Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 6, 2021

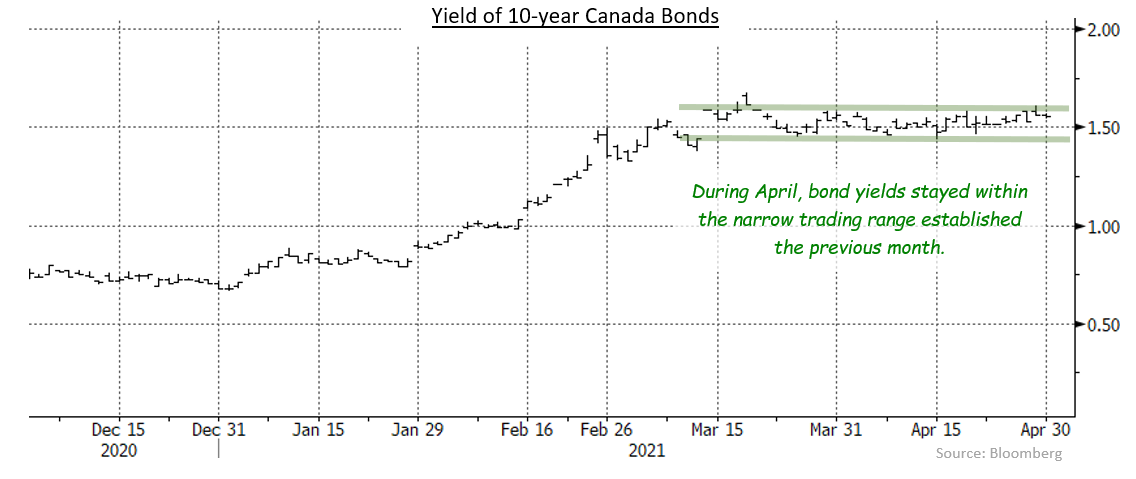

Following its sharp selloff of the first quarter, the bond market paused in April, trading within a narrow range all month. The stability was not due to a lack of significant news in the period. The lull between the second and third waves of the pandemic saw further recovery in the Canadian economy and provided reasons to be optimistic when current restrictions are lifted. Both the Bank of Canada and the U.S. Federal Reserve met in the month, and each surprised the markets, albeit in different ways. And the Government of Canada released its first budget in over two years, and as part of the process made significant changes to its plans for financing the deficit. The FTSE Canada Universe Bond index returned 0.06% in April, the first positive monthly return this year.

Canadian economic data received during April was generally robust and much better than forecasts. For example, a massive 303,000 increase in jobs during March (prior to third wave lockdowns) caused unemployment to fall to 7.5% from 8.2% and the participation rate to improve to 65.2% from 64.7%. Housing starts jumped 22% to the fastest pace in over four decades, while retail sales in February surged 4.8% higher from upwardly revised January sales. Canada’s GDP during February grew by 0.4% and StatsCan estimated growth accelerated to 0.9% in March. The year-over-year inflation rate doubled to 2.2% from 1.1% the previous month as the increase was measured from the depths following the start of the pandemic. The core rate of inflation edged up to 1.9% from 1.8% the previous month. The bond market took the good economic news in stride in part because the pandemic’s third wave was causing renewed restrictions on activity. As well, the sharp rise in bond yields in the first quarter had anticipated some, if not all, of the recent economic bounce.

As previously noted, after more than two years, the federal government finally released a new budget in April. Canada had been the only G-7 country not to produce a federal budget during the pandemic. With the federal Liberals widely expected to call an election later this year, the budget was chock full of policy proposals and spending initiatives rather than focusing on restoring the fiscal balance. Compared with last fiscal year’s $354 billion record shortfall, the 2021-22 deficit was projected to fall to $155 billion, but was higher than $121 billion forecast in last Fall’s Economic Statement. Along with the budget, the federal government released its annual Debt Management Strategy (DMS) that showed how the deficit was expected to be financed. Issuance of 2, 3, and 5-year bonds was predicted to fall sharply, but significantly more 10-year bonds were to be issued. The expected issuance of 30-year bonds was unchanged from last year’s total, although the government also proposed reopening the 2064 Canada bonds for $4 billion over the next twelve months. The greater reliance on longer term bonds was deliberate as the government was trying to lengthen the average duration of its debt. However, the bond market reacted to the DMS by immediately steepening the long end of the yield curve, with 30-year bond yields moving markedly higher.

At its April meeting, the Bank of Canada did the expected and left its trendsetting interest rates unchanged while lowering its bond purchases from $4 billion per week to $3 billion. More surprising was a dramatic shift in the Bank’s economic outlook from cautious and pessimistic to quite optimistic. The Bank now expects first quarter GDP growth to have been at a +7.0% pace, rather than shrinking by 2.5% as it had predicted only three months ago. The Bank also raised its outlook for all of 2021 to +6.5%, up from +4.0%. Most importantly, the Bank’s new forecast called for the output gap (i.e. the amount of slack in the economy) to close in the second half of next year rather than sometime in 2023 as previously predicted. As a result, the bond market anticipated the Bank’s first rate increases might occur as soon as October 2022, which led to some slight upward pressure on the yields of short term bonds.

