Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 12, 2022

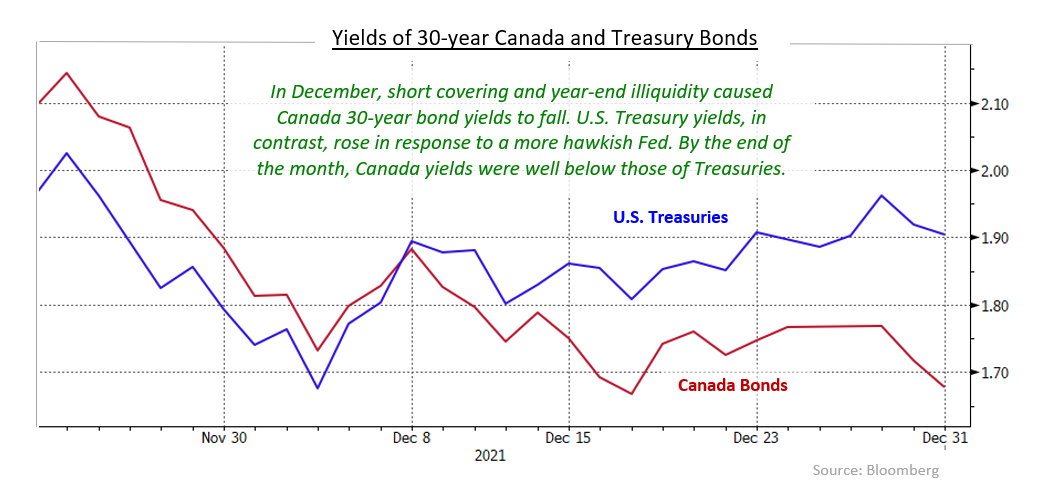

North American bond yields experienced some volatility in December. Concerns about the impact of the Covid-19 Omicron variant continued to generate a flight-to-quality bid in the bond market at the beginning of the month, causing yields to fall and prices to rise. In Canada, significant purchases by an Asian central bank were also supportive of bond prices. However, North American central banks were looking past Omicron and suggested that their respective economies were progressing such that tighter monetary policy would be required in early 2022. That pushed bond yields higher and prices lower toward month end, particularly in the United States, as the Federal Reserve indicated it would reduce monetary stimulus more rapidly than previously thought. The Fed’s more hawkish stance, combined with yearend illiquidity and short covering, helped the Canada bond market to outperform the U.S. market in December as Canada bonds generated positive returns while U.S. bonds declined. The FTSE Canada Universe Bond Index returned 1.67% in December.

Canadian economic data had a strong showing in December. Employment increased strongly by 153,700 which lowered the unemployment rate to 6.0% from 6.7% the month before. Headline retail sales were also stronger than expected and the Canadian year-over-year inflation rate held at 4.7%, the highest level in 18 years. Inflation has now been above the 2% Bank of Canada target level for nine consecutive months. The Bank of Canada, as expected, held its overnight rate at 0.25%. The Bank is expected to initiate its first rate hike in March of 2022, although lockdowns associated with the Omicron variant could possibly delay monetary tightening.

The U.S. economy during the period saw employment increase by 210,000, which was lower than expected. Retail sales were also lower than expected. Despite these two major economic indicators falling below expectations, the weekly initial claims for state unemployment benefits fell to only 184,000, which was the lowest since 1969 and was consistent with the ongoing recovery of the U.S. labour market. The strong jobs situation, combined with very accommodative U.S. monetary policy, caused inflation to climb further, with annual headline inflation reaching 6.8%, while the core rate of inflation rose to 4.9%. The headline and core inflation rates were at their highest levels in 40 and 30 years, respectively.

