Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

March 7, 2024

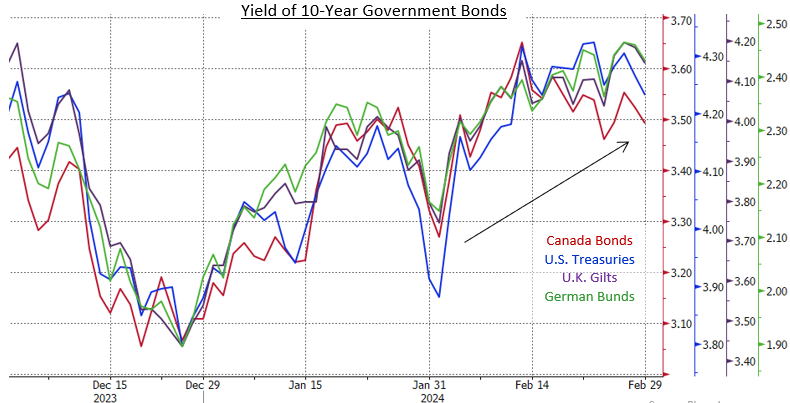

For the second consecutive month, global bond markets unwound some of the late 2023 optimism regarding central bank rate cuts. Yields of benchmark government bonds rose and their prices fell as inflation remained above the desired 2.0% level and economic activity was sufficiently strong to forestall urgent rate cuts. Notwithstanding the rise in bond yields, financial markets had a risk-on tone, with several equity markets including the U.S. S&P500 and the Japanese Nikkei hitting all-time highs. Better than expected sales and earnings from the AI chip maker, Nvidia, was a notable factor in the equity market strength. In the bond market, the risk-on sentiment led to narrower yield spreads for corporate and provincial bonds as investors sought to lock in what were perceived to be cyclical peaks in yields. The broad Bloomberg Canada Aggregate and FTSE Canada Universe indices returned -0.40% and -0.34%, respectively, in February.

The most noteworthy piece of Canadian economic data received in February was the Consumer Price Index. Prices were forecast to have risen 0.4% in January but were, in fact, unchanged. As a result, the annual rate of inflation fell to 2.9% from 3.4% the previous month. The core measures of inflation showed more modest improvement and remained above 3.0%. The better than expected inflation news caused a brief rally in bonds, but investors appeared to want confirmation that the improving trend would last. In other news, the unemployment rate declined to 5.7% from 5.8% due to good job creation and a slightly lower participation rate. Growth in average hourly wages decelerated but, at 5.3%, remained inconsistent with the 2% inflation target. In addition, Canadian economic growth in the final quarter of 2023 was estimated at an annual rate of 1.0%, slightly better than expected, while the third quarter contraction was revised upward from -1.1% to a slightly less worrisome -0.5% pace. On balance, the economic data showed the Canadian economy was performing below potential, but not so poorly that immediate monetary easing was required. The Bank of Canada did not have a rate setting announcement in February. Its next meeting is scheduled for March 6th, when it is expected to leave its trendsetting interest rates unchanged.

In the United States, the economic data was mixed, but provided little impetus for the Federal Reserve to lower interest rates in the next few months. Indeed, some forecasters began suggesting that the Fed might not cut rates at all in 2024. The estimate of U.S. GDP growth in the fourth quarter was revised slightly lower but, at 3.2%, suggested the U.S. economy was remarkably resilient. The unemployment rate remained at the very low 3.7% rate, while average hourly earnings accelerated to a 4.5% pace. Less positively, retail sales and housing starts were weaker than forecasts and consumer confidence unexpectedly declined. The Fed did not have a rate setting meeting in February. Its next meeting is scheduled for March 19th and 20th.

