Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 4, 2026

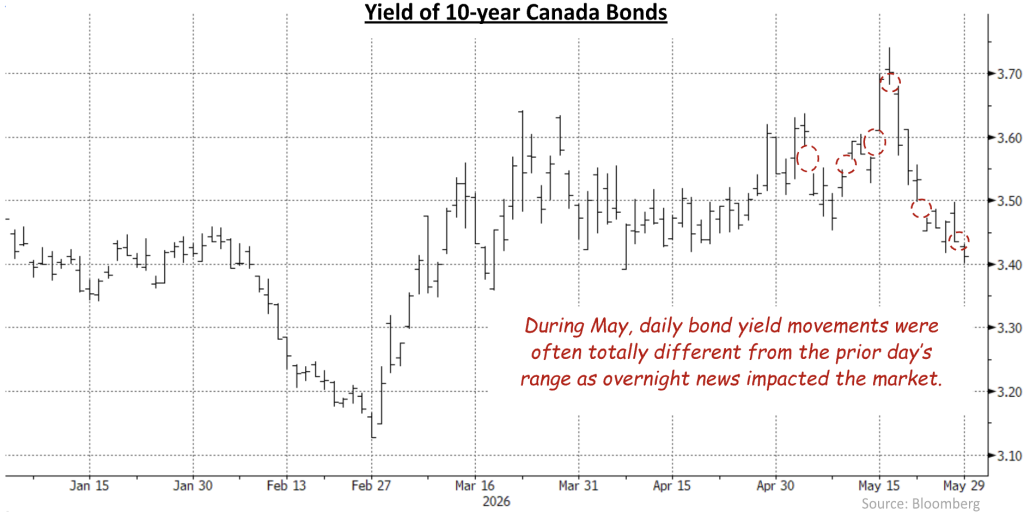

The Canadian bond market was choppy and volatile in May, with overnight developments frequently leading to significant shifts in bond prices and yields. The U.S./Israel war with Iran was, of course, one source of market moving headlines as speculation on peace negotiations led to price fluctuations in bonds, as well as in oil. (Over the month, the price of WTI oil initially fell from $105 per barrel to $90, then climbed back to $109 before falling and ending at $87.) However, there were other sources of volatility including political turmoil in Great Britain and large scale intervention in foreign exchange markets by the Bank of Japan to bolster the value of the Yen. Weaker economic data in Canada led investors to reduce expectations for Bank of Canada rate increases, while in the U.S. investors became less optimistic that the Federal Reserve would lower its interest rates. The month also featured a record breaking new corporate issue from Alphabet, the parent company of Google. The FTSE Canada Universe Bond index gained 1.36% in the month.

Canadian economic data received in May showed that the economy was continuing to struggle. Growth in Canadian GDP was weaker than expected in the first quarter at -0.1% which, combined with the 1.0% decline in the fourth quarter of 2025, met the technical definition of a recession. While other indicators such as domestic demand and investment spending failed to confirm a recession, weakness in the economy was apparent in the labour market statistics. The unemployment rate rose to 6.9% from 6.7% and the economy has shed 111,000 full-time jobs since the start of the year. Retail sales were stronger than expected, but only due to the jump up in the price of gasoline. Excluding gasoline, retail sales declined. Inflation rose to 2.8% from 2.4%, but that was well below the consensus forecast of 3.1%. Importantly, there was no indication that the surge in energy prices was leading to broader inflation in the rest of the economy. The weak economic data and lower than expected inflation caused investors to revise lower their expectations for Bank of Canada interest rates later this year, which resulted in lower bond yields and higher prices.

In the United States, that economy remained resilient notwithstanding a revision in the first quarter pace of GDP growth to 1.6% from 2.0%. The unemployment rate was steady at the low level of 4.3%, and investment spending continued growing strongly due to the Artificial Intelligence (AI) boom. Interestingly, the AI spending is not noticeably impacting GDP growth because most of the chips and other required equipment need to be imported, and imports are a negative factor in the GDP calculation. Inflation accelerated to 3.8% from 3.3% the previous month, and core measures also rose, which caused investors to reduce their expectations for interest rate cuts and pushed U.S. bond yields higher. Kevin Warsh was sworn in as Chairman of the U.S. Federal Reserve, while his predecessor, Jerome Powell, remained as a Governor.

