Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 16, 2022

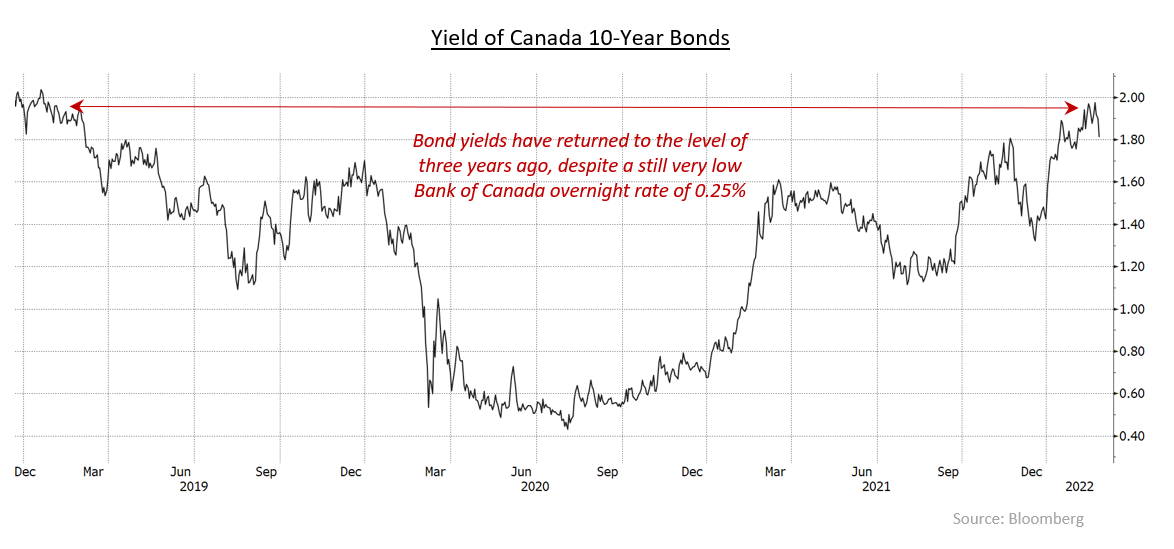

In February, bond prices initially traded lower and bond yields moved higher as Canadian inflation reached a multi-decade high and North American central banks were poised to soon begin their monetary policy tightening campaigns. By mid-month, Canadian and U.S. 10-year bond yields had risen to the psychologically important 2.00% level, which has not been seen since January 2019. Subsequently, yields leveled off due to the rising geopolitical tension surrounding Ukraine. Russia’s eventual decision to invade caused a flight to quality in the marketplace, so that risky assets such as equities and corporate bonds declined in value while government bonds reversed some of their earlier losses. Despite the seriousness of the invasion of Ukraine, central banks viewed it as a regional, rather than global, event. Consequently, the Bank of Canada and U.S. Federal Reserve appeared ready to begin raising interest rates in March. The FTSE Canada Universe Bond Index returned -0.72% in February.

Given that both Ontario and Quebec were in lockdown in January due to increased Covid-19 outbreaks, it was not surprising that Canadian economic data for that period showed weakness. Notably, employment contracted by 200,100 jobs, which caused the unemployment rate to jump to 6.5% from 5.9% the previous month. Retail sales fell during January, but Canadian inflation continued to increase, reaching 5.1%, its highest level in 30 years. However, a more positive piece of economic news received as this is being written showed that during the fourth quarter of last year Canada’s economy grew at a 6.7% pace, which was faster than both the market and the Bank of Canada expected. For all of 2021, Canadian gross domestic product expanded 4.6%, the largest increase in two decades. This gain in activity brought Canadian output back to pre-pandemic levels and should encourage the Bank of Canada to start reducing its monetary stimulus by raising interest rates.

