Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 10, 2019

We believe that the recent volatility in equity markets is an over-reaction to slower growth prospects combined with unwinding of excessive speculation following an unbroken rally since the financial crisis ten years ago. As investors realize that a recession is not in the cards for 2019, the risk-off market sentiment will fade, as will the flight-to-safety bid for bonds. We anticipate that bonds will give back their recent price gains over the coming months. Accordingly, we have reduced portfolio durations modestly below benchmark levels, and we anticipate becoming even more defensive in the near future.

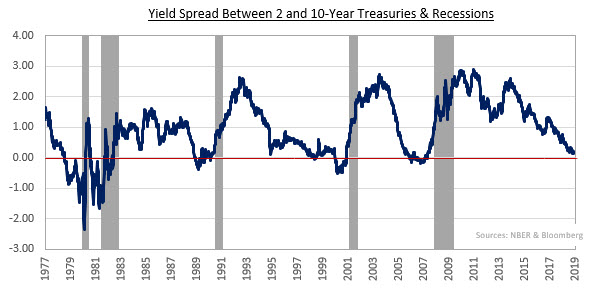

There has been considerable discussion whether the recent flattening of the yield curve is predicting a recession. In the following chart, the differential between 2 and 10-year U.S. Treasury Bond yields is used to indicate the steepness of the yield curve. When the value goes below zero, 2-year bond yields are higher than 10-year ones and the yield curve is said to be inverted. Recessions are indicated by the gray bars. Some observers believe an inverted yield curve is a good predictor of recessions. However, as can be observed, the yield curve has been quite flat or even inverted for years without a recession occurring. Indeed, in the 1990’s, the yield curve was quite flat for several years without any economic slowdown. So, we would suggest discounting the use of the yield curve as a good economic indicator.

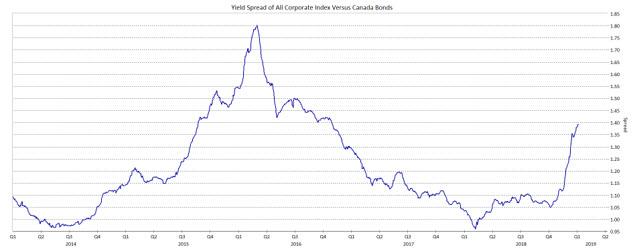

With regard to our sector allocation strategy, we note that the widening of corporate yield spreads in recent months has been only a fraction of the move experienced between 2014 and 2016. However, the level of spreads is more attractive than the average of the last several years. As a result, we are looking for opportunities to increase the corporate allocation. We will be concentrating on issuers with the financial strength to weather any economic slowdown in 2020 or 2021, should it occur.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.