Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

September 9, 2022

The bear market rally in the bond market that lasted from mid June to late July ended as bond prices fell and yields rose in August. Neither the Bank of Canada nor the U.S. Federal Reserve had active meetings during the month, but both central banks were vocal in stating their resolve to tighten monetary policy until inflation returned to their 2% targets. Indeed, the market began to believe that the Bank of Canada and the Fed would continue to tighten monetary policy to fight inflation, even if the economy falls into recession. In anticipation of higher money market yields, bond investors demanded higher yields. Globally, many other central banks continued to tighten monetary policy, including the Bank of England which raised its benchmark interest rate by 50 basis-points, the first hike of that magnitude in 27 years. The Reserve Banks of Australia and New Zealand, as well as Norway’s Norges Bank, each made similar rate increases in the month. This showed a concerted global effort by central banks to return inflationary pressures back to acceptable levels. The FTSE Canada Universe Bond Index returned -2.74% in August.

Canadian economic data released in August was mixed. July’s employment declined by 30,600. Despite the fall in employment the unemployment rate held at an all time low of 4.9% as the participation rate also declined. Canada’s GDP expanded at a 3.3% annualized real rate in the second quarter which was higher than the previous quarter, although below market expectations. On a nominal basis (i.e. including inflation) Canadian GDP increased at an eye-popping 17.9% pace in the quarter. However, the economy seemed to be losing momentum with June growth showing a moderate 0.1% expansion. Expectations are for annualized real growth to fall below 1.5% in the second half of the year with a substantial possibility of recession due to aggressive rate hikes by the Bank of Canada. June’s retail spending was stronger than expected, but most of the increase was due to higher prices, particularly for gasoline. The Canadian housing sector continued to see lower home sales, declining by 5.3%, as well as falling prices. Year-over-year inflation declined moderately from the prior month’s peak to 7.6% in July, but this remains far from the 2% target. The Bank of Canada is expected to raise the overnight rate by 75 basis-points at their September 7th meeting. [As this is being written, the Bank of Canada has raised rates by the expected 75 basis points.]

Major U.S. economic releases were strong in August as job creation was much higher than expected at 528,000, which pushed the unemployment rate down to the all time low level of 3.5%. Other data showed inflation declined from its peak from last month, but still high at 8.5%. At the Jackson Hole economic conference in late August, Fed Chairman Powell stated, “Restoring price stability will likely require maintaining a restrictive policy stance for some time”, which showed that the Fed, like the Bank of Canada, was willing to keep raising interest rates to slow inflation, even if it causes a recession. The relatively hawkish comment led to further declines in bond prices and higher yields. The Fed is expected to raise interest rates by 75 basis points at their September meeting.

