Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

September 6, 2021

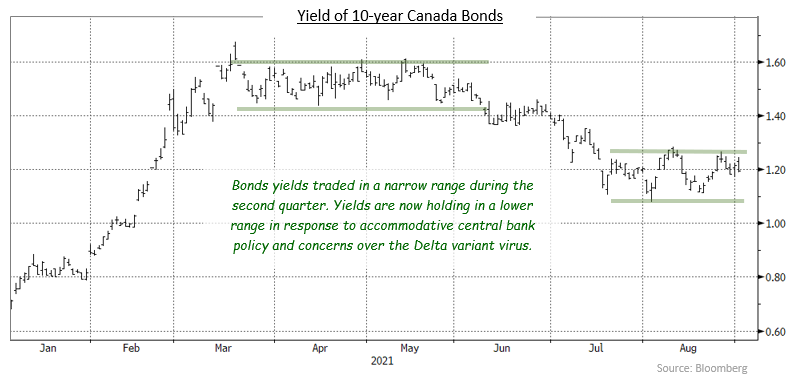

Bond yields fluctuated in a narrow band in August as vacations led to lower trading volumes. Investors continued to express concern of the spread of the Delta variant virus and central banks held to their accommodative policy stance rhetoric. Economic data was generally positive in both Canada and the United States, but investor reaction to economic news remained apathetic. The FTSE Canada Universe Bond index returned -0.12% in the month.

Canadian economic data received in August was mixed. The tough third-wave restrictions, alongside multiple supply chain challenges, stifled Canadian economic activity in the spring much more than expected. Canadian GDP shrank by 1.1% in the second quarter, substantially worse the 2.5% growth rate expected by the market. Canadian unemployment declined more modestly than expected, from 7.8% to 7.5%, but the quality of job creation was strong as full-time jobs made up the vast majority of new positions. Following the removal of third-wave lockdowns, retail sales advanced strongly. However, much of the boost in spending was driven by price increases instead of volume gains, as year-over-year inflation continued to climb, reaching a 10-year high of 3.7%. This, combined with commodity price gains still feeding through the economy, leads us to believe that the risk for inflation remains tilted to the upside.

U.S. economic data during the month were strong and included second quarter GDP growth at a robust 6.6% annual pace. Employment increased by 943,000 with an upward revision to the previous month and wages rose by a strong 0.4% as employers continued to pay up to entice workers back into the labor market. Retail sales surprised the market by declining, but this likely reflected a shift to spending on services versus goods. U.S. prices continued to climb with monthly inflation increasing 0.5% and year-over-year inflation holding a 13-year high of 5.4%. Core inflation, at 4.3%, was close to 30-year highs.

Neither the Bank of Canada nor the U.S. Federal Reserve met in August, so guidance from the North American central banks during the month was minimal. However, at the Jackson Hole Economic Symposium of Central Bankers, Fed Chairman Jerome Powell confirmed that accommodative monetary policy would remain in place but tapering of the U.S. quantitative easing program would likely commence in the autumn of this year.

During August, most bond yields rose moderately, and the Canadian yield curve steepened as 2-year Canada bond yields declined 2 basis points while 30-year yields increased by 3 basis points, so that the spread between the two maturities increased by 5 basis points. Mid-term bonds traded in a like fashion with 5-year and 10-year yields increasing 3 basis points and 2 basis points, respectively. U.S. Treasuries performed similarly to Canada bonds, although U.S. mid-term bonds underperformed as their 5-year and 10-year yields rose 7 basis points during the period.

Canadian federal bonds returned -0.07% as the moderately higher yields caused bond prices to decline. Provincial bonds returned -0.26% in the month. The longer average duration of the provincial sector led to its underperformance as yields increased while provincial yield spreads were little changed. Investment grade corporate bonds returned +0.01%. Short and mid-term corporate bonds generated small positive returns while long-term corporates underperformed with the slight rise in yields. Non-investment grade bonds returned +0.37%, outperforming higher quality issues during the period as riskier assets continued to perform well. Real Return Bonds, which have quite long average durations, returned -0.38%. Preferred shares gained +1.06% in August as redemptions created demand for replacement issues.

While the Bank of Canada and the Fed continue to have accommodative monetary stances, we believe that the recent low level in bond yields has been primarily driven by a flight-to-quality arising from fears of an economic slowdown due to the rise of the Delta variant virus and supply chain disruptions. We also believe international demand for the safe haven of North American bonds may have played a role in the recent rally. However, it is our view that, despite the recent second quarter decline in Canadian GDP, well vaccinated developed nations such as Canada will be able to stifle the spread of the virus and pent-up consumer demand will spur rapid growth as restrictions are removed and economies are reopened. In this environment, inflation may continue to build, and investors will likely demand higher yields to compensate them for the decay of fixed income streams from inflationary pressures. In addition, continued massive issuance of government bonds combined with declining central bank buying should provide significant upward pressure on yields. As a result, we are maintaining a defensive stance in portfolio durations with positioning that is shorter than underlying benchmarks.

Despite Canada recent weak economic performance, we expect to see the Bank of Canada continue to reduce its QE bond purchasing program, with its next reduction likely coming in October. In addition, the Bank of Canada and the U.S. Federal Reserve are both expected to begin raising interest rates in the second half of 2022. Since the beginning of the spread of the Covid virus, the central banks’ extreme accommodative monetary policies have led to a steepening of the yield curve. Now that economies are poised to begin reopening, yield curves should begin to flatten as the central banks “take their foot off the gas” to normalize monetary policy. This normalization will push the short and mid term part of the yield curve higher relative to longer term yields.

Looking ahead to the third quarter, we expect, as vaccinations increase across the population, lockdowns should recede, and the economy will continue to prosper as more businesses reopen. The Canadian household savings rate reached 14.2%, so considerable base and pent-up demand will likely spur robust growth over the remainder of 2021 and 2022. This strong demand growth will provide firm support for the corporate credit market. While the corporate credit backdrop looks attractive and we are comfortable positioning in the sector, we are mindful of the current expensive valuations of corporate bonds versus historical levels, and we are being very selective in adding to corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.