Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

March 12, 2018

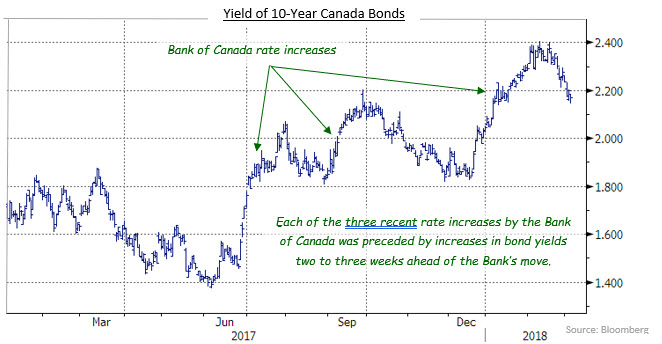

Notwithstanding the uncertainty, the most likely scenario is that the Bank of Canada will raise its administered rates in April. Based on the experience of the three recent increases by the Bank, the bond market will only anticipate the Bank’s move by a couple of weeks. That suggests that bond yields may drift sideways or lower for much of March before increasing near the end of the month.

From a longer term perspective, barring a surprise deceleration of the economy, the trend appears to be toward higher bond yields and lower prices. A synchronised global expansion is underway, and central banks are at various stages of lessening their respective stimulus programmes. In addition to interest rate increases, the extraordinary bond purchases known as quantitative easing (QE) are winding down. The Fed has already started to reduce its bond holdings, while the European Central Bank has substantially reduced its monthly purchases and plans to stop them altogether in September. The Bank of Japan has also started hinting that it may halt its QE in 2019. These three central banks’ bond purchases caused bond yields to fall to record lows in recent years, so the end of QE will likely result in bond yields moving higher again. Combined with anticipated future rate increases in the U.S. and Canada, that should push bond yields higher in the coming months. Accordingly, we are keeping portfolio durations shorter than respective benchmarks to reduce the negative impact of rising yields.

As we have noted in recent months, corporate yields spreads have narrowed to historically unattractive levels. In the current market environment, yield spreads could narrow further, but we believe it prudent to start reducing corporate exposure somewhat. With regard to the yield curve, we believe the flattening that has occurred in the last few months is overdone. Accordingly, we have structured portfolios to benefit from greater term differentials (i.e. a steepening of the yield curve).

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.