Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 6, 2022

The bond market continued to sell off in April as inflationary pressures pushed higher and the Bank of Canada raised its overnight interest rate by 50 basis points. This was the second rate hike by the Bank of Canada in as many months and its first increase of that magnitude since May 2000. The U.S. Federal Reserve was also expected to raise its Fed Funds rate by 50 basis points in early May. With the Canadian and U.S. economies operating at full capacity, the persistence of elevated inflation exacerbated by constricted supply chains will likely keep the central banks on a tightening path for the next several meetings. The prospect of sharply higher interest rates and inflation at decades high levels led bond yields to spike higher, with the 10-year Canada bond closing the month at a yield of 2.75%, a rate not seen since 2011 and a stark difference to the summer 2020 all time low of 0.43%. The prospect of higher rates also caused some volatility in riskier assets, such as stocks, as investors were concerned that too much monetary tightening might result in a recession. Corporate bond yield spreads widened in sympathy with equity market weakness. The FTSE Canada Universe Bond Index returned -3.49% in April.

Canadian economic activity was strong in April. Economic growth was robust, as GDP grew by 4.5%, up from 3.5% the previous month. Employment increased by 72,500 jobs, which pushed the unemployment rate down to 5.3%, an all-time low. The tightness of the labour market was also reflected by the increase in average hourly wages of 3.7% versus year ago levels. Consumers remained optimistic as retail sales continued to grow. Worryingly, Canadian inflation surged to 6.7%, which was the highest level since 1991, and that led investors to anticipate further rate increases from the Bank of Canada.

U.S. economic data also remained strong. Job growth was robust and the U.S. unemployment rate in April was just above the all time low level established in 2019. With the labour situation so strong, it is not surprising that retail sales growth was positive again this month. U.S. inflation also continued to climb, with the headline rate reaching 8.5% and the core rate rising to 6.5%. The headline and core inflation rates were at their highest levels in 40 years. As with the Bank of Canada, the Fed was expected to remain in tightening mode, leading investors to demand higher yields in the bond market.

Internationally, the Russian/Ukrainian war continued, causing prices of commodities and some foodstuffs to rise further. In China, that country’s zero-Covid policy was resulting in large scale lockdowns that were disrupting its economy as well as aggravating already struggling global supply chains. Both developments added to already excessive inflationary pressures in Canada and elsewhere.

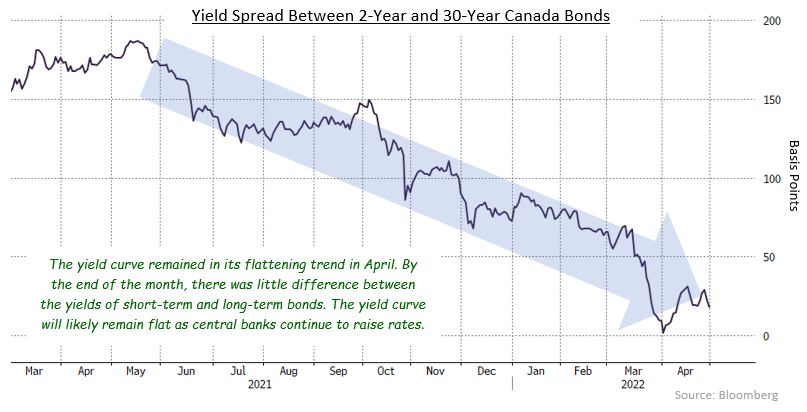

The Canadian yield curve reached its steepest level in the spring of 2021. Since that time, with the expectation of higher interest rates, shorter term bond yields have risen more than longer term bond yields, leading to a flatter yield curve. Further rate increases by the Bank of Canada in the coming months will likely extend the flattening trend and may result in an inverted yield curve, with shorter term yields consistently higher than longer term yields.

In April, Canadian federal bonds returned -2.52%, as rising yields caused bond prices to fall. Provincial bonds returned -4.61% in the month. Provincial yield spreads widened slightly in April which, combined with their longer average durations, hurt provincial bond performance. Investment grade corporate bonds returned -3.20% as their spreads widened by an average 15 basis points in response to equity market volatility and concerns about a potential recession. Non-investment corporate bonds returned -1.63% in April, outperforming investment grade corporates due to their higher coupons and shorter durations. Real Return Bonds which have relatively long durations, returned -4.84%, which was markedly better than the return of nominal bonds with similar durations. Preferred shares dropped -7.04%, as retail clients reduced their holdings in reaction to the common share volatility and higher interest rates.

With inflationary pressures reaching multi-decade highs, both the Bank of Canada and the Fed have become more aggressive in their monetary policy responses. The Bank of Canada initiated a 50 basis point hike in April and U.S. Fed Chairman Jay Powell committed to a 50 basis point increase at its next meeting on May 4. Both central banks are expected to continue with 50 basis point increases at subsequent meetings. In addition, both the Bank of Canada and the Fed are expected to begin Quantitative Tightening (reducing their respective holdings of federal bonds through maturities and/or sales) in May, which will add to upward pressure on bond yields.

In mid-April, we re-established a moderate underweight in duration relative to the benchmark. We believe both the Bank of Canada and the Fed are behind in their efforts to control inflation and will need to raise rates substantially in the coming months in order to slow demand and reduce inflationary pressures. The interest rate increases plus the initiation of Quantitative Tightening will put upward pressure on bond yields, hence the move to a more defensive duration.

As mentioned above, we believe the yield curve may flatten further and eventually invert as the Bank of Canada continues to aggressively tighten monetary policy. While an inverted yield curve is often considered an indicator of a pending recession, we do not believe one is imminent in Canada as growth is expected to remain acceptable for the next year or so. We anticipate that the yield curve will trend flatter and we continue to structure the portfolios to preserve value as shorter term yields are pushed higher.

Corporate yield spreads are, in our opinion, attractive, and we are monitoring the market for opportunities to add to our holdings. We also believe that, in the environment of central banks tightening aggressively, we can afford to be patient in our search for additional value in this area.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.