Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 20, 2017

The Canadian bond market declined for the third consecutive month in December. Driving forces within the market included an interest rate increase by the U.S. central bank, the Federal Reserve, and speculation the European Central Bank would eventually wind down its quantitative easing programme. In addition, the U.S. presidential transition continued to roil bond markets because of the anticipation for substantial fiscal stimulus, faster economic growth, and wider budget deficits. Bond yields rose and prices fell in the first half of the month before bargain hunting by some investors led to a partial recovery in the second half of the month. The FTSE TMX Canada Universe Bond index returned -0.50% in December.

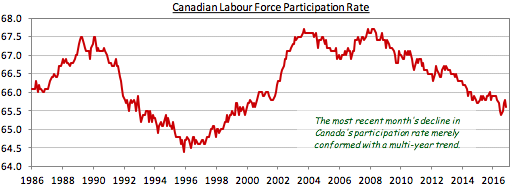

Canadian economic data received in December was mixed, and provided little impetus for the Bank of Canada to adjust monetary policy. On the positive side, retail sales grew more than expected and the trade deficit shrank more than forecast as exports rose and imports fell sharply after an outsized transaction the previous month. The unemployment rate fell to 6.8% from 7.0%, but the improvement was due primarily to a drop in the participation rate to 65.6% from 65.8%. The drop in the participation rate extended a trend going back several years that is likely due to the Baby Boomer demographic cohort starting to retire. Negative economic news included an unexpected decline in the October GDP level and weaker than expected manufacturing sales. Inflation was below forecasts, with CPI falling to 1.2% from 1.4% the previous month. At its scheduled rate-setting meeting, the Bank of Canada left interest rates unchanged.

U.S. economic data was, on balance, positive. The cyclical housing sector continued its long recovery with existing home sales at their fastest pace since May 2007 and new home sales at the second strongest rate since 2008. As a consequence, homebuilder confidence jumped to the highest level since 2005. Consumer and business confidence surveys were more optimistic than expected and investment spending by business continued to improve. Unemployment fell to 4.6% from 4.9%, in part due to a lower participation rate, but it still suggested that the U.S. economy is close to full employment. With CPI inflation edging higher to 1.7%, the Fed did the expected and raised its administered interest rates by 25 basis points at its December 14th meeting. Interestingly, bond yields actually fell over the balance of the month even though the Fed statement was more hawkish than expected.

Overseas, the key development was the decision by the European Central Bank early in the month to extend its quantitative easing programme. Originally scheduled to end in March 2017, the ECB purchases of bonds will now continue until next December. The monthly size of the purchases, however, will be reduced from €80 billion to €60 billion. The president of the ECB, Mario Draghi, claimed that the reduction in size was not “tapering”, referring to how the U.S. Fed wound down its quantitative easing programme in 2014. Investors were sceptical of Draghi’s assertion and they began discounting the potential of the ECB finally ending its quantitative easing. As the ECB’s bond purchases in recent years have pushed global yields to record lows, the termination of quantitative easing could lead to a sharp rise in yields, and as a result investors became more cautious regarding bonds.

The O.P.E.C. agreement to limit oil production, reached in late November, was supportive of oil prices through December, resulting in the WTI price surging over 8% and hitting US$54/barrel for the first time this year. The Canadian dollar initially rose versus the U.S. dollar on the strength of the oil price increase. However, following the Fed’s interest rate increase, the Loonie swooned and gave back all of its gains to finish the month little changed. With the Fed poised to raise rates again in 2017 and the Bank of Canada at best on hold, the divergent monetary policies clearly favoured the U.S. currency. Even so, the Canadian dollar fared better than most other major currencies in the month.

The Canadian yield curve steepened somewhat in December as shorter term yields rose less than longer term ones. For example, 2-year Canada Bond yields moved up 5 basis points while 30-year yields rose 15 basis points. With the Bank of Canada not expected to raise its administered interest rates for at least a year, with a possibility of an interest rate reduction in 2017, the yield of 2-year bonds had limited scope to increase. Longer term yields, however, had no constraint on their increases. Unusually, the increase in longer term Canadian bond yields exceeded the increase in comparable U.S. bond yields in December. Domestic selling of bonds in Canada contrasted with a large asset allocation shift from stocks to bonds in the United States, accounting for the different performance.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.