Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 8, 2025

The Canadian bond market experienced a second consecutive volatile month in December, with 10-year Canada bond yields again trading in a wide 40 basis point range. Despite interest rate reductions by the Bank of Canada and the U.S. Federal Reserve, most bond yields moved higher in the month, with a very weak U.S. market leading Canadian bond prices lower and yields higher. A major catalyst for the bond selloff was revised investor expectations for future interest rate cuts as both central banks warned that future moves would not occur as quickly as recent ones. Yearend illiquidity contributed to the volatility in the period. The FTSE Canada Universe Bond index returned -0.69% in December.

On December 11th, the Bank of Canada lowered its overnight interest rate by 50 basis points to 3.25%. In doing so, the Bank brought the rate down to the top of the 2.25% to 3.25% range that it estimated was neutral, neither restrictive nor stimulative for the economy. Consequently, the Bank suggested that going forward the pace of rate reductions would likely slow. Economic data received in the month confirmed that the Bank could slow its rate decreases. Better than expected economic indicators included GDP growth in October, which exceeded forecasts and showed annual growth accelerating to 1.9% from 1.6%, as well as strong manufacturing sales and housing starts. Job creation remained robust but the unemployment rate rose to 6.8% from 6.5%, due primarily to an increase in the participation rate to 65.1% from 64.8%. The headline rate of inflation edged down to 1.9% from 2.0%, but higher than expected core measures of inflation reinforced the Bank’s concern that inflation is not yet fully under control.

In the United States, the economy remained quite healthy. The estimated pace of GDP growth in the third quarter was revised up to 3.1% from 2.8%, suggesting even more momentum heading into the final quarter of the year. While the unemployment rate edged up to the still very low rate of 4.2%, job creation was robust and there was an unexpected jump in the number of unfilled job openings. The good labour situation encouraged consumers, leading to stronger than expected retail sales and better than expected sales of new vehicles. The Fed chose to lower its interest rates by 25 basis points on December 18th, but like the Bank of Canada, it warned investors that future rate reductions were likely to be slower, and a pause in rate cuts was a possibility. The better than expected economic data and the Fed’s warning about slower rate cuts contributed to a very weak U.S. bond market in December, which weighed on Canadian bonds in turn.

Internationally, the Swiss National Bank (SNB) unexpectedly lowered its policy rate by 50 basis points to 0.50%, its largest move in nearly 10 years. With inflation running below 1.0%, the SNB was focused on avoiding deflation and may also have wanted to discourage speculators from using the Swiss Franc as a safe haven. Elsewhere, the European Central Bank and Sweden’s Riksbank continued their monetary easing programmes, cutting their respective policy rates by 25 basis points in the month.

In December, the Canadian yield curve continued its shift toward a “normal” shape with longer term bond yields higher than shorter term yields. The rapid interest rate cuts by the Bank of Canada, including the one in December, have eliminated the inversion of the yield curve because short term bond yields have fallen sharply. At the same time, longer term bond yields have drifted higher as investors reacted to higher yields in the United States and as expectations of the Bank of Canada’s terminal rate have been revised higher. In the month, the yield of 2-year Canada bonds declined 9 basis points, while 30-year bond yields rose 22 basis points. By the end of the month, 2-year bond yields had moved lower than 5-year bond yields for the first time in 2½ years. In the United States, the Treasury yield curve also steepened significantly, and in a more dramatic fashion. The yield of 2-year Treasury bonds rose 7 basis points, while 30-year yields surged a remarkable 43 basis points. The Fed’s hawkish rate cut and the robust GDP data caused investors to reduce their forecasts of future Fed rate cuts.

The federal bond sector returned -0.43% in the month as higher yields caused longer term bond prices to fall. The provincial sector returned -1.42%, as its longer average duration and the bigger increases in long term yields hurt the sector’s performance. Investor demand for investment grade corporate bonds remained strong, leading to mid and long term yield spreads compressing another 6 basis points in the month. As a result, investment grade corporate bonds performed better than the government sectors, declining only 0.14%. Non-investment grade corporate bonds gained 0.79% and Real Return Bonds returned -0.76%, which was substantially better than nominal bonds with similarly long durations. Preferred shares capped a remarkable year with another robust gain, earning 2.59% in December.