Internationally, the British Prime Minister, Keir Starmer, came under substantial pressure to resign following poor results in local elections. The political uncertainty led to concerns of wider budget deficits and U.K. 30-year bond yields rose to their highest levels since 1998. Global bond yields moved higher in sympathy, although not to the same degree. In Japan, the Yen weakened through the 160 level which prompted the Bank of Japan to spend almost U.S. $74 billion to bolster the exchange rate. The intervention would have required the Bank to sell holdings of U.S. Treasury bills and bonds, putting upward pressure on U.S. yields. The intervention also prompted speculation that the Bank would be forced to raise interest rates to strengthen the Yen, which led to a rise in Japanese bond yields . The Bank of Japan’s efforts to defend its currency followed a similar exercise by the Turkish central bank in March. During May, we learned that the Central Bank of the Republic of Turkey had sold 89% of its U.S. Treasury securities, totaling U.S. $14 billion, defending the Turkish lira two months earlier. Elsewhere in the world, Norway’s Norges Bank and the Reserve Bank of Australia each raised their respective interest rates by 25 basis points to counter higher than desired inflation.

As noted above, one of the so-called hyper-scalers in AI, Alphabet, brought a multi-tranche new issue to help fund its massive capital spending plans. At $8.5 billion, Alphabet’s issue eclipsed the previous $7.15 billion record that Coastal GasLink raised in June 2024. Rated AA, the Alphabet issue was priced at spreads equivalent to those of A-rated issues, which led to some widening of the lower rated issues’ spreads, as well as some tightening of Alphabet spreads after the new issue. Another noteworthy corporate event was yet another bond tender by BCE Inc. It will be buying back bonds denominated in both Canadian and U.S. dollars, although the exact amounts have not yet been disclosed. Unlike previous tenders that were funded by the issuance of subordinate hybrid securities that received partial equity treatment by rating agencies, the current tender was funded with the issuance of approximately $2.5 billion of senior bonds. While there was some benefit in repurchasing bonds at discounts to par, as with the previous tenders, the main purpose of this tender appeared to be extending the average term of BCE’s debt and reducing near term refinancing needs rather than deleveraging.

Reduced expectations for the Bank of Canada to raise rates later this year, which we have long discounted, resulted in bond yields declining across the maturity spectrum. The yield of 2-year Canada bonds declined 19 basis points, while 10-year and 30-year Canada bond yields fell 14 basis points during May. In contrast, U.S. Treasury yields rose at all maturities and their yield curve flattened in the month. Yields of 2-year and 5-year Treasuries rose 13 basis points, while 30-year yields edged up by only a single basis point.

Lower yields helped propel the federal sector to a return of 1.13% in May. The provincial sector, which has a longer average duration and is, therefore, more responsive to yield changes, gained 1.75%. Provincial yield spreads also edged slightly tighter in the month. The investment grade corporate sector earned 1.26% in May. Short and mid term corporate yield spreads narrowed a few basis points in the month, but long term spreads widened slightly, perhaps due to the pressure caused by the Alphabet new issue. Non-investment grade corporate bonds trailed the higher quality issues, earning only 0.99% in the period. The rise in inflation appeared to spur interest in Real Return Bonds, as they rose 2.35%. Preferred shares fared slightly better than bonds in the month, returning 1.56%.

The Bank of Canada is scheduled to release its next decision on interest on June 10th. We believe the Bank will leave rates unchanged at that meeting, as well as for the balance of this year. The weak state of the economy is offsetting the risk of higher inflation, and the lack of evidence that inflationary pressures are broadening will allow the Bank to be patient about adjusting monetary policy. We anticipate market expectations for rate increases later this year will continue to unwind, resulting in lower short term bond yields. Longer term bond yields may not rally as much, however, given the volatility of international bond markets.

We remain cautious about the corporate sector because yield spreads are at historically tight levels and, in our opinion, do not properly reflect the current levels of economic and financial risks. We recognize, though, that yield spreads may stay narrow for some time, so we are maintaining a sector allocation that is close to neutral while trying to further reduce credit risk.

As this is being written, the European Central Bank has released statistics showing that gold has supplanted U.S. Treasuries as the most common reserve asset of global central banks. At the end of 2025, gold accounted for 27% of reserve assets, while Treasuries amounted to 22%. The doubling of the price of gold in the last two years obviously played a significant role in the change. However, central banks have also been relentlessly buying gold for several years (and helping to push the price higher).

One reason for the shift to buying gold is reduced trust in U.S. dollar assets. The repeated use of financial sanctions by the U.S. government, including those imposed on Russia following its invasion of Ukraine, has encouraged diversification away from U.S. dollar assets. With no effort being made to control the massive U.S. fiscal deficit, the shift by foreign investors away from U.S. dollar-denominated securities may eventually lead to higher U.S. bond yields. That could lead to increased market volatility, but Canada could also benefit as a high quality, creditworthy alternative.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.