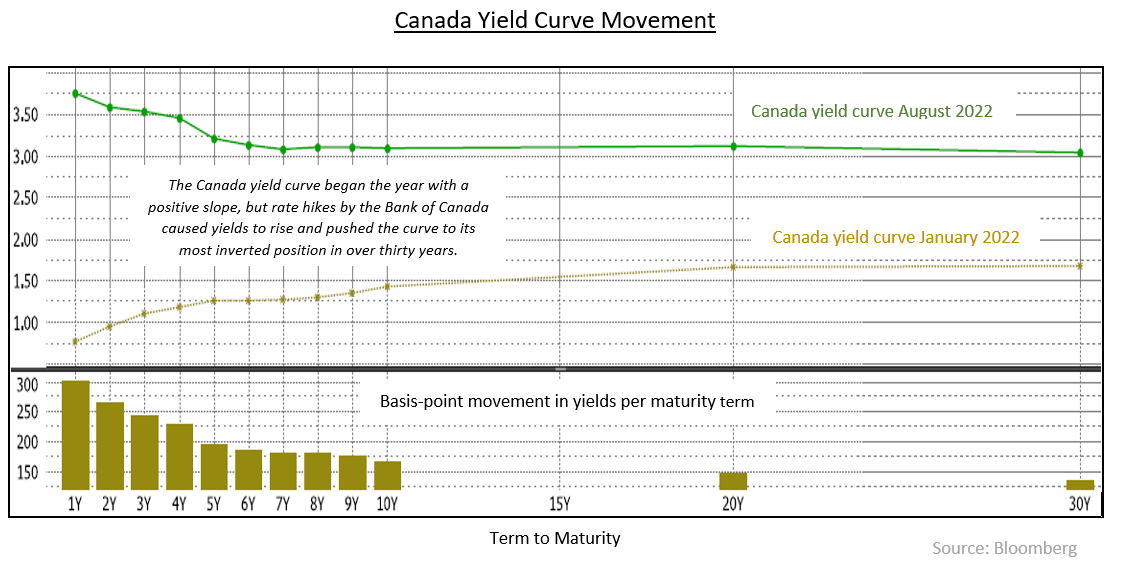

In August, the Canadian yield curve inverted further as 2-year Canada bond yields increased 68 basis points while 30-year yields rose 25 basis points. Currently, the spread between the 2-year and 30-year bond yields has reached a level of -62 basis points, which is the most inverted the Canada yield curve has been in over thirty years. Mid-term yields also rose with 5 and 10-year yields increasing 66 and 50 basis points, respectively. In the United States, the yield curve also inverted further as 2-year Treasury yields increased 61 basis-points while 30-year yields rose 28 basis points. Mid-term bond yields also rose with 5 and 10-year Treasury yields increasing 68 and 54 basis points, respectively. The dramatic reversal in market direction from July spoke to North American central banks’ commitment to raising interest rates to fight inflation, which the market now believes may take longer than originally expected.

The federal bond sector returned -2.62% in August as yields reverted to higher levels resulting in falling bond prices. The provincial sector returned -3.44%. Provincial bonds suffered from a combination longer average durations and spread widening during the period. The investment grade corporate bond sector earned -1.95% as it also suffered from higher yields. Non-investment grade bonds earned +0.05%, outperforming investment grade bonds due to low new issuance, combined with shorter durations and higher coupons. Real Return Bonds returned -4.31%, essentially in line with nominal federal bonds of similar duration. Preferred shares demonstrated their usual lack of correlation with bonds, earning +1.12% in the month.

It is not surprising to see volatility emerge in markets as central banks instigate aggressive monetary policy tightening. In June, Canada and U.S. 10-year bonds sold off and reached a recent high yield of 3.50%. By the end of July those 10-year bonds had rallied substantially as their yields declined 100 basis points to reach 2.50%. The market was expecting that aggressive interest rate increases would quickly cause a recession and that, in turn, would force central banks to lower interest rates. We were not believers of this simplistic view. Instead, we thought inflation would be challenging to break and central banks will have to continue increase interest rates, regardless of a potential recession. Both the Bank of Canada and the Fed confirmed our thinking in August, which led to the rise in bond yields.

For much of August we maintained a short duration position to protect portfolios from the impact of rising yields. Late in the month, we shifted durations back to neutral due to concerns about market volatility. We anticipate returning the portfolio durations to a more defensive level in the coming weeks. With our conviction that central banks will continue to raise rates to fight inflation despite the risk of recession, we are comfortable maintaining an underweight position in the mid-term sector of the market because those bonds are likely to underperform as the yield curve inversion increases.

With both the Bank of Canada and the Fed expected to continue their interest rate increases in September, the risk of a recession by the end of this year or the beginning of 2023 is a strong possibility. Corporate credit has been under pressure so far this year, but we would expect to see credit spreads widen further as the risk of a serious recession increases. Consequently, we have positioned corporate holdings in the portfolio towards high quality and we have been very conservative in adding new positions. We are willing to be patient and look to take advantage of wider credit spreads as they occur in a slowing economy.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.