The Bank of Canada’s warning that future interest rate cuts would occur at a slower pace was not a surprise. For some months we have been pointing out that the Bank’s terminal rate (where it stops lowering rates) is more important than the pace the Bank arrives at it. We believe the Bank will probably lower rates by 25 basis points twice more in the first quarter of 2025. If that happens, the overnight target will be 2.75%, the midpoint of the Bank’s neutral range estimate. That seems like a reasonable point for the Bank of Canada to at least pause, given the economy is not in a recession, the scale and pace of easing since the Bank began lowering interest rates last June, and the lag with which the economy responds to rate changes.

In the current environment, with the Bank of Canada still easing monetary policy, the yield curve should continue to normalize. Short term yields are likely to move further below longer term yields, resulting in a steeper slope to the yield curve. However, if we are correct that the Bank may pause when its overnight rate is at 2.75%, there is not much room for shorter term bonds to rally given that 2-year Canada bond yields are already below 3.00%. That means additional steepening of the yield curve may occur with longer term yields rising without shorter term yields falling. As a result, we are cautious about the prospects for a bond market rally.

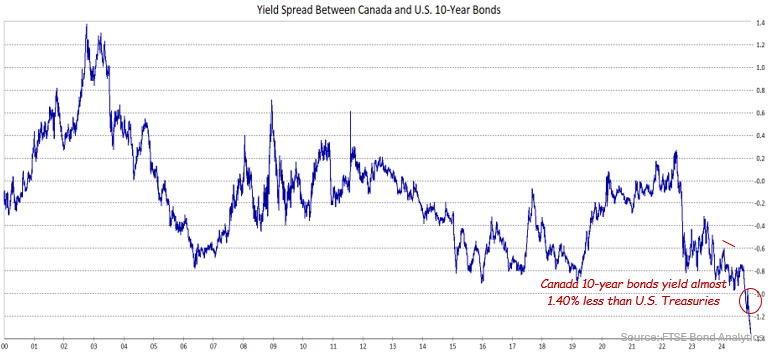

Another reason for our caution is that Canadian bonds are more expensive (lower yielding) relative to U.S. bonds than they have ever been before. While much of the recent widening between Canadian and U.S. yields was due to concerns about president-elect Trump’s economic policies and the already massive U.S. fiscal deficit, Canadian bonds are not particularly attractive for international investors.

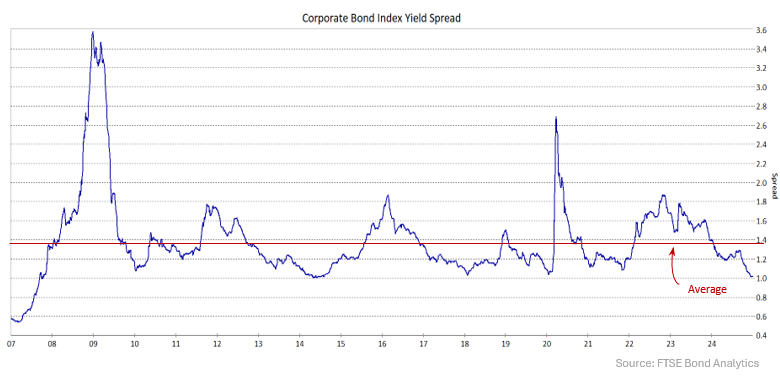

We also note that the recent compression in corporate bond yield spreads has shrunk the average risk premium to its smallest level since the 2008-2009 Financial Crisis. Corporate bond spreads versus provincials are also at multi-year tight levels. While spreads could theoretically narrow further, we believe there is more risk that they widen, which would lead to corporate issues underperforming government bonds. Potential catalysts for corporate spreads to widen include an equity market correction (think of tech stock valuations) or an economic slowdown (possibly caused by punitive U.S. tarrifs). As a result, we are keeping the corporate sector allocation close to neutral and using pension fund bonds as high quality substitutes.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.