Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

September 11, 2023

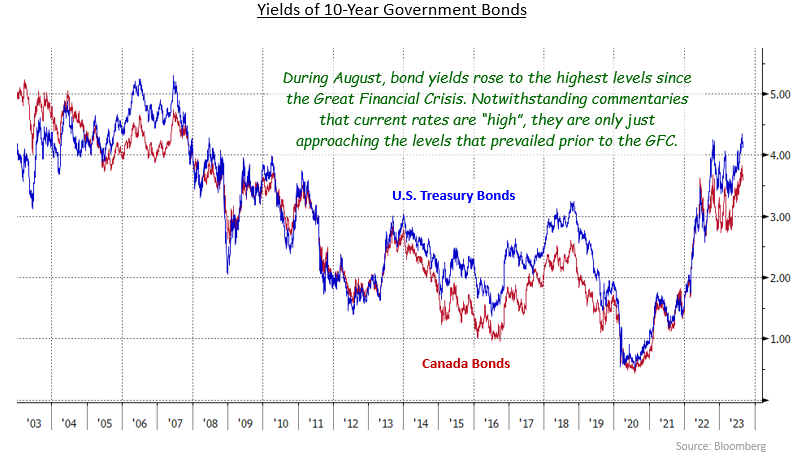

Global bond yields moved higher in August as economic growth remained positive while inflation stayed above central bankers’ comfort zones, and in some cases started reaccelerating. In North America, Canadian and American bond yields hit their highest levels since the Great Financial Crisis before easing back somewhat. The rise in yields reflected investor expectations that monetary policy would need to remain restrictive for longer than previously thought necessary to bring inflation under control. Later in the month, some secondary economic data suggested the U.S. labour market was weakening and that led to bonds reversing some of their earlier losses. Central bank activity was muted as the Bank of Canada, U.S. Federal Reserve, and European Central Bank did not have rate setting meetings in the month. The Bloomberg Canada Aggregate and FTSE Canada Universe indices declined 0.23% and 0.18%, respectively, in August.

Canadian economic data released in August was somewhat limited. The unemployment rate edged up to 5.5% from 5.4% the previous month. A small decline in the number of jobs was partially to blame, as was a slight drop in the participation rate. Of note, the unemployment rate has jumped from 5.0% to 5.5% in only three months, and that rapid increase led to some speculation that the economy was about to tip into a recession. However, the labour market data also showed that the increase in average hourly wages accelerated from 3.9% to 5.0%, suggesting the Bank of Canada’s monetary tightening has yet to be fully effective. Reinforcing that was Consumer Price Index (CPI) data that showed a larger than expected 0.6% increase in the most recent month and a jump in annual inflation from 2.8% to 3.3% a month earlier.

U.S. economic news in August was mixed. On the positive side, the unemployment rate declined to 3.5% from 3.6% the previous month, industrial production was better than expected on more robust manufacturing activity, and retail sales were surprisingly strong. On the negative side, the estimated growth rate of U.S. GDP in the second quarter was revised lower from 2.4% to 2.1%. As well, consumer confidence fell sharply, and the number of unfilled job openings declined markedly. Inflation, though, edged higher, with U.S. CPI rising to 3.2% from 3.0%.

Internationally, economic activity was mixed in Europe, with its largest economy, Germany, experiencing weakness. Inflation, however, remained stubbornly above 5% in the Eurozone, putting pressure on the European Central Bank to consider another interest rate increase at its September 14th meeting. In China, the government introduced a series of incremental interest rate reductions and tax cut to try to stimulate disappointing economic growth and bolster a weak real estate market. News of Chinese economic weakness tended to result in weaker industrial commodity prices and better global bond prices.

The yield of 2-year Canada bonds closed 3 basis points lower in August, while the yields of 5, 10, and 30-year Canada bonds rose between 6 and 9 basis points. The relatively small net changes in yields belie the volatility during the month as yields across the maturity spectrum fluctuated in wide 30 to 35 basis point ranges. The shift in U.S. Treasury yields was similar, but more pronounced. The yield of 2-year Treasuries also declined 3 basis points while 10-year and 30-year Treasury yields rose 26 and 18 basis points, respectively. The yield range of 10-year Treasuries was a remarkable 50 basis points in the month.

The federal sector of the Canadian bond market returned exactly 0.00% in August as the decline in bond prices was offset by interest income. The provincial sector returned -0.45%, because the longer average duration of provincial bonds increased the impact of high yields. Investment grade corporate bonds returned -0.09% as their yield spreads widened an average of 5 basis points in the period. Non-investment grade corporate bonds earned +0.37%, as their higher yields more than offset declines in their prices. Real return bonds declined 1.35% on average, slightly underperforming nominal bonds of similar durations. Preferred shares were quite weak in August, declining 4.21%. Liquidation of a fairly large preferred share portfolio was likely a contributing factor.

As this is being written, Canadian GDP for the second quarter of the year has been reported to have declined an annual rate of 0.2%, much weaker the expected growth of 1.2%. While much of the shortfall was due to reduced inventory accumulation (which can be reversed in coming quarters), and final domestic demand grew by 1.0% in the quarter, we do not disagree with forecasts that the Bank of Canada will hold interest rates unchanged at its September 6th announcement. However, whether the Bank needs to raise rate again, perhaps as soon as its October meeting, will be determined by inflation rather than by the pace of economic growth. That is a concern because inflation appears to be strengthening again despite the substantial increase in interest rates in the last year and a half. We anticipate the annual increase in CPI will accelerate to above 4.0% in the coming months and that will force the Bank of Canada to raise interest rates again. Reasons for the resurgence in the inflation rate will include base year effects as weak increases from a year ago fall out of the calculation, oil prices that have rebounded to the highest level in 10 months, ongoing mortgage rate increases, elevated wage settlements, and a decline in the Canadian exchange rate. Given the likelihood of additional monetary tightening, we believe it appropriate to keep portfolio durations defensively positioned, shorter than the benchmarks.

Even if the Bank of Canada does not increase rates further, it is unlikely to lower rates for several quarters. Consequently, we believe the risk of a recession beginning in the next few quarters is significant. Indeed, a recession may be required to bring inflation back to the 2% target on a lasting basis. Importantly, we believe the Bank of Canada is willing to tolerate a recession as it struggles to control inflation. Should a recession occur, we would expect corporate yield spreads to widen sharply in reaction to the heightened credit risk. Alternatively, a sharp selloff in equity markets could be the catalyst for significant widening of corporate yield spreads. Given what we perceive to be elevated risk, we are continuing to reduce the exposure of the corporate sector in client portfolios.

As we noted last month, the yield curve is still adjusting to interest rates needing to stay higher for longer and longer term bonds look most vulnerable to higher yields. Eventually, we expect the yield curve will normalize from its current inverted shape, either through higher long term yields or lower short and mid term yields. Accordingly, we have begun to shift the portfolio structure to benefit from long term bond yields moving higher relative to mid term bond yields.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.