Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

September 21, 2017

As this is being written, the Bank of Canada has raised its administered interest rates by 25 basis points. In its announcement, the Bank stated that the increase removed “some of the considerable monetary policy stimulus in place”. That phrase suggested further increases would be required if the remaining stimulus was to be eliminated. While the Bank anticipates that Canadian growth will moderate in the second half of 2017, it also believes that the economy has little remaining slack, which suggests monetary stimulus is no longer required. Interestingly, the Bank also downplayed the recent strength in the Canadian exchange rate, characterizing it instead as weakness in the United States dollar “against many major currencies”. The Bank apparently is willing to tolerate additional strengthening in the Loonie against the U.S. dollar and it would not be an impediment to further rate increases.

Notwithstanding the Bank of Canada’s somewhat hawkish statement, we believe that the Bank will pause in its rate increases so as to not get ahead of the Fed. The Canadian overnight target rate of 1.00% is now at the lower bound of the U.S. fed funds target range of 1.00% to 1.25%. We believe the Bank of Canada will probably wait for the Fed to raise rates, most likely at its December meeting, before it moves again. Rather than an interest rate increase, the Fed’s next move is likely to be implementation of its plan to gradually unwind its massive holdings of U.S. Treasuries and mortgage-backed securities. We believe that the Fed will announce that at its September 20th meeting.

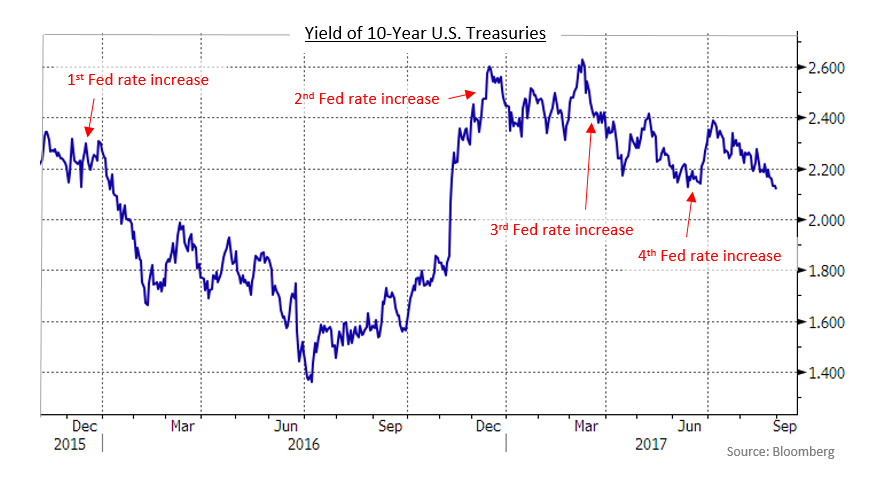

Anticipation and implementation of Bank of Canada rate increases has led to higher short and mid term bond yields in the last three months, and we believe that further administered rate increases will push bond yields still higher. However, we note that central bank rate increases do not always lead to higher bond yields. As can be observed in the following chart, since the Fed began a series of four 25 basis point rate increases in December 2015, the yield of 10-year U.S. Treasury Bonds has declined modestly.

Strategically, we are keeping the portfolio durations shorter because we believe that further central bank moves are likely in the coming months and that these will eventually push bond yields up and prices down. As well, Canadian government bond yields remain lower than U.S. Treasury yields for all but the shortest maturities. The better economic performance of Canada suggests that our yields should move closer to, and possibly higher than, comparable U.S. yields. In other words, the Canadian bond market is likely to underperform the U.S. one, even if the U.S. does not move to higher yields.

Cash levels in the portfolios have been kept relatively high as a hedge against the Bank increasing rates. We anticipate that with the Bank’s latest move there will be opportunities to lock in higher yields as we invest the cash balances in short term bonds. We have reduced slightly the allocation to corporate bonds and may make further reductions because their yield spreads are no longer as attractive as they once were. We have also minimized exposure to the retailing sector and to retail-oriented real estate issuers.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.