imposition of tariffs later in the month caused yields to fall sharply on concerns of the potential negative economic impact. Over the whole month, yields of 2-year and 30-year Canada bonds declined 9 and 12 basis points, respectively. Yields of mid term issues fell slightly more with 5-year and 10-year yields declining 14 and 17 basis points, respectively. In the United States, bond yields fell more sharply as investors were concerned that a potential global trade war would result in slower U.S. economic growth. The yields of U.S. Treasuries dropped 25 to 33 basis points across the various terms.

The federal sector returned 1.06% in February as lower yields resulted in higher bond prices. The provincial sector, which has a much longer average duration and is therefore more responsive to changes in yields, gained 1.37%. However, provincial bond returns were negatively impacted by their yield spreads widening 2 basis points because investors were concerned that a tariff war would slow economic growth and cause provincial budget deficits to increase substantially. Investment grade corporate bonds returned 0.79%, thereby underperforming government issues, as corporate yield spreads widened 6 basis points due to the economic uncertainty. High yield corporate issues earned 0.70% in the month, while preferred shares gained only 0.45% as volatile equity markets negatively impacted sentiment in that market.

A month ago, we thought it was unlikely that Trump would decide to impose 25% tariffs on all Canadian imports (excluding energy). It seems we were both right and wrong. As this is being written, the 25% tariffs were initially imposed on March 4th, but the automotive sector was spared a day later, and on March 6th tariffs on the 60% of Canadian imports covered under the USMCA free trade agreement (NAFTA 2.0) were delayed until at least April 2nd.

It is not known what Trump’s ultimate objective is with the tariffs threatened against Canada. The supposed goal of wanting to eliminate fentanyl smuggling and illegal immigration to the U.S. isn’t credible given how little there is of either coming from this country. As a result, it is difficult to anticipate what sectors will eventually be targeted and what the overall impact will be on the Canadian economy. At a minimum, the uncertainty is causing consumers and businesses to pause spending and investing, while taking a wait-and-see approach. Economic activity will likely slow in this environment.

We believe the domestic reaction in the United States to Trump’s trade war will be crucial regarding how the tariffs are imposed. Numerous sectors and industries in the U.S. recognize the fundamental importance of Canadian imports and are lobbying for the elimination or reduction of tariffs. The Big 3 auto manufacturers, for example, appear to have won a reduction in the tariff rate to 10%, as has the farming sector that needs Canadian potash for fertilizing its crops. Additionally, Trump appears sensitive to equity market weakness which, if it continues, should temper his policies.

In light of the uncertainty and the volatility, we are keeping portfolio durations close to benchmark levels. We believe the Bank of Canada will, as a precautionary measure, lower its interest rates by 25 basis points at its next announcement date of March 12th. Given current bond levels, though, there may not be much of a market reaction. The uncertainty also makes us cautious about adding corporate bonds. Indeed, we anticipate the allocation to the corporate sector will decline somewhat in the next few months as corporate maturities are reinvested in government bonds.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.