Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 5, 2026

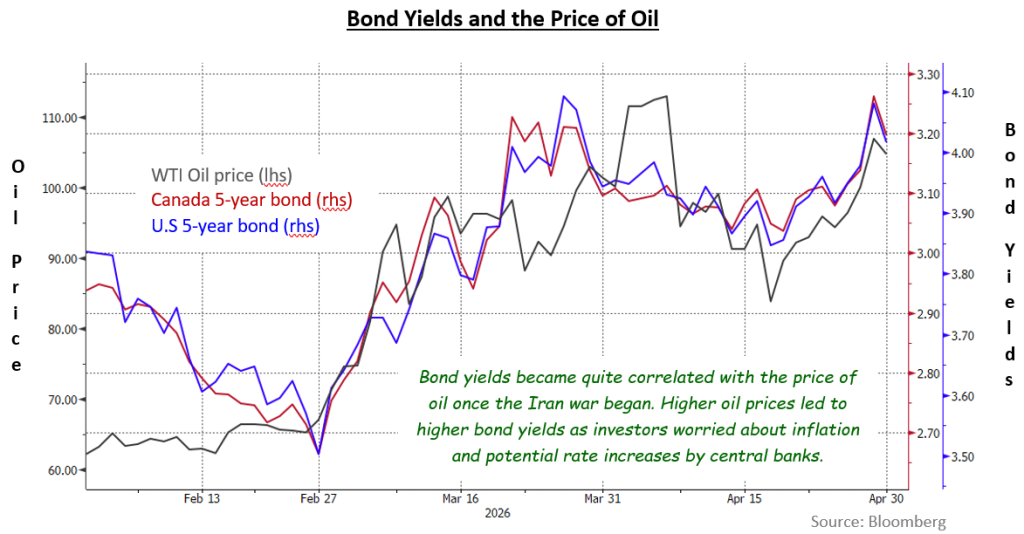

Bond yields fluctuated in a narrow range for much of April. However, a spike up in oil prices late in the month caused bond yields to rise and finish higher on the month. As can be observed in the chart below, bond yields have closely followed oil prices since the start of the war in Iran because investors are concerned that higher inflation will cause central banks to raise interest rates. The rise in oil prices occurred despite a ceasefire in the war being in place for most of the month. The lack of progress in peace negotiations between the United States and Iran led to speculation that the Strait of Hormuz would remain closed for considerably longer than previously thought, meaning no relief from the shortage of oil for several more weeks, if not months. Several major central banks noted the potential effects of high oil prices but refrained from adjusting rates. The FTSE Canada Universe Bond index returned only 0.12% in the month, as slightly higher yields pushed bond prices a little lower.

In contrast with bonds, equity markets shrugged off the rise in oil prices and their potential negative economic impacts as stocks enjoyed strong gains in the period. The U.S. S&P 500 gained more than 10% while the tech-heavy NASDAQ rose more than 15%. Canada’s S&P/TSX trailed but still gained 3.8% in the month. The positive sentiment in equities benefitted credit spreads in the bond market, as they reversed some of the widening that had occurred in February and March. Provincial yield spreads tightened by 5 basis points on average and corporate yield spreads narrowed an average of 8 basis points. The tighter corporate spreads came despite heavy new issue supply. A total of $22.1 billion new corporate bonds were issued in April, the third highest monthly total ever. Relatively high absolute yields appeared to attract investors even if the risk premiums were near historic lows.

Economic data received in April was mixed as the Canadian economy continued to struggle as a result of the U.S. trade war. The pace of Canadian GDP growth over the last year was estimated to be only 1.0% and the unemployment rate held at the relatively high rate of 6.7%. The jump in gasoline prices in March showed up in the CPI inflation rate as it rose to 2.4% from 1.8%. The federal government provided a budget update with its Spring Economic Update. The deficit for the fiscal year ended March 31st was estimated to be $66.9 billion, well below the $78.3 billion assumed last fall, because of higher tax revenue and reduced spending. Unfortunately, the good news was not expected to continue because of the $15.7 billion of new spending measures announced since last fall. In light of the slow pace of economic growth, the increased fiscal stimulus is expected to add about 0.5% to the pace of GDP growth this year.

On April 29th, the Bank of Canada left its overnight target interest rate unchanged at 2.25%, as had been widely expected. The Bank acknowledged there was economic slack and various sectors were performing differently: “Consumption and government spending are key sources of strength, while exports and business investment remain weak, continuing the pattern seen in 2025. A slowdown in the housing market is also weighing on growth.” The Bank indicated a willingness to either raise interest rates (if oil prices stayed high and led to more widespread inflation) or to lower them (if higher U.S. tariffs caused weaker economic activity). On the day of the announcement, Canadian yields moved higher, particularly for shorter maturities, because the Bank had presented a scenario of higher for longer oil prices leading to the need for higher interest rates and coincidentally oil prices spiked higher on the day. We believe the Bank is most likely on hold for the balance of this year.

In contrast with the sluggish Canadian economy, the U.S. economy appeared resilient, with GDP growing at an annual rate of 2.0% in the first quarter of this year. Robust investment in Artificial Intelligence (AI) and strong consumer spending were primary drivers of growth, but the economy also benefitted from a rebound following the end of last fall’s federal government shutdown. The unemployment rate declined to 4.3% from 4.4% on good job creation, and retail sales were stronger than expected. Inflationary pressures increased with CPI rising to 3.3% from 2.4%, and the quarterly core PCE price index jumped to a 4.3% pace from 2.7%.