As expected, the U.S. Federal Reserve left its administered interest rates unchanged at the conclusion of its mid-December meeting. However, owing to “inflation developments and the further improvement in the labor market”, the Fed decided to make sharper reductions in its monthly purchases of government bonds. As a result, its asset purchases will end by mid-March instead of mid-June. Because the Fed wants to conclude the monetary stimulus provided by quantitative easing before it starts tightening monetary policy with interest rate increases, the bond purchase programme needed to be wound up more rapidly. In the press conference following the Fed meeting, Chair Powell indicated that he did not foresee a long delay between the end of QE and the start of monetary tightening. The U.S. bond market reacted to the change in the Fed’s stance with bond prices falling and yields rising over the balance of the month.

In December, Canadian bond yields declined and the yield curve continued to flatten. The yield on 2-year Canada bonds dropped 4 basis points while 30-year yields fell 22 basis points, so that the difference between the two maturities decreased by 18 basis points. Mid-term bonds rallied as well, with 5-year and 10-year yields falling 15 basis points and 16 basis points, respectively. In the U.S., the yield curve flattened like the Canadian yield curve, but bond yields actually rose across the maturity spectrum rather than falling. The U.S. yield curve flattened because 2-year and 5-year Treasury yields increased more than the yields of longer term issues. This shift was driven by the Fed increasing its pace of tapering QE and the resultant market repricing the timing of the first rate increases to the spring of 2022.

Canadian federal bonds returned 1.19% as the falling yields caused bond prices to rise. Provincial bonds returned 2.22% in the month, benefiting from their longer average durations and the greater decline in long term yields. Investment grade corporate bonds returned 1.50% in December. Interestingly, the yield spreads of both provincial and corporate bonds tracked the overall flattening of the yield curve, as short term spreads widened while long term spreads compressed. Non-investment grade bonds returned 0.37% in the month. Real Return Bonds returned 3.64%, which was substantially better than the return on nominal bonds, due to the continued high rate of inflation. Preferred shares earned 1.33% during the month as redemptions in that market spurred reinvestment buying.

The potential economic shock from the Omicron variant is concerning, and it may provide some near-term support for the bond market. However, North American central banks seem willing to look past the current pandemic wave and are confident in economic growth. They are more focussed on excessive inflationary pressures and are positioned to begin tightening monetary policy in the first half of 2022. It has been our view that inflation pressures can be sticky and that central banks will need to be more proactive in addressing them. We expect, as vaccinations and boosters continue to increase across the population, the current phase of lockdowns will be shorter in term and the Canadian economy will continue to recover.

The Bank of Canada has ended its QE and the Fed has accelerated its QE tapering such that its bond purchases will end by March 2022. The elimination of these massive buying programmes combined with ongoing government deficits should provide significant upward pressure on bond yields. As the Bank of Canada and the Fed transition to tighter monetary policy, bond yields should continue to rise from the current low levels. We are also mindful of the short term run up in bond prices at the end of the year, and the potential for that to be unwound. (Indeed, some unwinding is occurring as this is being written.) As a result, we are maintaining a defensive stance in portfolio durations with positions that are shorter than their underlying benchmarks.

With both the Bank of Canada and the Fed now expected to begin raising rates in the first half of 2022, yield curves have flattened dramatically. In past cycles, yield curve flattening has usually occurred only after the central banks started raising interest rates, so this cycle has a greater degree on anticipation. It is possible that yield curves have moved too far, too fast, and may experience a “sell-the-fact” re-steepening when central banks actually begin raising rates. However, it is likely that North American interest rates will be increased multiple times in both 2022 and 2023, and we believe yield curve flattening will continue further into that timeline.

The pandemic-related lockdowns and other restrictions have constrained many types of spending and has generated considerable pent-up demand as a result. That pent-up demand will likely spur robust economic growth in 2022 and provide firm support for the corporate credit market. While the corporate credit outlook remains attractive, we are mindful of the relatively expensive valuations of corporate bonds versus historical levels and the potential for substantial corporate new issue supply. Consequently, we are being cautious about adding to our corporate allocations.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.