In contrast to Canada, the U.S. economic data received in February showed continued growth. U.S. employment increased by 467,000, which was substantially higher than expected, and the positive revision to the previous month jobs growth more than doubled January’s increase. Retail sales were also higher than forecasts and U.S. headline inflation continued to climb, reaching 7.5%, while the core rate rose to 6.0%. U.S. headline and core inflation rates were both at their highest levels in 40 years, adding to the pressure on the Fed to quickly begin reducing its monetary stimulus that takes the form of both ultra-low interest rates and ongoing purchases of government bonds.

In February, the Canadian yield curve flattened by 11 basis points as bond yields of all maturities moved higher. Yields of 2-year Canada bonds rose by 17 basis points, five-year yields increased by only 1 basis point and 10 and 30-year yields by 6 basis points. In the U.S., the yield curve also flattened amid higher yields. U.S. 2-year yields increased 27 basis points while 30-year yields increased by 8 basis points, which resulted in the U.S. yield curve flattening 19 basis points. The more extreme flattening and sell off in the short end of the U.S. yield curve reflected the market’s expectation of the Fed having to be more aggressive in fighting a higher U.S. inflation rate. We believe the Fed will likely be increasing rates by 25 basis points increments, but the central bank is also very motivated to conduct quantitative tightening (reducing its holdings of U.S. Treasuries) to further increase monetary tightening.

In February, Canadian federal bonds returned -0.31% as rising yields caused bond prices to fall. Provincial bonds returned -0.87% in the month. Provincial performance suffered due to their longer average durations as yields increased and yield spreads that widened an average 2 basis points versus federal bonds. Investment grade corporate bonds returned -1.04% as corporate yield spreads widened an average 13 basis points in the month. Non-investment corporate bonds returned -1.22%, underperforming investment grade corporates due to their higher risk and lower liquidity in the face of pending central bank tightening and the Russia/Ukraine hostilities. Real Return Bonds returned -0.25%, which was markedly better than the return on nominal bonds with similarly long durations. This was likely due to North American inflation rates reaching multi-decade highs. Preferred shares returned -2.25%, apparently hurt by the risk-off sentiment during the period.

Following Russia starting to invade Ukraine, we increased the duration of the portfolios back to neutral. Provided the scope of Russia’s aggression does not expand beyond Ukraine, both the Bank of Canada and the Fed should start raising their respective interest rates in March. As the Russia/Ukraine situation develops, we may shift the durations back to more defensive levels. However, we are mindful that yields of 5 and 10-year Canada bonds are already up about 40 basis points since the beginning of the year and close to 150 basis points since the all-time lows yields of 2020. Given that neither the Bank of Canada nor the U.S. Federal Reserve have yet begun raising interest rates, the market has already discounted substantial monetary tightening.

Canadian and U.S. yield curves reached their steepest points in the spring of 2021. Since then, the yield curves have flattened dramatically in advance of anticipated monetary tightening. Similar to the upward move of bond yields, it is possible that the yield curve has flattened too far, too fast, and may experience some re-steepening when central banks actually begin to raise interest rates. However, North American Central Banks will raise interest rates multiple times in both 2022 and 2023, and we believe it is more likely that yield curve flattening will continue throughout this process, with the eventual possibility of yield curve inversion. Therefore, we are maintaining our lean to yield curve flattening in the portfolios.

The extraordinary economic stimulus in the form of accommodative monetary and fiscal policy that was provided during the pandemic helped corporate bonds to rally to historically expensive levels by the summer of 2021. At that time, given the expensive valuation, we were cautious regarding the positioning of corporate bonds in the portfolio. In the response to Omicron, geopolitical conflict and imminent monetary policy tightening, corporate credit spreads have moved sharply wider. With the cheapening of corporate bonds, we now see corporate credit as somewhat more attractive, and we are patiently looking for opportunities to add oversold corporates to the portfolios.

As this is being written, the Bank of Canada has raised its administered rates 0.25%, thereby commencing what is expected to be a series of several interest rate increases. The Bank’s move was expected and, as a result, does not change our strategic outlook.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.