As in Canada, U.S. economic data received during April were very strong. Growth in the U.S. GDP during the first quarter accelerated to 6.4%, up from 4.3% in the final quarter of 2020. Unemployment declined to 6.0% from 6.2% and the participation rate rose because of robust job creation, especially in sectors such as leisure and hospitality that were reopening. The housing sector continued to be very active, with starts and sales of new homes hitting their highest levels since 2006. In addition, retail sales jumped a remarkable 9.8% in March alone, likely due to the $1,400 stimulus cheques sent to most Americans. Similar to the Canadian experience, though, U.S. bond investors were blasé to the very strong economic news, prompting one market strategist to coin a new term “datapathy” from the melding of “data” and “apathy”.

Remarkably, the U.S. Federal Reserve, also had very little reaction to the rapidly recovering U.S. economy. As expected, the Fed left its rates unchanged at its April meeting, and it acknowledged the better than expected economic results. However, unlike the Bank of Canada, the Fed made no mention of changing its quantitative easing programme that buys $120 billion of bonds every month. Asked if the Fed is “talking about talking about tapering” its QE, Fed Chair Jay Powell said, “The economy is a long way from our goals.” We suspect the Fed’s reticence to discuss reducing its massive monetary stimulus reflects concern that the Taper Tantrum of 2013 might be repeated. Eight years ago, the U.S. was in the midst of an earlier version of QE, and the mere mention of a potential gradual reduction in bond purchases by the then Fed Chair led to a very sharp selloff in U.S. Treasuries. Unfortunately, the continuing strong rebound in the U.S. economy as a result of massive fiscal stimulus and widespread vaccinations is making the current QE less necessary and some reduction is increasingly likely.

Usually Canadian and U.S. bonds move in similar fashion, but not so in April. The Canadian yield curve steepened in the month as 2-year Canada yields went up 4 basis points, while 30-year yields rose 11 basis points. The lift in short term yields was a reaction to the Bank of Canada revising its economic projections while the increase in 30-year yields reflected the greater emphasis on longer term issuance in the DMS. Interestingly, 5-year Canada yields declined 6 basis points while short and long term yields rose. In the U.S., the yield curve flattened as 2-year Treasury yields were unchanged while 30-year yields declined 12 basis points. Yields of 5 and 10-year Treasuries moved lower by smaller amounts. The decline in U.S. yields was a consolidation following the sharp rise in yields in the first quarter. The dovish Fed announcement had little impact because it came near the end of the month.

Federal bonds returned -0.01% in April as price declines were almost exactly offset by interest income. Provincial bonds returned +0.15% in the month. The provincial results benefitted from a 4 basis point narrowing of average yield spreads versus benchmark Canada bonds that offset larger price declines from longer average durations. Investment grade corporate bonds returned +0.01% as a slight narrowing of short and mid term yield spreads compensated for a slight widening of long term yields. Non-investment grade bonds returned +0.98%, as they followed stronger equity markets higher. Real Return Bonds earned -1.79%, which was surprisingly worse than similar duration nominal bonds. Investors apparently agreed with the Bank of Canada’s assessment that inflationary pressures would not last. Preferred shares enjoyed another strong month, rising 2.06% as announcements of share redemptions caused prices to move higher.

As we noted last month, the bond market often pauses and consolidates within a trading range after a significant change in yields, so we were not surprised by the sideways movement in April. The question now is how long it will it last? We believe it could last another month or two, particularly if yields eventually start rising again, because the market has already anticipated a very robust recovery with rising inflation. The recent increase in inflation was mainly due to base year effects as plunges in prices a year ago fell out of the calculation. Going forward, if supply bottlenecks in areas as diverse as computer chips, lumber, and soybeans extend, costs will rise, and firms will increasingly pass them along to consumers. Unless the increase in inflation soon proves transitory, as central bankers are hoping, the bond market may react and move to higher yields. In addition, the ongoing deluge of government bond issues should provide significant upward pressure on yields. As a result, we are maintaining portfolio durations somewhat shorter than benchmarks and are looking for opportunities to shift to an even more defensive stance.

The overall yield curve will likely steepen as most bond yields rise while short term yields are restrained by the lack of movement in the Bank of Canada’s overnight target rate. Notwithstanding their better performance in April, we think mid term yields will anticipate reductions in monetary stimulus, leading to a steeper yield curve in the shorter maturities and a flatter curve for longer term issues. Accordingly, we have reduced portfolio exposure to the mid term sector.

We remain somewhat cautious about corporate bonds as they remain historically expensive. Should benchmark Canada yields resume rising in the next few months, issuers will try to lock in low financing rates and new issue supply will weigh on valuations. We also wonder if rising benchmark yields will reduce the seemingly insatiable demand for the higher yield of corporate bonds.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.