The Fed also met on April 29th and, as expected left its rates unchanged. Interestingly, there were four dissents to the decision, with one committee member wanting a 25 basis point rate reduction and three members objecting to “the inclusion of an easing bias in the statement at this time” although it was not obvious what part of the statement they were objecting to. The immediate market reaction saw Treasury bond yields move sharply higher as the potential for rate cuts appeared reduced. Global bonds, including Canadian ones, followed Treasuries lower in price and higher in yields.

The Fed meeting was likely Jerome Powell’s last one as Chairman, because the nomination of Kevin Warsh as his successor began the approval process with the Department of Justice ending its investigation into Powell. Powell, however, will remain on the committee as a Governor once his term as Chairman ends, making it less likely that there will be a significant change in policy once Warsh takes over.

The last week of April was a busy one for central bank meetings. In addition to the Bank of Canada and the Fed meetings, the Bank of Japan, the European Central Bank, and the Bank of England each met to decide whether to adjust their respective monetary policies. The Bank of Japan, as expected, left its rate unchanged at 0.75%, but the vote was split 6-3, with the three dissenters wanting to raise the rate. Compared with the 8-1 split in March, it suggested a greater likelihood of a rate increase at the next meeting in mid-June. The foreign exchange market was less impressed and over the next few days the Yen weakened to the psychologically important 160 level, prompting government intervention (selling of U.S. dollars to buy Yen). If continued intervention occurs, that could prompt selling of U.S. Treasuries to fund the dollar sales. The Bank of England and the European Central Bank completed the month leaving their respective interest rates unchanged, choosing to wait and see the duration of the energy price shock and whether it leads to a broader acceleration in inflation.

As this is being written, the FTSE Canada bond indices have adjusted their durations, primarily because the $25.7 billion Canada 2.75% May 1, 2027 issue dropped out on May 1st. Whenever the shortest bond or a coupon payment is removed from the calculation, the average duration increases. In this case, the Short Bond index duration has risen 0.04 years, while the Mid and Long Term Bond indices are little changed. The Universe Bond index duration rose 0.06 years.

Much bigger changes, though, are anticipated on June 1st and 2nd, because the majority of federal and provincial bonds mature in either June or December, and pay interest in both. On June 1st and 2nd, the Universe index duration is estimated to increase a combined 0.14 years as a result of $41.4 billion of 1-year bonds falling out of the index and the payment of a record $18.3 billion in coupons. The Short Term Bond index duration is expected to increase 0.16 years, while the Mid Term Bond index duration will increase 0.27 years. The Long Term Bond index duration will see the largest increase, rising 0.54 years, primarily because $43 billion of 10-year bonds will shift into the Mid Term index. The change in the Long Term index duration is typical of other June and December index rebalancing and is expected to result in significant buying of 30-year bonds, most heavily in the afternoons of June 1st and 2nd by passive index funds and closet-index managers.

The Canadian yield curve flattened somewhat in April as 2-year and 5-year Canada bond yields climbed 14 basis points, while 30-year yields gained only 5 bass points. In contrast, the U.S. Treasury yield curve experienced almost a perfect parallel shift upward with 2, 5, and 10-year yields all rising 8 basis points, while 30-year yields were up 10 basis points.

The increase in yields caused price declines that left the federal sector of the Canadian bond market with a -0.19% return. The provincial and investment grade corporate sectors benefitted from the spread tightening that occurred, earning +0.34% and +0.40%, respectively. Non-investment grade corporate bonds returned 0.89%, buoyed by robust equity markets. Real Return Bonds earned 0.39%, outperforming nominal issues as inflation accelerated. Preferred shares performed markedly better than bonds in April, gaining 2.51% in the month.

We believe that, as a result of the recent pandemic-induced spike in inflation, bond investors are too focussed on the potential for inflation and not paying enough attention to the economic risks of higher energy prices and the U.S. trade war. We acknowledge the inability of the United States to produce a satisfactory conclusion to the war means it may extend at least another quarter or two, but we believe that we are not in for a prolonged period of elevated inflation.

We believe the Bank of Canada will look through the temporary spike in inflation that is occurring. Higher interest rates won’t lower gasoline prices, though. With the Canadian economy already struggling due to the U.S. trade war, the potential for demand destruction due to higher energy prices and uncertainty around the Iran war could slow domestic economic activity even more. Global growth also seems at risk. We believe the Bank of Canada is unlikely to raise interest rates this year, while interest rate cuts are a growing possibility. Consequently, we believe the recent rise in short term bond yields is likely to reverse.

With the narrowing of yield spreads in April, both the provincial and corporate sectors are historically very expensive, in our opinion, and do not properly reflect the currently elevated economic risks. Corporate bonds, we believe, are particularly vulnerable to a correction in equity markets. We also remain concerned that a developing liquidity crisis in private credit may spill over to public credit markets. In both Canada and the United States, large private credit funds have had to restrict, or “gate”, withdrawals because the funds did not have sufficient liquidity to satisfy investors’ redemption requests. In Canada, the biggest problems in private credit appear to be in the real estate sector, particularly for loans to condo developers. In the United States, private credit concerns appear to be particularly concentrated in software development firms negatively impacted by AI coding. What is unknown are the exposures of banks and alternative lenders to private credit.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.