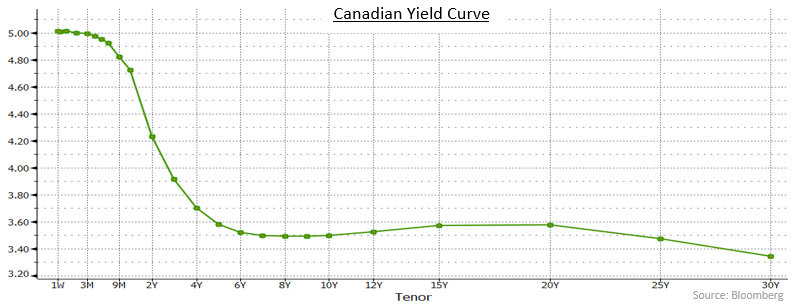

The Canadian yield curve became more inverted in February as shorter term yields rose more than long term ones. The yields of 2-year Canada bonds rose 19 basis points as investors lowered their expectations for a Bank of Canada rate reduction in the near future, while the yield of 30-year Canada bonds increased only 7 basis points. As can be observed in the following chart, the inversion is quite steep between money market securities and 5-year bonds. From 5-year maturities to long term bonds, however, the yield curve is relatively flat. In the United States, the yield curve also became more inverted in February, but the strength of the U.S. economy caused investors there to make larger revisions to their expectations for Fed rate reductions. The yield of 2-year Treasuries jumped 42 basis points higher, while 30-year Treasury yields rose 16 basis points.

Federal bonds returned -0.47% in February, as the higher yields pushed bond prices lower in the month. The provincial sector, which has a longer average duration, returned -0.60%. Provincial yield spreads were marginally narrower in the month. Investment grade corporate bonds returned +0.21% in the period, as their yield spreads narrowed a further 7 basis points in the month, continuing the tightening trend that began last November. The spread narrowing occurred despite relatively strong new issuance, with $12 billion of new issues in February compared with only $5.3 billion in the same month last year. Non-investment grade issues gained +0.83% in the month. Real Return Bonds returned -0.30% in February, substantially better than nominal bonds with similarly long durations despite the unexpected drop in CPI. Preferred share returns were close to those of corporate bonds, earning +0.13% in February.

We remain cautious about the bond market because we believe investors are too optimistic about inflation slowing and because of the potential for fewer interest rate cuts by the Bank of Canada than many investors are anticipating. While the January inflation data was a pleasant surprise, we are not confident that it is the start of a trend. The first six or seven months of each year is when Canada tends to experience the greatest inflationary pressures and 2024 is likely to be no different. Given the complexity of the economy and the potential for a second round of price increases well above the Bank of Canada’s target rate, we prefer to be patient about anticipating a return to the 2% objective.

The next couple of quarters may also determine whether the Canadian economy falls into a period of stagflation. Stagflation refers to an economy characterized by high inflation, low economic growth and high unemployment. At present, inflation is too high and economic growth is sputtering, but unemployment cannot be characterised as high. Should unemployment rise substantially from current levels, the Bank of Canada will have a dilemma because its actions to lower inflation may hurt the labour market.

As we noted last month, if and when the Bank of Canada begins lowering interest rates, a key consideration will be how low rates might go. For several years, the Bank has been estimating the “neutral” rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Given the recent bout with inflation, we believe the Bank will be reluctant to lower its target interest rate below 3.00%. We suspect that level differs from the expectations of investors who started their careers in the last fifteen years, a period when the Bank of Canada kept its interest rate well below 2.00%. We believe that period was an aberration, rather than the new normal, and the Bank will be reluctant to return interest rates to such low levels, given the negative consequences that included a housing bubble. Prior to the Great Financial Crisis, the Bank’s overnight target rates never went below 2.00% and yet the Canadian economy performed reasonably well. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period. And if money market yields do not fall below 3.00%, we do not see a lot of value in long term bonds currently yielding less than 3.50%.

At a time of economic uncertainty, the premium gained for taking on corporate credit risk has shrunk. The tightening of corporate yield spreads in recent months has brought them to below their average level since the Great Financial Crisis. In other words, the corporate sector has become somewhat expensive, which is making us cautious. We are particularly cautious regarding real estate issuers given their elevated leverage and the need to adjust cap rates to reflect current interest rates and bond yields. In addition, there is a concentration in equity market gains, particularly in the U.S. S&P500 where seven massive tech stocks are dominating the price performance of the other 493 index constituents. Any correction in equities will likely cause corporate yield spreads to widen noticeably. Should yield spreads continue to tighten, we may look at reducing exposure to the corporate sector.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.