Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 10, 2025

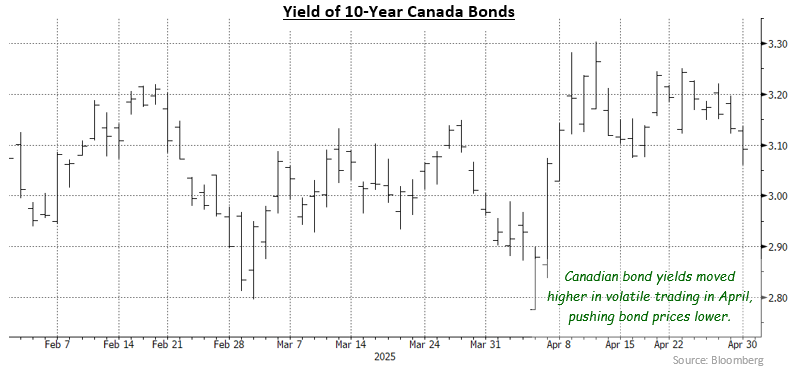

U.S. President Trump’s erratic policies generated considerable volatility in financial markets during April. Late in the afternoon of April 2nd, Trump imposed 10% tariffs on virtually all U.S. imported goods, as well as “reciprocal” tariffs on 60 countries. Equity markets were swift to react, with the S&P 500 plunging over 12% and the S&P/TSX dropping 11% in the next four days. The sharp equity selloff led the U.S. president to pause the reciprocal tariffs for 90 days, with the notable exception of those imposed on China. The equity markets subsequently recovered most, if not all, of their losses over the balance of the month. Bond markets also reacted to the tariff news, with 10-year U.S. Treasury yields rising a remarkable 50 basis points in a week, as the U.S. trade war with China escalated. Once the tit-for-tat escalation in tariffs paused (at the eye-watering 145% level) bond yields began reversing some of their move. In addition, yield spreads on corporate bonds moved sharply wider due to recession concerns and the plunge in stock prices. Bond market volatility was also increased by Trump’s criticism of Federal Reserve Chair Jerome Powell and his expressed desire to fire Powell. While Trump does not have the legal authority to fire the Fed chair, his threat to the Fed’s independence raised concerns about the safety and stability of U.S. Treasuries. The FTSE Canada Universe index returned -0.65% in the month.

Economic data received in April reflected activity prior to the implementation of most of of the new U.S. tariffs, making the data less useful in anticipating future trends. It did suggest, however, that businesses and consumers are acting cautiously in advance of potential economic upheaval from the tariffs. The unemployment rate edged up to 6.7% from 6.6% as a decline in the participation rate failed to offset the loss of 32,600 jobs. Housing starts were weaker than expected and Canadian GDP declined 0.2% in February, although the drop was primarily due to severe weather in the period. Inflation unexpectedly fell to 2.3% from 2.6%, mainly as a result of a decline in gasoline prices. The Bank of Canada chose to leave its administered interest rates unchanged, waiting to evalute the impact of the U.S. trade war. The federal election had little impact on the bond market.

As in Canada, the U.S. economic data received in April dealt with activity prior to most of the tariffs being implemented, but indicated businesses and consumers were becoming concerned that growth could be hurt. The unemployment rate rose to 4.2% from 4.1% and business surveys suggested firms were not adding to their workforces. The consumer sentiment survey indicated steady views of the current situation but sharply lower future expectations. The U.S. GDP shrank at an annual rate of 0.3% in the first quarter, but the decline reflected a surge in imports due to frontrunning of the tariffs. Excluding the imports, U.S. growth remained positive. The bond market was less optimistic about the future, though, as short term bond yields fell in April because investors anticipated slower growth that would cause the Fed to lower interest rates.

Internationally, the European Central Bank followed up its March rate cut with another 25 basis point reduction in April. The Reserve Bank of New Zealand also lowered its interest rates by 25 basis points in the month. The imposition of tariffs prompted dozens of countries to initiate trade negotiations with the United States, but despite Trump’s hope for successful deals, the only agreements were to start talking.

The Canadian yield curve “bear steepened” in April as the yields of longer term bonds rose (and their prices dropped), while short term bond yields were little changed. The yields of 30-year Canada bonds, for example, rose 19 basis points, while 2-year yields gained only one basis point. Yields of mid term issues also rose, but by lesser amounts. The increase in longer term yields suggested the Bank of Canada’s pause made investors reconsider their expectations for additional rate reductions in the future. The U.S. yield curve also steepened in the month, but in a different manner than in Canada. Investors in U.S. Treasuries appeared concerned that Trump’s erratic trade policies would cause a significant economic slowing that would eventually cause the Fed to cut its interest rates. Yields of 2-year and 5-year Treasuries fell roughly 30 basis points, and only 30-year yields increased, finishing 7 basis points higher on the month. Longer term investors may have been swayed by the lack of attention to the United States’ massive fiscal deficit, as well as the potential for higher inflation as a result of the tariffs on U.S. imports.

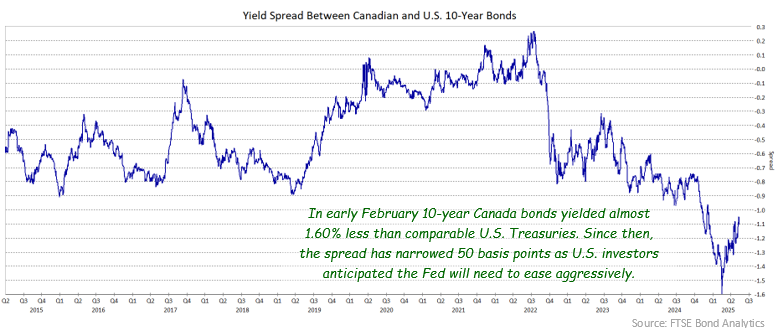

The different shifts in Canadian and U.S. yields meant that Treasuries continued to recover from the record yield differences hit in early February. At that time, U.S. yields were higher than comparable Canadian ones by a larger margin than they had ever been. The yield of 10-year Treasuries, for example, was close to 160 basis points higher than that of 10-year Canada bonds. In the last three months, however, that differential has shrunk to 110 basis points.

The rise in Canadian yields resulted in bond prices declining and caused the federal sector to return -0.44% in April. The provincial sector, which is more exposed to changes in longer term yields, returned -1.08%. Provincial yield spreads were little changed in the period. Investment grade corporate bonds returned -0.42% despite some small net widening of the yield spreads for short and mid term issues. The average duration of the corporate sector is almost a year and a half shorter than the broad Universe index, which meant higher yields had less impact. Corporate yield spreads initially widened with the tariff related volatility early in the month but mostly recovered by the end of the period on good investor demand and a shortage of new issues. Only $3.6 billion of new issues came to market in April, the lowest monthly total in several years. Non-investment grade corporate bonds returned -0.47% as their higher yields offset wider yield spreads in the risk-off environment. Real Return Bonds declined 1.80% in April, hurt by their longer durations and the lower than expected inflation rate. Preferred shares returned -3.12% in the month, as they sold off in the early volatility but failed to fully participate in the subsequent equity market recovery.

Given the on again off again implementation of Trump’s multiple levels of tariffs, combined with his narcissistic need to be in the headlines, it is difficult to anticipate how the trade war will unfold. We believe Canada has an advantage in negotiating with Trump because it already has a trade agreement in place. With the U.S. now negotiating trade agreements with dozens of countries, it needs to show that it will abide with existing agreements in order to close new ones. The U.S. administration seems to recognize that need as Canadian goods that are in compliance with the free trade agreement known as USMCA or NAFTA 2.0 have been exempted from U.S. tariffs. In broad terms, it seems likely that Canadian economic growth will suffer, although a recession is still only a possibility rather than a probability. We think the Bank of Canada’s recent decision to keep rates steady until it can assess the impact of the tariffs makes a lot of sense. Accordingly, we expect the Bank to be on hold until at least its July 30th announcement date.

The negative economic outlook makes us reluctant to have portfolio durations less than that of the benchmark. It also suggests caution regarding credit risk. We have reduced portfolio exposure to the corporate sector to close to benchmark levels and may reduce further should yield spreads tighten more because of lack of supply. We are also looking to shift the holdings to even more conservative ones.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.